Each client’s goals and values are at the center of every Brown Brothers Harriman (BBH) Private Wealth Management relationship. Only by understanding our clients and their families, values and goals can we create a wealth and investment plan that is designed to help them to achieve their unique definition of success. Through our work with families, we have found that many clients seek to incorporate their core values not just in philanthropy and wealth planning, but also their investment portfolio. For these clients, BBH offers sustainable investing.

What is sustainable investing? BBH uses the following definitions to describe the sustainable investment landscape and our solutions for clients and their families, as the nomenclature across the industry varies.

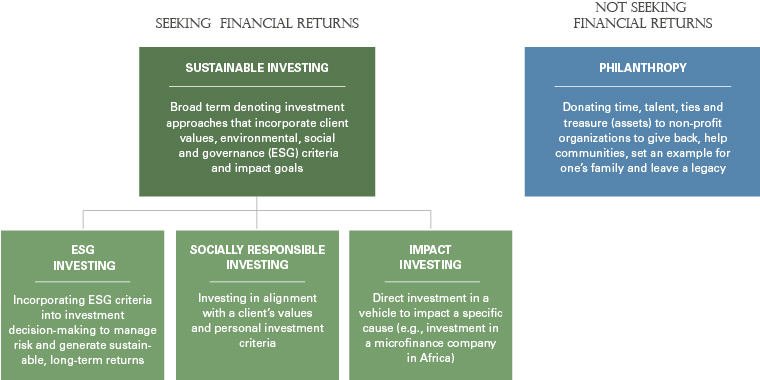

This graphic shows how BBH defines sustainable investing, as the nomenclature across the industry varies.

Seeking Financial Returns

Sustainable Investing: Broad term denoting investment approaches that incorporate client values, environmental, social and governance (ESG) criteria and impact goals

ESG Investing: Incorporating ESG criteria into investment decision-making to manage risk and generate sustainable, long-term returns

Socially Responsible Investing: Investing in alignment with a client’s values and personal investment criteria

Impact Investing: Direct investment in a vehicle to impact a specific cause (e.g., investment in a microfinance company in Africa)

Not Seeking Financial Returns

Philanthropy: Donating time, talent, ties and treasure (assets) to non-profit organizations to give back, help communities, set an example for one’s family and leave a legacy

Environmental, social and governance (ESG) investing occurs when a set of nonfinancial environmental, social and governance criteria contributes to qualitative research used to manage risk and identify sustainable businesses in the security selection and portfolio construction process. We believe BBH’s investment philosophy naturally aligns with the core tenets of ESG: BBH employs active, bottom-up, fundamental research to identify what we believe to be businesses with superior corporate governance, a strong relationship with all stakeholders, policies that lead to a judicious use of resources and management teams with the highest integrity and ethical standards.

ESG investing is a “values agnostic” undertaking; however, we recognize that a client’s values should ultimately shape her definition of what it means to invest responsibly. Socially responsible investing (SRI) addresses clients’ desires to incorporate their unique values into their portfolios. Naturally, SRI means different things to different people, and as a result, we seek to partner with our clients to first identify their unique values and objectives and to then work with them to customize portfolios to meet their individual needs. Impact investing takes values-based investing a step further and seeks to use capital to directly impact a cause that clients support.

By working with clients to define and communicate their values, we help them create and execute on philanthropic and sustainable investment plans aligned with their unique objectives. In the article that follows, we offer eight principles that help guide our own thinking about sustainable investing and how we incorporate those beliefs into client portfolios.

1. Bottom-up fundamental investing executed properly is consistent with ESG investing.

We believe that investors who successfully build portfolios from the bottom up, employ rigorous fundamental research and have a quality bias ultimately construct a portfolio in which many of their investments meet ESG criteria, as this process typically identifies companies that have strong business models, corporate governance and relationships with all stakeholders.

