Hiring a private wealth manager can seem like a complicated decision. This is especially the case for those who may not have a great deal of familiarity with the industry or investing. For anyone, it’s a decision that involves a number of considerations and often affects one’s entire family.

Questions abound, such as:

- Where do you start?

- How do you determine who is the right choice?

- What questions should you ask?

- What is truly important?

We interviewed three of the most senior relationship managers at Brown Brothers Harriman (BBH) to answer these questions. Here are the 10 most cited considerations for high-net-worth individuals – those with over $10 million in investable assets – though many of the points that follow are applicable to people with less wealth as well. Please note that the following list is not in order of importance, but rather in chronological order (though some considerations happen concurrently).

1. Trusted advisors or referral sources

Do you have capable, current advisors outside of private wealth management, such as a trusts and estates attorney or accountant? If so, consider using them as a source for creating a short list of private wealth managers to interview.

Other potential referral sources could be family or friends who may be able to recommend an advisor with whom they have personal experience. It is usually good practice to identify multiple providers and interview as many as necessary to determine who the right choice is.

2. Capabilities needed

Do you just have investment advisory needs, or do you have others as well, like wealth and estate planning, trust services, or borrowing? A private wealth manager’s core competencies should relate to investing and wealth planning, though some may offer other services that are also important to you.

If an otherwise strong private wealth manager lacks a service that is important to you, consider finding a separate provider, especially if it is likely that another firm is better or more efficient at providing the service in question. Private wealth managers often offer an array of solutions aimed at high-net-worth individuals like personal concierge, aircraft leasing , or art appraisal that are not related to investing or wealth planning. These offerings can sound alluring to some, but they should not be your wealth manager’s core competency; they should be the focus of companies that specialize in these services.

3. Your goals

“Goals” may be the most overused word in private wealth management – but it is an important one. Your goals determine:

- Risk tolerance

- Return objectives

- Income needs to support your current lifestyle

- Future liabilities

- Desire for liquidity

- Several other considerations

In other words, you must define success for yourself, given certain constraints specific to you and your assets. You may have a specific statement of your family’s mission or, like most, may need some help in bringing your priorities into focus.

Some private wealth managers will be better suited than others to help you and your family identify your most important objectives and carry out a plan to meet them given your financial situation, and you need to use your judgment to determine who those providers are.

4. Investment philosophy

Investment philosophy relates to goals, but there is a distinction: Goals generally refer to wealth planning (e.g., do you want to create a trust with certain assets to leave for your children?) and asset allocation (e.g., how do you and your advisors distribute assets between strategies with differing risk and return profiles to preserve and grow wealth or achieve income objectives?).

On the other hand, investment philosophy relates to the manner in which investors select investments and strategies to offer to clients. For example, at BBH, we believe in:

- Performing bottom-up, fundamental research on all investments so we know what we own and why

- Protecting first, then growing capital

- Only partnering with those we believe to be the world’s best third-party investment managers – no matter the investment, we insist on a consistent philosophy

Your private wealth manager’s approach must philosophically align with how you view the world. If you don’t have a strong viewpoint or philosophy before interviewing private wealth managers, it is still worthwhile to ask about investment philosophy and then consider whether the response is consistent with how you want to invest.

5. Service level

Determine how high your private wealth manager will prioritize his or her relationship with you by asking these questions:

- How many clients do you oversee?

- How often are you typically in contact with clients, and how frequently do you meet with them?

- How large (in asset dollars) is your total book of business, and what is the average relationship size?

- How many other professionals support you?

The answers to these questions will provide you with a deeper understanding of how much attention you will receive. It is important to note three points, however.

- First, more attention isn’t necessarily better – it depends on the needs of you and your family.

- Second, sometimes very senior wealth management professionals have junior team members who oversee relationships on a day-to-day basis. For that reason, it is often important to meet the entire team that will work with your family and understand how the relationship will be serviced.

- Third, some private wealth managers will be better at servicing larger numbers of relationships than others, so the answers to the prior questions will not necessarily tell the entire story.

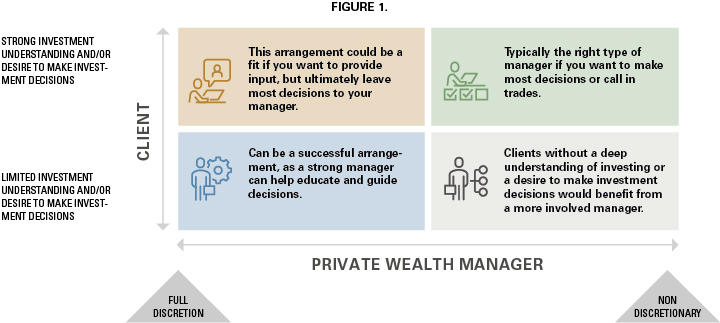

6. Involvement in investment decisions

At their core, private wealth managers provide investment advice.1 Therefore, you should consider how involved you want to be in investment decisions. Some clients have a deep understanding of investing or a strong desire to be involved in how their accounts are invested. Others have limited knowledge or limited time, so they want a private wealth manager with full discretion over investment decisions.2

These examples are the poles, however, and it is important to know where you fall in the spectrum within Figure 1.