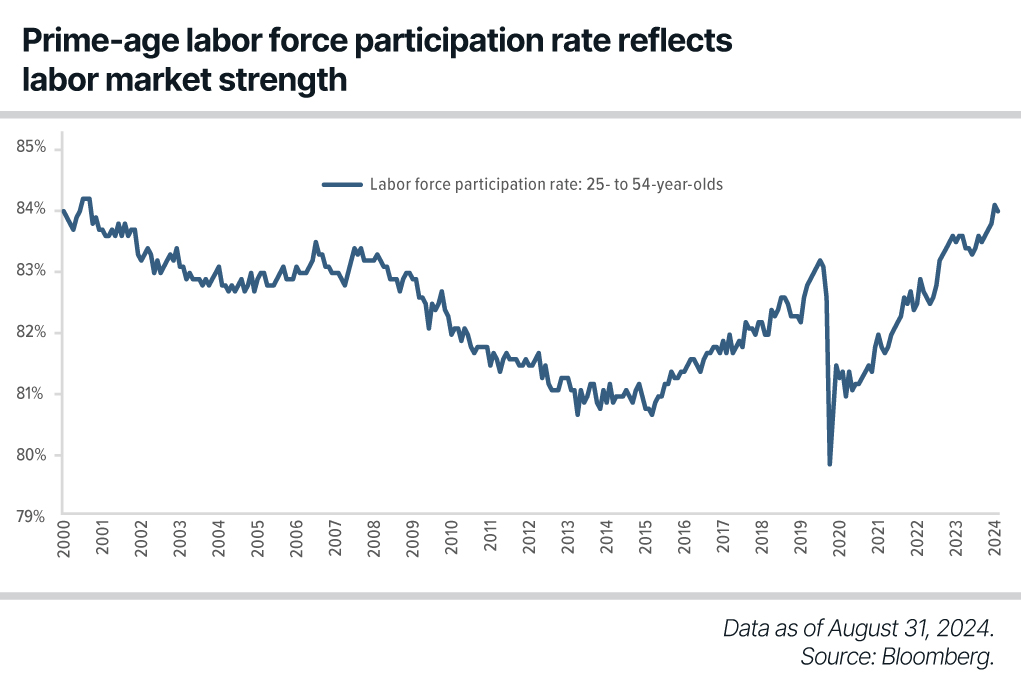

Chart showing the labor force participation rate of 25-54 year olds. The latest figure is 83.9%, as of August 31, 2024.

In each issue of Owner to Owner, we review aspects of the business environment on three fronts:

- Overall economy

- Credit markets

- Private equity (PE) and mergers and acquisitions (M&A) markets

The following article examines the state of the economy in the midst of rate cuts, continued caution from banks, and the growing influence of artificial intelligence (AI).

The Economy

According to the “third” estimate by the U.S. Bureau of Economic Analysis, U.S. real gross domestic product (GDP) expanded at a quarter-over-quarter annualized rate of 3.0% in second quarter 2024, topping the 2.9% estimate. This marks an acceleration from the 1.6% (revised upward from 1.4%) real GDP growth recorded in first quarter 2024, which reflected an upturn in private inventory investment and an acceleration in consumer spending.

The personal consumption expenditure (PCE) component of GDP – which drives 70% of GDP over the long run – advanced 2.8%, with increases in both services and goods. In addition, corporate profits rebounded sharply from the first quarter, which should help sustain the economic expansion.

Meanwhile, the U.S. unemployment rate remained above 4% for the fourth consecutive month. August’s reading of 4.2% marks its longest streak above 4% since the beginning of 2018 (excluding the COVID-19 pandemic period).

The increase in July’s unemployment rate (released on August 2, 2024) was a key driver of the August 5 market sell-off, in which the S&P 500 declined 3% and the VIX Index recorded its widest daily range ever, advancing to an intraday high of 65.7. This was its third highest level after the global financial crisis and the COVID-19 pandemic.