BBH’s comprehensive qualitative approach to security and manager selection drives the makeup of our clients’ portfolios and orients them toward environmentally sustainable, socially minded and appropriately governed businesses. In the end, our long-term fundamental investment philosophy narrows a broad investable universe to a select number of exceptional businesses that meet rigorous qualitative criteria. This results in a portfolio that is consistent with high ESG investment standards.

| BBH Investment Philosphy | Alignment with ESG Investing |

|---|---|

|

ESG investing implicity involves active management through the active development, by the investor, of financial and personal criteria. |

|

ESG investing requires bottom-up fundamental research and a quality bias. To determine each company's fit with ESG criteria, investors much understand a company's business model, corporate governance and key stakeholder relationships. |

|

The concepts of long-term ownership, value orientation and a capital perservation focus do not conflict with ESG investing. |

2. Identifying businesses that compound capital through a market cycle steers investors toward sustainable firms.

It is our view that high-quality businesses that meet our qualitative and quantitative criteria are better positioned to compound capital through a full cycle. As a result, we typically avoid businesses with the following characteristics: excessive leverage, high capital expenditure requirements and revenue models reliant on hard-to-predict commoditized goods. Consequently, our clients’ portfolios tend to have limited exposure to energy exploration and production (E&P), coal or other asset-heavy businesses. Additionally, we seek to invest with businesses that efficiently manage their assets and resources, which reduces operational costs, drives better economic returns and reduces business risk.

3. Focusing on key stakeholder relationships helps identify firms with excellent social practices.

Similarly, our investment criteria focus on the important stakeholders that engage with our portfolio companies, including their employees and communities broadly. We believe a company that invests in its brand, customers and communities creates a virtuous circle of behavior. For example, a business that focuses on its employees creates better outcomes for all its constituents. Better outcomes lead to market share gains and pricing power. Market share gains and pricing power lead to better economics for the business. Better economics often lead to further investment in employees. Ultimately, a business that focuses on its employees and customers expands its competitive moat, resulting in long-term sustainability of the business.

4. Identifying businesses that make effective management decisions leads to companies with strong governance.

Understanding what motivates management decisions is arguably one of the most important components of the research process for any long-term fundamental investor. Examining how the board, C-suite and management are incentivized and how compensation is structured, understanding whether the company has a strong corporate culture, identifying whether the management team is transparent and forthright in its communication with investors, employees and customers and determining if management decisions today will positively affect the future success of the business and related stakeholders all assist in identifying ethical companies with strong corporate governance.

5. ESG investing does not mean investors must sacrifice returns.

It is important to note that when choosing ESG investing, investors are not giving up returns simply because they select such an investment approach. Rather, they are adding qualitative factors to their fundamental investment criteria, which are aimed at identifying excellent businesses that generate sustainable shareholder value. In fact, we believe that because our investment approach is anchored in investing in sustainable companies, our clients’ portfolios benefit over time.

6. Values must drive a client’s socially responsible investment plan.

Individuals and organizations have different values, experiences and priorities. At BBH, we believe that SRI should not be a one-size-fits-all exercise and that defining one’s values is a critical step in determining success. To help clients express their values in their investment portfolios, we begin with a series of questions to understand their specific SRI objectives, as they can be different depending on the individual. For example, thoughtful people can have differences of opinion on social topics, such as nuclear power, and those definitional issues can lead to different portfolios. As such, having a deep-dive conversation with each client on values and goals is a key component to tailoring our approach. Through this exercise, we seek to construct an investment plan that is designed to help achieve each client’s unique definition of success.

7. Impact investments must make a “positive, measurable social and environmental impact alongside a financial return.”

The term impact is sometimes used indiscriminately in the marketplace; however, we believe that in order to make an impact investment, an investor must truly make a positive, measurable difference. The types of impact these investments can make are diverse and can include everything from increased availability of safe drinking water to access to capital for low-income entrepreneurs. In most cases, to make a positive, measurable impact, investors must invest in the private markets. Though not impossible, it is rare to find a public market equity fund that is truly making an impact based on the Global Impact Investing Network definition (above in quotes).

8. Philanthropy can also be an excellent way to make a “positive, measurable social and environmental impact,” though it does not generate a financial return.

For those seeking to create a positive impact, we recommend that philanthropy play a role in the plan. First, for some very specific causes like protecting certain endangered species, philanthropy is the only option, as most impact funds do not invest in such granular themes. Second, and most importantly, depending on the cause a client wants to support and the opportunity set on offer to do so, philanthropy may be a more effective way to make the impact most important to that client. When discussing sustainable investing with our clients, we typically will also raise the topic of philanthropy in an effort to take a more holistic approach to aligning our clients’ goals with their values.

