This is impressive in percentage terms, but the size of these smaller Asian markets – even if combined – pales in comparison to China. This data argues that the real winners of the U.S.-China trade war, so far, are those markets that are benefiting from shifting trade patterns.

On August 1, President Trump, unhappy with the pace of negotiations, threatened to levy a 10% tariff on a further $300 billion of Chinese imports as of September 1, in addition to the $250 billion of Chinese imports already subject to a 25% tariff. This imposes tariffs of 10% or 25% on essentially all Chinese exports to the United States.

What needs to change to resolve this dispute? First, the White House would like to negotiate updated trade agreements that reflect China’s current participation in the global economy. As China emerged from economic isolation 50 years ago, trading partners agreed to generous terms of trade in order to foster this evolution. The White House is right to conclude that China no longer needs the same degree of foreign encouragement in 2019 and wants trade agreements to acknowledge this current reality.

On a related topic, President Trump is demanding that China open its markets more fully to American exports, particularly in the areas of financial services and automotives. There are 1.4 billion people in China with a GDP per capita of $15,000. This represents a growing demand for things like automobiles, savings accounts and insurance policies that the United States wants to help meet. China is making progress on these fronts, albeit at a measured pace. Earlier this year, Premier Li Keqiang promised that China is “quickening the full opening of market access for foreign investors in banking, securities and insurance sectors,” but the “quickness” of this reform falls short of American expectations so far.

A final broad issue is better protection of intellectual property. China has long been accused of pilfering U.S. technology by insisting on joint ventures in critical sectors, obtaining sensitive technology from JV partners, and then using that technology elsewhere. Here, too, China has made gradual progress. In December 2018, China issued a list of 38 specific punishments for Chinese companies that steal proprietary technology from business partners, including restricted access to financing. As part of that announcement, China explicitly acknowledged U.S. concerns for the first time: “The release of the memo, one of the most detailed documents on intellectual protection issued by China, signals a further step by China to strengthen IPR protection and shows China’s sincerity in addressing American concern over the issue.” To make the point even clearer, the Chinese memorandum continues, “It could be useful as part of the U.S.-China trade discussions, but this is not a direct reaction to pressure from the U.S.”

The good news is that the direction of reform in China is consistent with U.S. demands. The bad news is that change moves slowly in a 4,000-year-old nation. Committing to reform is one thing. Implementing and monitoring it is another.

The pace of change (or lack thereof) is a driving force in trade negotiations, due in no small part to the U.S. election cycle. Economically, the United States holds the stronger hand in negotiations. Trade is a large part of the Chinese economy, so the U.S. can theoretically exert more economic pain on China than China can on the U.S. through the imposition of tariffs. Politically, however, the advantages are reversed. Whereas the American president has to face an election every four years and is term limited from more than eight years in office, Chinese President Xi Jinping faces no such constraint on his leadership. China can wait out the current U.S. administration – even at the cost of short-term economic pain – and hope for a more malleable successor.

Domestically, prolonged trade friction is a double-edged sword. On one hand, addressing the imbalance of trade with China is as close to a bipartisan issue as can be found in Washington these days, and President Trump’s supporters generally applaud his approach to China. And, with other sectors of the economy doing well, the United States can afford some pain in export markets as China retaliates with tariffs of its own. The domestic unemployment rate is low, wages are rising, inflation is subdued and financial markets are near all-time highs.

On the other hand, the uncertainty of prolonged trade disruption does pose a risk to the broader economy, which informed the Federal Reserve’s decision in late July to lower interest rates by 25 basis points and accelerate the end of balance sheet adjustments. In the absence of the risks to the global economy posed by trade disputes, there is simply no rationale for the Federal Reserve to ease monetary policy. Traders have concluded that there is more to come. In the wake of the Fed’s action in late July, futures markets placed the probability of another interest rate cut in September at more than 90%.

What Next?

The politics on both sides of the negotiating table imply that this conflict can be resolved. President Trump wants a victory headed into the 2020 election, as would any candidate for re-election, and China knows that it has enjoyed the benefit of outdated trade agreements for far too long. We are encouraged by the steps that China has taken to address U.S. concerns, while recognizing that the pace of progress falls short of U.S. demands. Our optimism, however, is tempered by the recognition that mistakes happen in tense situations. We see three scenarios in which the present trade environment might deteriorate to the detriment of the U.S. economy.

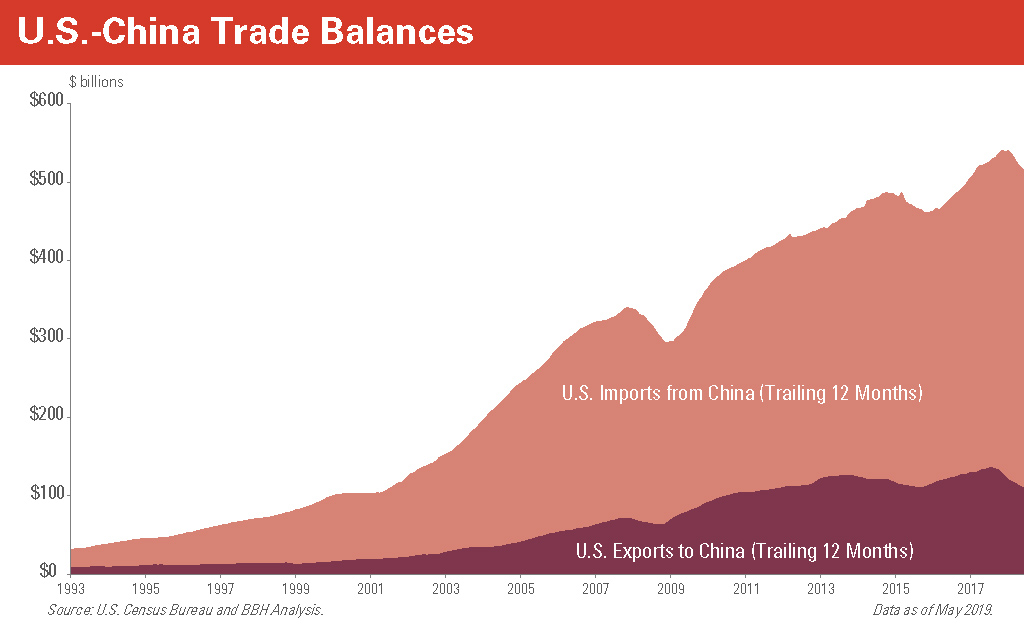

First, current tensions could both escalate and broaden, and arguably we are already experiencing this. Within hours of President Trump’s August 1 announcement that the U.S. would levy tariffs on all Chinese exports as of September, China promised to retaliate without offering any specifics. The imbalance of trade makes it hard for China to match U.S. tariffs proportionately, as the country’s $514 billion of annualized exports to us is far larger than our $110 billion of exports to it. This might prompt China to apply pressure to specific U.S. industries or companies in addition to broader tariffs. Technology companies are particularly wary of this risk. The U.S. has already engaged in targeted trade measures by placing severe trading restrictions on Huawei, a leading Chinese technology exporter. If the U.S. follows through and imposes tariffs on all Chinese exports, the risk of more targeted measures will increase. China could, for example, restrict the export of vital materials such as rare earth minerals, critical elements for technology manufacturing that are only found in China.

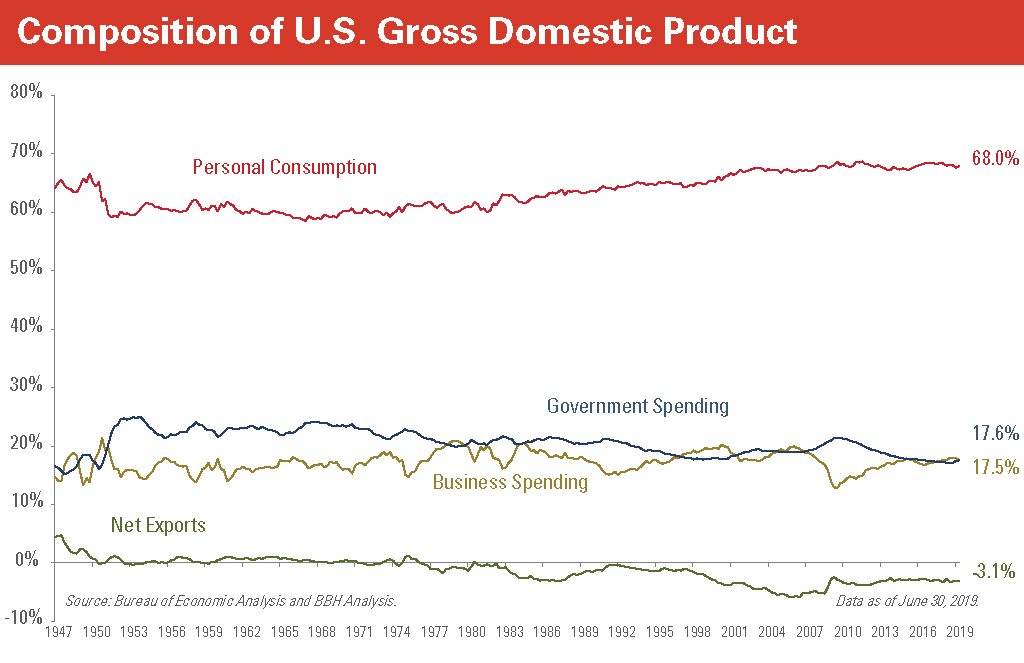

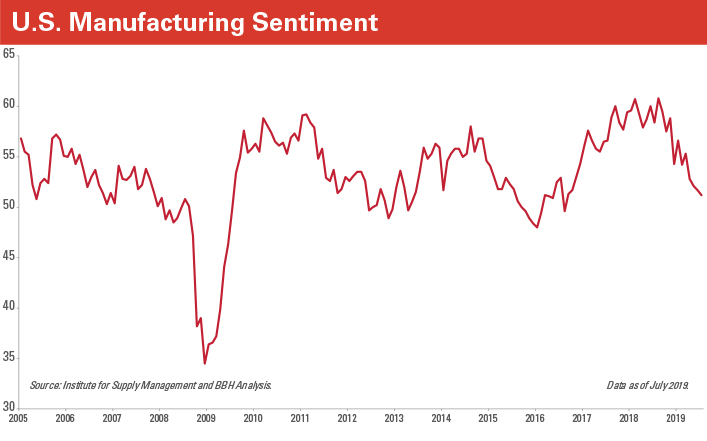

This possibility raises a second category of risks, namely that U.S. companies might rein in investment and spending in response to heightened uncertainty about trade. Not only does this pose a threat to the 17.6% of the American economy that is the business sector, but it potentially has implications for hiring and employment as well. There is some evidence that business sentiment has already shifted in response to trade uncertainty. As shown in the nearby graph, the Institute for Supply Management’s Purchasing Managers’ Index (PMI) declined to 51.2 in July, the weakest level since August 2016. Readings below 50 are historically associated with a downtown in economic activity.