When U.S. Presidential Climate Envoy John Podesta recently called for a “21st century trade policy” that encourages a “race to the top for climate action”,1 it was clear that he meant business. He asserted carbon pricing would help limit emissions and China’s dominance of key industries, showing the approach’s growth in policy response to climate change.

However, carbon pricing is not without its challenges.

What is Carbon Pricing?

Carbon pricing is an approach to emissions reduction that attempts to pass on the cost of polluting directly to emitters of Greenhouse Gases (GHG), primarily carbon dioxide and to a lesser extent methane, nitrous oxide, and fluorinated gases. Direct carbon pricing can take multiple forms including carbon taxes, emissions trading schemes (ETS), and carbon crediting mechanisms. Indirect carbon pricing includes taxes and subsidies that change the price of inputs, most ubiquitously fuel excise taxes. Carbon pricing can be viewed as an attractive policy option in that they are relatively straightforward to administer and give the option of raising public revenues.

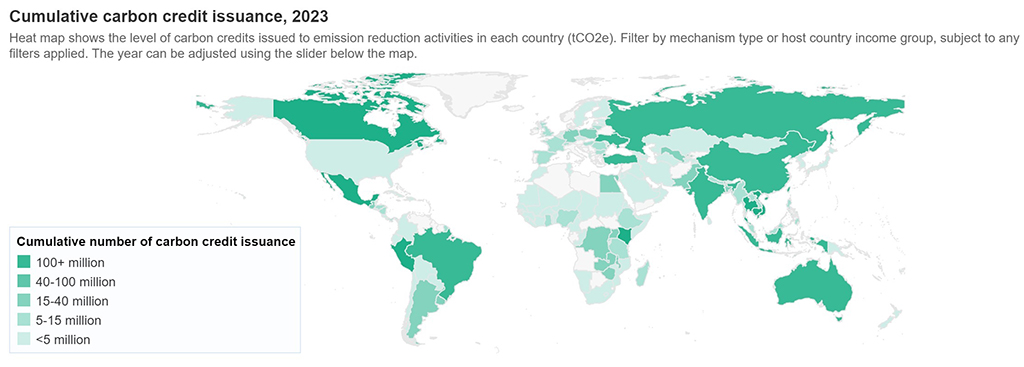

Carbon pricing has existed for decades, one such example being the sulfur dioxide cap-and-trade system implemented in the U.S. in the 1990s. The 2015 U.N. Paris Climate Agreement, however, required signatory countries to establish Nationally Determined Contributions (NDCs), or goals for reducing GHG emissions over a specified time horizon. This advent of NDCs – 120 countries have established these - has accelerated the adoption of carbon pricing as well as the creation of markets in which abatement and other carbon credits are traded.

|

As with any tax, carbon pricing can impact inflation and therefore macroeconomic performance; their adoption at a national level also creates incentives and disincentives for countries to implement carbon pricing from a competitive standpoint.

Considering such challenges, the full economic impact of carbon pricing is understood by analyzing the current mechanisms, identifying upcoming events in the evolution of carbon pricing infrastructure, and exploring the data around the macroeconomic impact of carbon pricing where implemented.

1) Today’s carbon pricing mechanisms include carbon taxes, emissions trading schemes (ETS), and carbon crediting mechanisms (CCM).