The rise in the unemployment rate over the last several months was driven by:

- A continued robust increase in the labor force, up 1.1 million since the end of 2023

- A rise in the labor force participation rate for prime-age workers (25- to 54-year-olds) to 83.9%, the highest level since 2001

The latter suggests that the labor market is in better shape than the unemployment rate indicates, as prime-age workers typically become discouraged and leave the labor force during a recession.

From 2024 to 2026, the Federal Reserve estimates real GDP growth of 2% annually, down from 2.9% (revised upward from 2.5%) real GDP growth rate in 2023. As such, the Fed does not currently forecast a recession over the next three years.

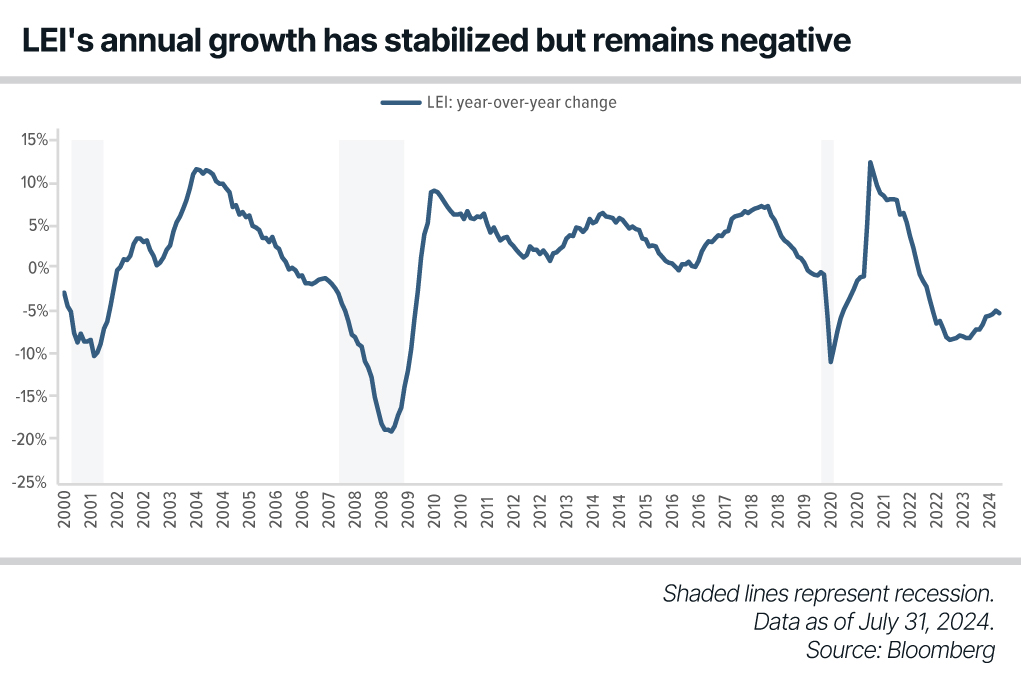

Turning to forward-looking indicators, we believe that The Conference Board’s index of 10 leading economic indicators (LEI) provides the most balanced, forward-looking gauge of economic activity. While many economic indicators display more noise than signal, the LEI has proved to be a valuable forecasting tool over multiple economic cycles.

In the prior three recessions (excluding the COVID-19-induced recession in 2020) that started in 1990, 2001, and 2007, the LEI began declining between 12 and 22 months prior to the start of the recession. As of July 2024, the LEI has declined for five consecutive months since recording a flat month-over-month reading in February 2024.

Despite the overall decline, four out of 10 leading indicators made positive contributions to the LEI in July. Nonetheless, a deterioration in new orders, softer building permits, and lower hours worked in manufacturing offset these improvements. As the magnitude of monthly declines has lessened, the LEI’s 12-month growth rate has continued to trend upward after bottoming in October 2023 but remains negative, suggesting downward pressure on economic activity ahead is probable.

Chart showing year-over-year change of the LEI. The latest figure is -5.2%%, as of July 31, 2024.

At the Fed’s annual policy conference in Jackson Hole, Wyoming, in August 2024, Chairman Jerome Powell stated that “the time has come for policy to adjust,” as inflation continues to trend toward the Fed’s 2% target and as the Fed does not seek further cooling in labor conditions. Indeed, in August, the U.S. Personal Consumption Expenditures (PCE) Price Index increased 2.5% year over year, its lowest level since early 2021.

This increase gave the Fed confidence that inflation is declining in a sustainable way toward its 2% target. As a result, the early August drawdown in the S&P 500 proved to be short-lived, with the S&P 500 advancing 2.4% in August and VIX Index falling sharply to end the month lower than July levels.

As it relates to monetary policy, in September the Federal Open Market Committee (FOMC) joined global central bank peers by beginning its interest rate-cutting cycle. The FOMC reduced the fed funds rate by 50 basis points (bps) to a target range of 4.75% to 5.0%.1 This marks the FOMC’s first rate cut since July 2019.

As of September 26, the fed funds futures curve is pricing in that the fed funds rate ends 2024 at 4.1%. This implies a target range of 4.0% to 4.25%, which is more ambitious than the Fed’s terminal rate guidance of 4.4% (implying a target range of 4.25% to 4.50%) estimated in its September 2024 economic projections release.

The difference between the Fed’s and investors’ estimates on the number of potential rate cuts in 2024 may result in elevated volatility in the near term and may impact equity prices, as real interest rates are likely to stay higher for longer than what is currently priced (equity multiples share an inverse relationship with real interest rates).

There is much underway as we progress through the remainder of 2024 – rising tensions in the Middle East, ongoing economic uncertainty in China, and the fast-approaching U.S. presidential election, to name just a few – and we will be watching inflation and global growth developments closely.

The Credit Market

Since the beginning of 2024, market participants have been uncertain about when and how quickly policymakers will adjust the federal funds rate. The widely referenced CME FedWatch tool showed significant fluctuations in the period leading up to the September 2024 FOMC meeting.

In the FOMC’s Survey of Primary Dealers and Survey of Market Participants, most respondents expected a 25-bp cut at September’s meeting, while futures prices implied a greater probability of a 50-bp cut. Though banking analysts, Fed presidents, and other experts suggested different opinions about the magnitude of the adjustments, investors could have turned to Rod Stewart, because, as the saying goes, “The first cut is the deepest.”

All FOMC governors, save one, ultimately decided to implement a more considerable 50-bp rate cut at its September 18 meeting. Chairman Jerome Powell described this decision as a “recalibration” of monetary policy, recognizing that the policy rate, currently at 4.75% to 5.00%, is still higher than the neutral rate. Importantly, Powell stated that the 50-bp cut was intended to support the economy’s current strength, rather than respond to significant economic weakness.

Chart showing U.S. two-, five-, and 10-year Treasury yields through September 30, 2024. The latest figures are 3.7%, 3.6%, and 3.8%, respectively.

While the FOMC will continue to use incoming economic data to assess the timing and pace of future monetary policy adjustments, which influence short-term rates, outlooks for future growth and inflation are more impactful on longer-dated Treasury yields. The long tail of high but short-term, pandemic-induced inflation and the Fed’s policy rates in response, combined with more modest, longer-term inflation and economic growth expectations from market participants, drove the two-year Treasury yield above the 10-year yield for the last two years – a scenario known as an inverted yield curve.

The overall impact of elevated but slowing inflation through the end of 2023 and into 2024 is shown in the above chart, where U.S. two-, five-, and 10-year Treasury yields on average shifted downward by approximately 132 bps from their recent October 2023 peak. Notably, in September 2024, the yield curves normalized, or un-inverted, as two-year Treasury yields continued to decline with falling inflation and the 50-bp Fed rate cut. Like the FOMC, the market will reflect expectations of the economy. However, the normalization suggests a more positive outlook or potential for a soft landing, as investors are willing to lock in higher rates for extended periods. Further, the 12-month Consumer Price Index (CPI) measured 2.4% in September, which may enable further rate cuts during the remainder of 2024.

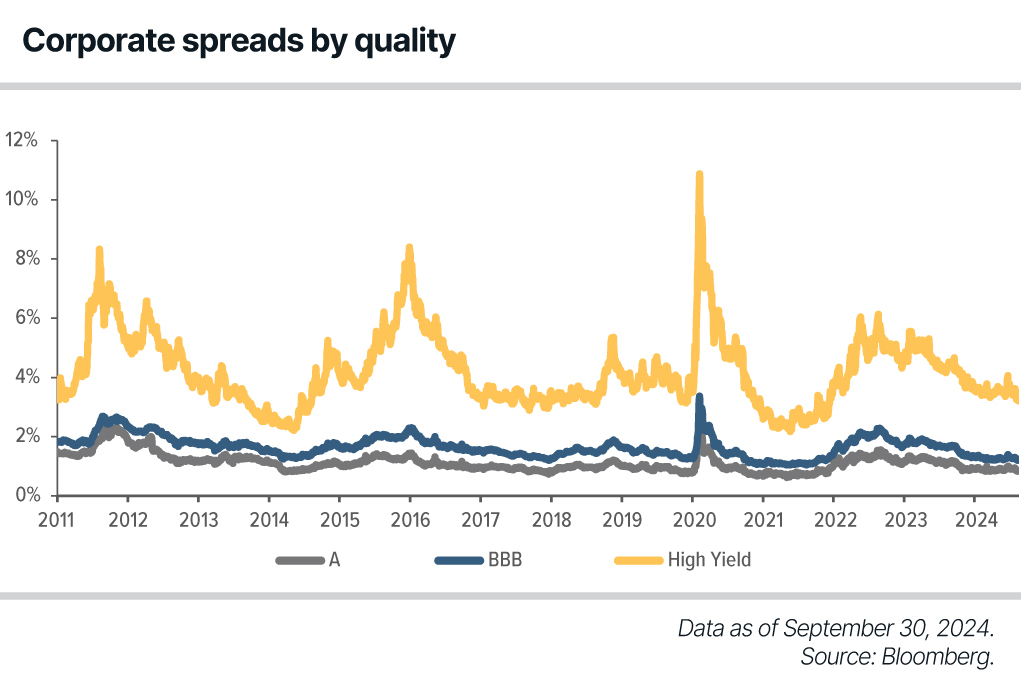

Corporate spreads reflect how the market assesses risk and credit quality by measuring the additional return demanded for investing in riskier securities. Spreads for corporate bonds across various rating classes narrowed through September, reaching a three-year low. All were below their respective 2023 averages and narrower than at the start of 2024. The below chart indicates that the bond market is gaining confidence in corporate creditworthiness and stable or improving economic conditions.

Chart showing corporate spreads by quality from 2011 to 2024. As of September 30, 2024, spreads for high-yield, BBB, and A bonds were 3.2%, 1.2%, and 0.8%, respectively.

The following chart shows the historical trend of commercial and industrial (C&I) loans outstanding to companies, as well as the net percentage of U.S. banks adjusting their credit standards for loans to large and middle-market firms according to the Federal Reserve’s Senior Loan Officer Opinion Survey (SLOOS). Note that the SLOOS data corresponds to activity in the prior quarter (that is, a report released in July represents the activity from April through June). As illustrated, during economic uncertainty or decline, banks usually tighten their lending standards and increase the cost of borrowing, leading to reduced loan demand in the following months.

Chart showing the amount of C&I loans vs. bank standards from 2005 to 2024. The latest figures are $2,767.7 million and 79%, respectively.

With a cautious economic outlook that aligned with the Fed’s view and increasing policy rates, banks’ tightening cycle began in first quarter 2022. U.S. regional banking disruption in March 2023 exacerbated this. As banks restricted access to credit and costs to borrow increased, C&I loans outstanding moderately declined throughout 2023 and into the first half of 2024, helping to cool down the economy and contributing to moderating inflation.