How we work with clients to implement their philanthropic and sustainable investment plans

BBH’s investment philosophy and manager selection process naturally results in an investment platform that includes managers who implicitly incorporate ESG factors into their security selection process, and we report on this alignment over time. When we begin working with clients, BBH seeks to define and understand a client’s values and the related objectives for her wealth, including the goals of her investment portfolio, by deploying our proprietary values-based planning and socially responsible investing tools and methodologies. A client’s discrete set of values and goals are imbued into their sustainable investment portfolio to create a truly unique offering for each client.

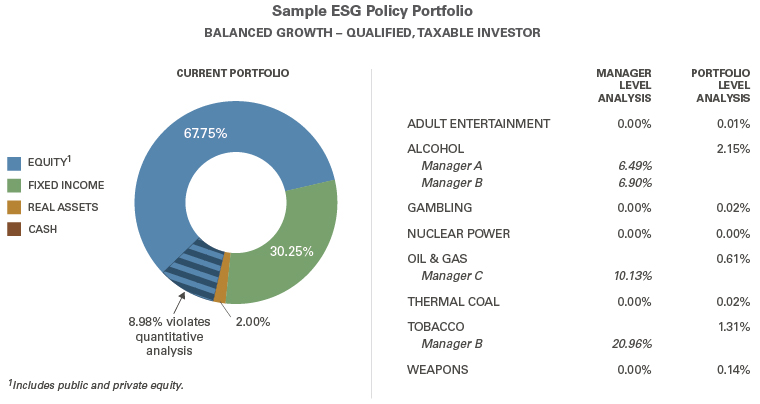

As follows is an example of a taxable investor seeking to grow wealth over time in a sustainable investment portfolio, with income and liquidity as secondary considerations. After extensive conversations with a client, we learned that her custom sustainable investment portfolio would include investment strategies aligned with ESG and no meaningful exposure to oil and gas, coal, nuclear power, weapons, tobacco, adult entertainment and alcohol. Through discussions with the client, we defined meaningful exposure as any manager deriving over 5% of total revenues from their underlying holdings. From there, BBH created a taxable, balanced growth portfolio with underlying managers whose approaches aligned with ESG and did not include equities and issuers with more than 5% of their total revenues derived from the aforementioned specific themes included in our proprietary strategies and among our external managers’ holdings, which represent the 9% shaded section of the nearby chart. We then reallocated capital to other investments that met our client’s needs. The resulting portfolio was a sustainable investment portfolio that aligned with our client’s objectives. We follow a similar process for all clients seeking sustainable portfolios and customize according to each client’s unique objectives.

This graphic shows a sample ESG policy portfolio for a balanced growth, qualified, taxable investor.

The left-hand side shows an asset class breakdown, which is as follows:

Equity (public and private equity): 67.75% -- 8.98% (a portion of the equity portion) violates the quantitative analysis

Fixed Income: 30.25%

Real Assets: 2.00%

Cash: 0.00%

The right-hand side shows an analysis of the exposure to different stocks in industries that typically do not align with ESG on both a manager and portfolio level. The following lists the exposure for each:

Adult Entertainment: 0.00% (Manager Level), 0.01% (Portfolio Level)

Alcohol: 6.49% (Manager A), 6.90% (Manager B), 2.15% (Portfolio Level)

Gambling: 0.00% (Manager Level), 0.02% (Portfolio Level)

Nuclear Power: 0.00% (Manager Level), 0.00% (Portfolio Level)

Oil & Gas: 10.13% (Manager C), 0.61% (Portfolio Level)

Thermal Coal: 0.00% (Manager Level), 0.02% (Portfolio Level)

Tobacco: 20.96% (Manager B), 1.31% (Portfolio Level)

Weapons: 0.00% (Manager Level), 0.14% (Portfolio Level)

Conclusion

Sustainable investing is a complicated topic with many considerations, and this document merely provides an overview of its many facets, how BBH offers it to clients and what our key beliefs are surrounding it. Ultimately, sustainable investing is not a product, but an approach. There is no one-size-fits-all solution, and individuals who choose to pursue this approach must be committed to the required work and ongoing conversation it entails. In summary, investors must understand the methodologies used to construct their portfolios to ensure an outcome that aligns with their personal values and expected investment returns.

Contact Us

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-06525-2023-07-06