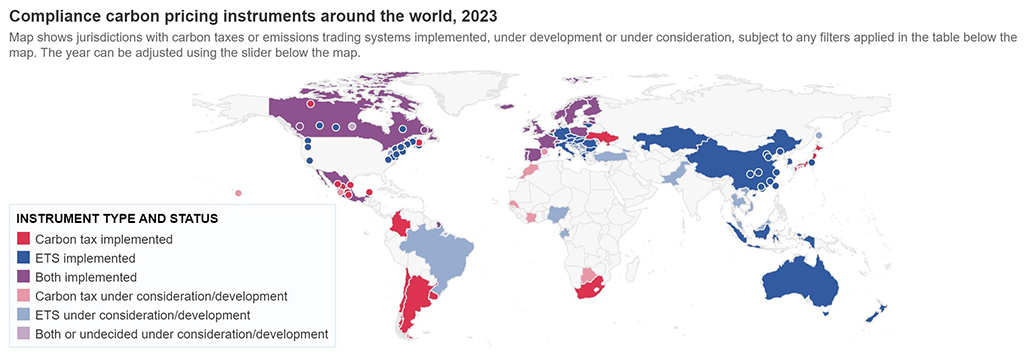

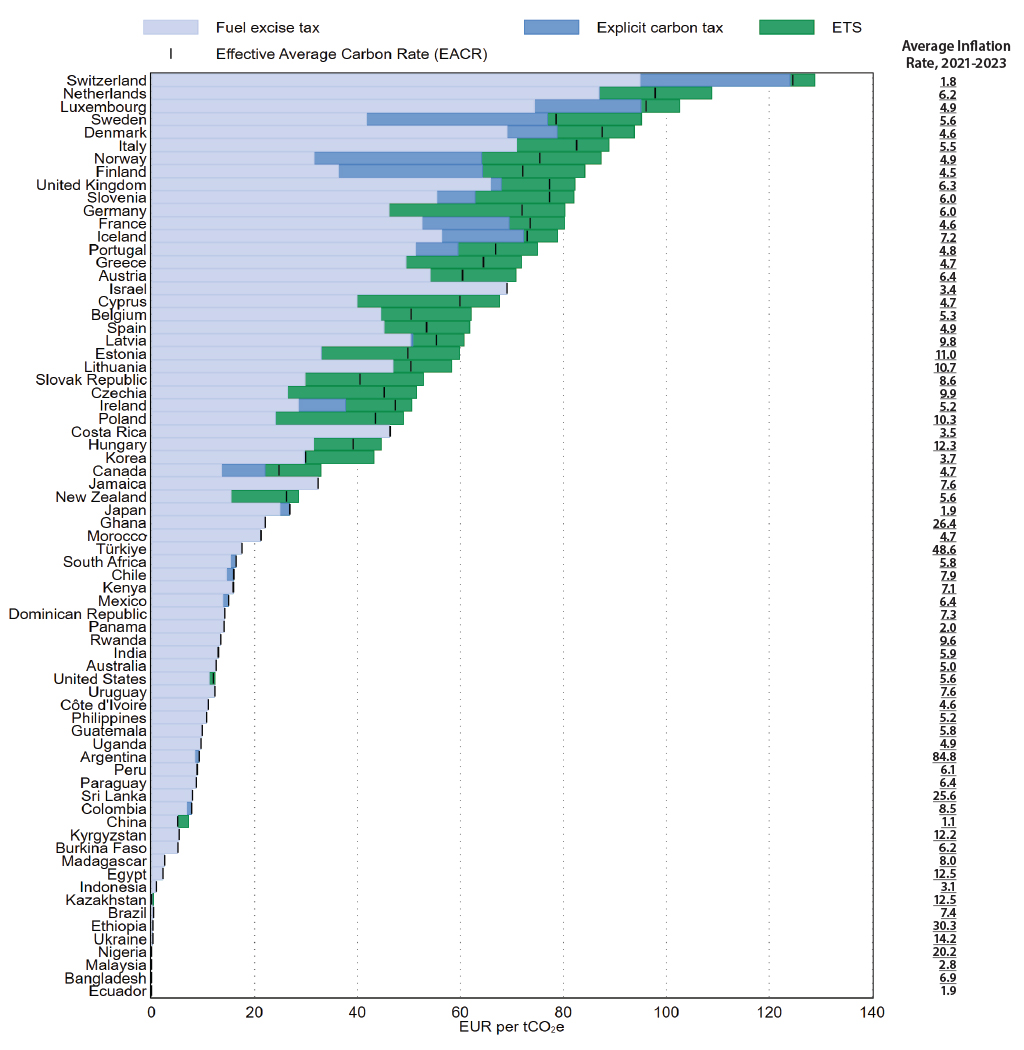

Carbon Taxes: 37 Carbon Tax programs have been implemented globally at national and subnational levels, covering 5% of global GHG emissions. Prices range from $0.41/tonne of Carbon Dioxide (tCO2) in Mexico to $155/(tCO2) in Uruguay, and with several Scandinavian and Western European countries having prices over $80/(tCO2). Average tax across the 37 programs is $25.38/(tCO2). Such taxes generate approximately $30 billion in government revenues globally.

Emissions Trading Schemes (ETS): 37 Emissions Trading Schemes have been implemented globally at national and subnational levels, covering 18% of global GHG emissions. Pricing ranges from $1.12/(tCO2) in the Kazakhstan ETS to $96.29/(tCO2) within the EU ETS; average price amongst all 37 ETS is $25/(tCO2) and 10 of the 37 ETS are Canadian Federal or Provincial programs. These ETS generate approximately $67 billion in government revenues globally.

Figure 1: Direct Carbon Taxes and ETS Implemented and Under Consideration/Development Globally, 2023: