Data as of December 31, 2024, and March 31, 2025.

Theoretical Investor indifference is based on the highest federal tax bracket of 37%.

Sources: MMD (Municipal Market Data), Bloomberg, and BBH.

Highlights

|

Five years ago, our lives came undone from a global pandemic. Face masks, remote work, and social distancing became commonplace amid rampant contagion fear. Financial markets spiraled as volatility reached crisis levels, and we all focused on our work as a welcome respite. Capitalizing on volatility-driven opportunities is core to our strategy, but protecting our clients’ capital has always been our number one priority. When we discuss the concept of credit durability, it typically connotes resilience in the face of a variety of economic conditions. Today, our portfolios also face a growing array of political risks.

From persistent inflation to geopolitical conflicts, to nascent trade wars and growing questions about how tax cuts will be funded, today’s news is dizzying. With progress in the fight against inflation stalled, policy risks rising, the Federal Reserve (Fed) faces an even more difficult landscape than usual. The monetary policy transmission mechanism was blunted during the tightening cycle that ended last year and we wonder how monetary policy can effectively respond to potentially high and sustained tariffs. Thus far, investors and the Fed have tried to look through the noise. We entered 2025 with investors expecting 75 basis points (bps)1 of easing by the end of 2026 and we ended the quarter with 100 bps priced in.

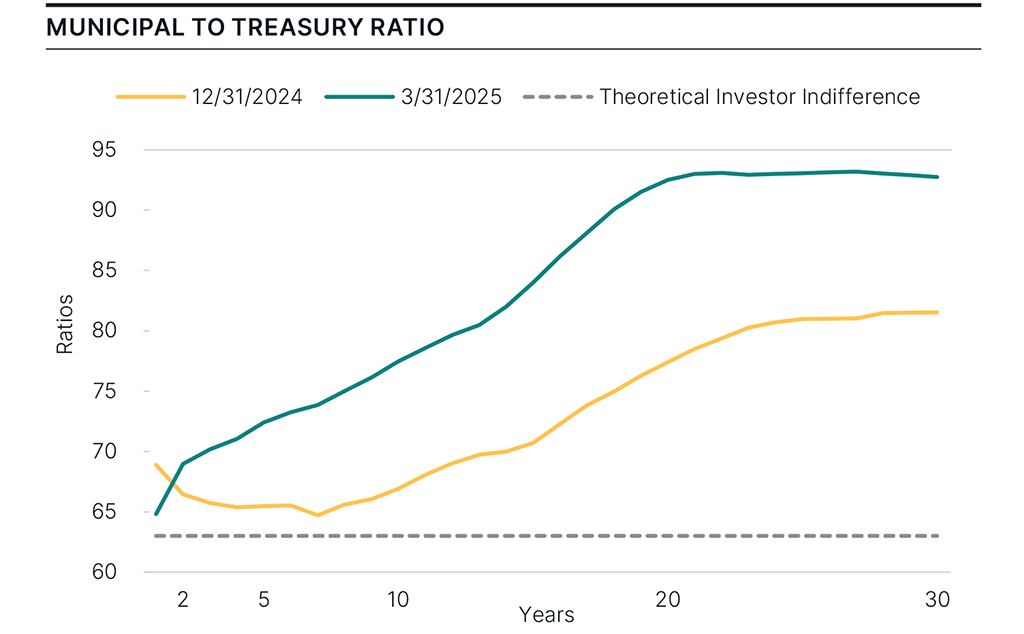

Expectations of further Fed easing, coupled with rising uncertainties, drove yield curves steeper during the quarter with two-year tax-exempt yields falling 10 bps and 10-year yields rising by 15 bps. With yields up nearly 50 bps, 30-year municipals severely underperformed. Many cite threats to the tax treatment of municipals as a reason or both the relative underperformance of long bonds and of municipals relative to Treasuries. For the quarter, municipal-to-Treasury ratios widened five-to-10 percentage points, the majority of which occurred after the second week of March.

