Let’s take a closer look at three regional scenarios.

1. U.S. ETF Settlements

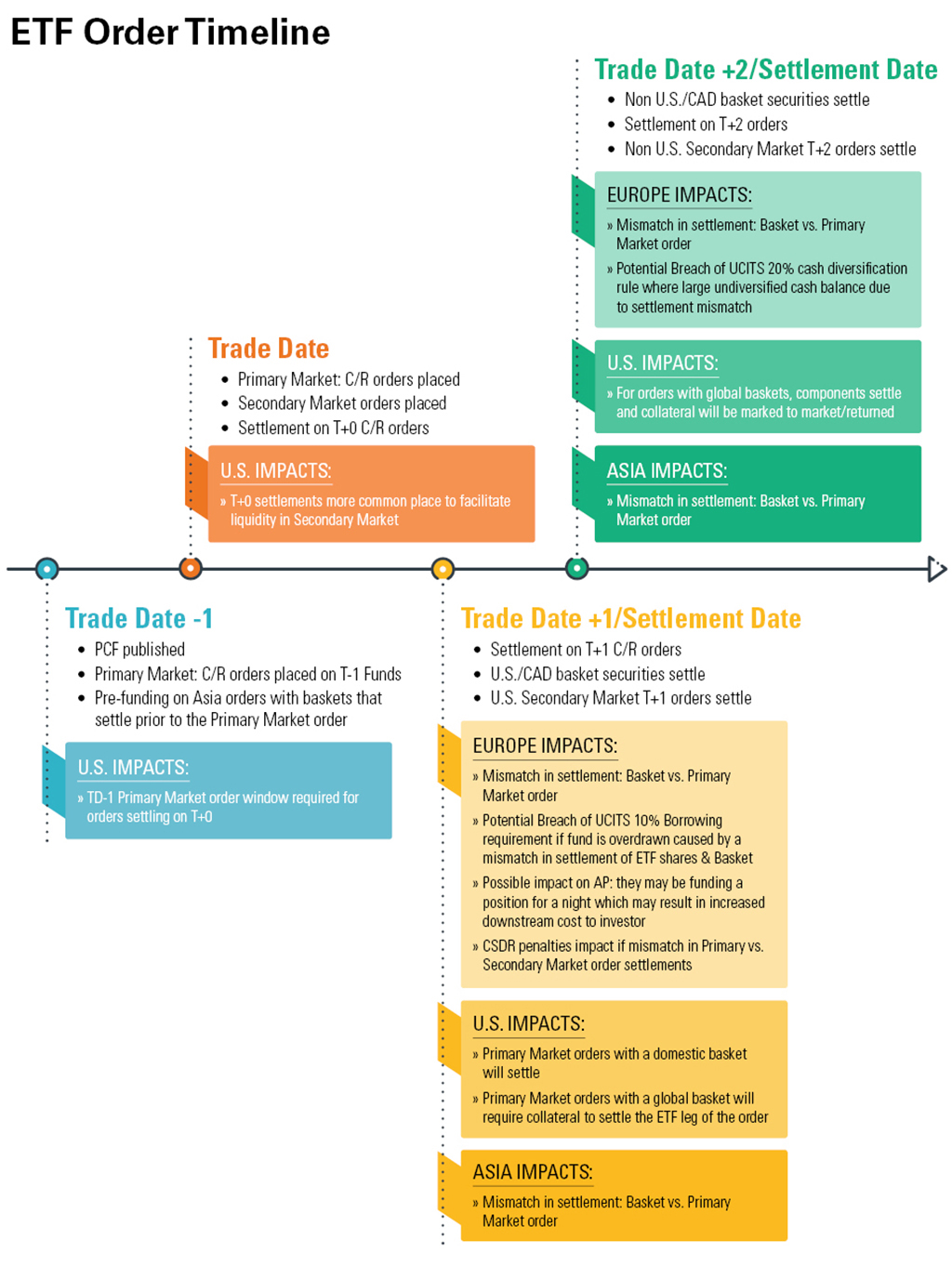

As the driving force behind the move to T+1, the U.S. market will experience the greatest impacts and market participants will need to navigate several potential associated challenges. Since the transition in 2017 to T+2 settlement, ETFs have gained numerous efficiencies that may be further enhanced by condensing to T+1.

Fortunately, the National Securities Clearing Corporation’s (NSCC) Continuous Net Settlement (CNS) mechanism, which supports the clearing and settlement of ETFs with U.S. securities, will greatly streamline the process, due to the inherent operational efficiencies and settlement guarantee.

Creation and redemptions will become more complex for U.S. ETFs with global holdings, which settle outside the NSCC’s CNS infrastructure.

Additionally, where secondary market trading requires creation activity to support shortened settlement, ETF sponsors and APs will need to support a T+0 creation process. This will allow for ETF shares to be created in the primary market and onward delivered to satisfy secondary market trading obligations.

2. European ETF Settlements

In Europe, trading and settlement happens across 35 exchanges and 31 central securities depositories. Since most exchanges settle ETF share activity on a T+2 cycle, primary market activity - ETF creations and redemptions with the fund - may need to consider a move to T+1 settlement if a majority of the securities held in the portfolio are from the U.S. or Canada 3

UCITS rules restrict how much cash a portfolio may hold with any one institution to 20% of net assets and borrowing is limited to 10% of net assets. Mismatches in settlement may result in breaches of these UCITS rules where a substantial portion of the basket settles on T+1 and primary orders settle on T+2.

How this impacts AP’s and Market Makers needs to be considered. They may be faced with additional costs and increased risk where there are differences between primary and secondary market settlement cycles, ultimately impacting their pricing model and hence the spreads on the funds.

3. Asian ETF Settlements

The shift to T+1 will be most impactful in Asia for regional asset managers that lack U.S. time zone coverage. Many regional asset managers are familiar with shortened settlement cycles when investing into markets like China where the standard is T+0 settlement. As a result, many firms have already adopted practices like pre-funding to manage the settlement mismatch between the underlying investments and the primary market.

Asia-based managers will need a coverage model which accounts for U.S. business hours, where they can monitor and amend their trade instructions during the Asia evening of T+1, if the trades are not matched with their counterparties.

The use of pre-funding will likely expand, as ETF baskets with U.S. or Canadian securities will now come into scope.

Action steps to take

In preparation for U.S. T+1, ETF managers should review their current workflows and timings around order settlement and portfolio trading. Some areas of focus include:

- Assess the impact of the condensed settlement timeline on investment tasks such as reconciliations, trade, and FX settlement instructions

- Evaluate the implementation of trade affirmations, to reduce the risk of fails

- Engage with APs and Market Makers on any product-specific considerations

- For all non-U.S. ETFs, assess on a fund-by-fund basis the impact on primary market order activity of Canadian and U.S. securities moving to a T+1 basis – to identify where a move to T+1 settlement is required for creations and redemptions

- Where identified, plan for European prospectus supplement amendments to reflect changes from T+2 to T+1 for primary market orders

- Update U.S. prospectuses to reflect T+1 on create/redeem orders

- Consider how to support T+0 create/redeem activity in the primary market in the U.S.

For more information and practical insights contact Antonette Kleiser, Chris Pigott, John Hooson, or your BBH Representative.