Data as of December 31, 2024, and March 31, 2025.

Theoretical Investor indifference is based on the highest federal tax bracket of 37%.

Sources: MMD (Municipal Market Data), Bloomberg, and BBH.

The last time municipal yields traded this wide relative to Treasuries was in the fall of 2023.

Municipal new issuance momentum carried into the new year. After eclipsing $500bn for the first time in 2024, first quarter 2025 issuance of $120 billion exceeded last year’s tally by 20%. Many issuers accelerated deals last year to front run potential election-induced volatility. This year, issuance is being pulled forward to get ahead of legislative changes. Up until mid-March, the new supply was easily absorbed, and investor sentiment remained positive, reflected by $1 billion in average weekly inflows. Only time will tell whether the late-quarter weakness portends a broader trend.

Despite all the political noise and market volatility, our intermediate portfolios ended the quarter with modestly positive returns, both on an absolute basis and relative to our benchmarks. In general, the outperformance of low rated credit and the outperformance of short maturities as the yield curve steepened detracted from our relative results. We typically de-emphasize traditional short maturity fixed-rate municipals in favor of floating rate notes and zero-coupon bonds, which also lagged. Our portfolios’ yield advantages and the performance of our Freddie Mac and Fannie Mae-backed multi-family housing bonds offset these factors. By trading convention, many of the multi-family related bonds we own tend to track Treasury performance even though they pay tax-exempt interest. As Treasuries outperformed municipals, these bonds benefited significantly.

Ending the tax-exempt status of municipal bond income has been mentioned as an option to offset some of the cost of the Tax Cuts and Jobs Act (TCJA) extension. It will surprise no one that we think this is a bankrupt idea. As we learned from the Build America Bond experiment in 2009 and 2010, taxable bonds usually find their way into exempt accounts such as IRAs, endowments, or overseas portfolios that offer no benefit to domestic tax collections. With that said, we believe it likely the municipal market will be altered in some way. Several administrations dating back to Nixon tried to reform the municipal market. The Reagan tax cuts altered the taxation of private activity bonds. President Obama also floated capping the tax benefit on municipal bonds at 28%. The first Trump tax cuts eliminated tax-exempt advanced refundings. We derive comfort from the fact that while many presidents have tried, we are still here offering our clients substantial tax-advantaged income.

The new administration has announced several plans that could have large impacts for the municipal bond market. From a credit perspective, our primary concern relates to spending cuts to help offset the effect of extending the TCJA. Based on the current budget blueprint, Medicaid appears to be the primary target, facing $880 billion in spending reductions over 10 years. The healthcare sector has faced numerous challenges over the past few years and reductions to federal funding will slow, if not reverse, their recovery. A reduction in Medicaid coverage would result in lower revenues and lower collection rates. We have positioned cautiously in the hospital sector as risk-adjusted yields generally fall short of our requirements. We also expect higher education to be affected, but our exposure is limited for similar reasons. On the table are proposed cuts to research funding, restrictions on tax-exempt bond issuance, and an increase in the endowment tax. We believe these challenges are manageable with prudent financial planning.

Up until the recent election, municipal credit had broadly benefited from federal fiscal largesse, but changes are looming. Traditional credit valuations still reflect a “priced-to-perfection” world. This implies not only a hope that fundamentals will stay strong, but also that investor greed persists to squeeze every basis point of yield from the market. We prefer to be more selective. Staying flexible and building portfolios one bond at a time with high-quality credits that provide attractive yield is at the heart of our mission. Despite low spreads on bonds with generic structures, during first quarter 2025 we invested in a wide range of opportunities with less traditional structures that offered healthy spreads. These purchases enhanced existing portfolio exposures in prepaid energy, housing, and airport bonds, among others.

Specifically, we purchased prepaid energy bonds backed by the regulated insurance arm of Athene at a spread of over 150 bps. This is well beyond our purchase threshold and wider than Athene’s structurally weaker holding company’s taxable corporate bonds. We added Freddie Mac-guaranteed low-income, multifamily housing backed bonds with spreads between 80 and 140 bps, depending on maturity. We also invested in a range of State Housing Finance Authority bonds with four-to-six-year average lives and spreads around 100 bps versus generic triple A-rated municipals. Lastly, we added a new position in Los Angeles International Airport (LAX) late in the quarter. Airports represent about 15% of our portfolio holdings, and our airport credits often benefit from near monopoly power. Furthermore, LAX has among the best carrier diversity of any airport in the United States, which means it is not overly reliant on service from one airline, and it also enjoys strong liquidity.

We remain excited about the income potential of our portfolios and the opportunities on offer but remain cognizant to the risk that markets could once again come undone. There is no shortage of economic and political uncertainties that could lead market conditions to change suddenly. Our job is not to predict these changes, but rather to react appropriately and capitalize on them. Investors’ positive sentiment will eventually turn, and we are likely past the high-water mark for credit, so we are staying on our toes. With longer-term yields nearing their peak of 2023, the municipal market offers compelling value for our clients. We strive to stay blind to the distractions from the hope and fear outside and remain focused on finding securities that satisfy our conservative investment criteria.

| Performance As of March 31, 2025 |

|||||||

|---|---|---|---|---|---|---|---|

|

Total Returns |

Average Annual Total Returns |

|||||

Composite/Benchmark |

3 Mo. |

YTD |

1 Yr. |

3 Yr. |

5 Yr. |

10 Yr. | Since Inception |

BBH Municipal Fixed Income Composite (gross of fees) |

0.65% |

0.65% |

3.03% |

3.04% |

1.97% |

2.57% |

3.62% |

BBH Municipal Fixed Income Composite (net of fees) |

0.58% |

0.58% |

2.77% |

2.78% |

1.72% |

2.32% |

3.36% |

Bloomberg 1-10 Yr. Municipal Bond Index |

0.70% |

0.70% |

1.99% |

2.03% |

1.28% |

1.80% |

3.14% |

Returns of less than one year are not annualized. BBH Municipal Fixed Income inception date is 05/01/2002. |

|||||||

| Past performance does not guarantee future results. Sources: BBH & Co and Bloomberg | |||||||

| Representative Account Top 10 Obligors As of March 31, 2025 |

|

|---|---|

South Carolina Mortgage Revenue Bonds |

2.8% |

Salem-Keizer School District #24J, OR |

2.5% |

Texas Department of Housing and Community Affairs Single Family Mortgage Revenue Bonds |

2.3% |

Illinois Housing Development Authority |

2.3% |

Central Plains Energy Project Gas Project Revenue Bonds Project No. 5 Series 2022 |

2.2% |

Houston Airport Enterprise, TX |

2.2% |

Grossmont Healthcare District |

2.1% |

Texas Municipal Gas Corporation II |

2.1% |

New Mexico Mortgage Finance Authority |

2.1% |

Salt Verde Financial Corporation |

2.1% |

Total |

22.7% |

| Sources: BBH and Bloomberg | |

1 Basis point (bp) is a unit that is equal to 1/100th of 1% and is used to denote the change in price or yield of a financial instrument.

Risks

There is no assurance that a portfolio will achieve its investment objective or that the strategy will work under all market conditions. The value of the portfolio can be affected by changes in interest rates, general market conditions and other political, social and economic developments. Each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market.

Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, maturity, call and inflation risk; investments may be worth more or less than the original cost when redeemed.

Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

The Strategy also invests in derivative instruments, investments whose values depend on the performance of the underlying security, assets, interest rate, index or currency and entail potentially higher volatility and risk of loss compared to traditional stock or bond investments.

As the Strategy’s exposure in any one municipal revenue sector backed by revenues from similar types of projects increases, the Strategy will become more sensitive to adverse economic, business or political developments relevant to these projects.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. IM-16345-2025-04-07

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE MONEY