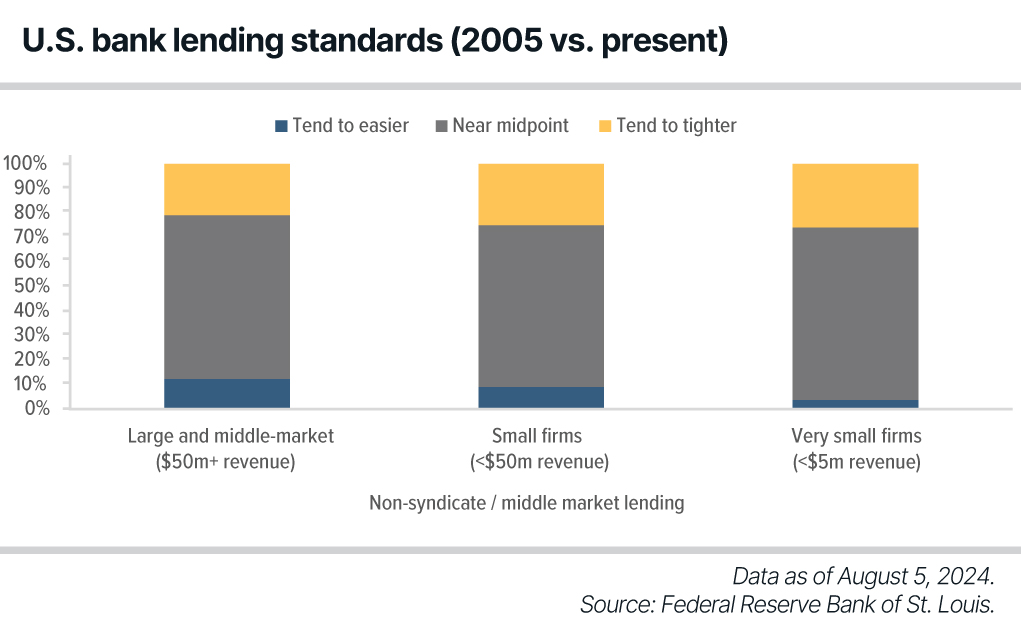

In the July 2024 SLOOS, the net share of banks reporting tighter standards for C&I loans fell to the lowest level in two years (8%). However, the current state of bank lending remained relatively stringent compared with historical norms. The following chart displays responses from the banks surveyed in July regarding their current lending standards compared with historical levels since 2005. The evaluation shows that, on average, lending standards were near the historical midpoint. Still, about a quarter of the banks reported that their standards across various categories were tighter than the historical average.

| Lender Type | Non-Syndicate / Middle Market Lending | ||

|---|---|---|---|

| Borrower Type | Large & Middle Market (revenue of $50M+) | Small Firms (<$50M of revenue) | Very Small Firms (<$5M of revenue) |

| Tend to Easier | 12% | 9% | 4% |

| Near Midpoint | 67% | 66% | 70% |

| Tend to Tighter | 21% | 25% | 26% |

While most lenders reported about the same C&I loan demand as in the previous quarter, banks reporting weaker C&I loan demand equaled banks reporting greater demand for the first time since October 2022. While banks’ caution prevails, driven by economic outlook and risk tolerance, the results indicate a steady and improving borrower optimism. In addition, with the recent decrease in the federal funds rate in September and the anticipation of further cuts before year-end, we anticipate the October 2024 SLOOS will show an increase in demand for C&I loans among U.S. banks in the upcoming months. Similarly, at BBH, we are actively expanding our corporate loan portfolio while focusing on sound credit opportunities.

The Private Equity and Mergers and Acquisitions Markets

A number of the macroeconomic and market trends from 2023 carried over through the first half of 2024. Fund managers continued to work through the shifting economic landscape by:

- Being adaptable

- Embracing technology and AI

- Focusing on value creation and optimization

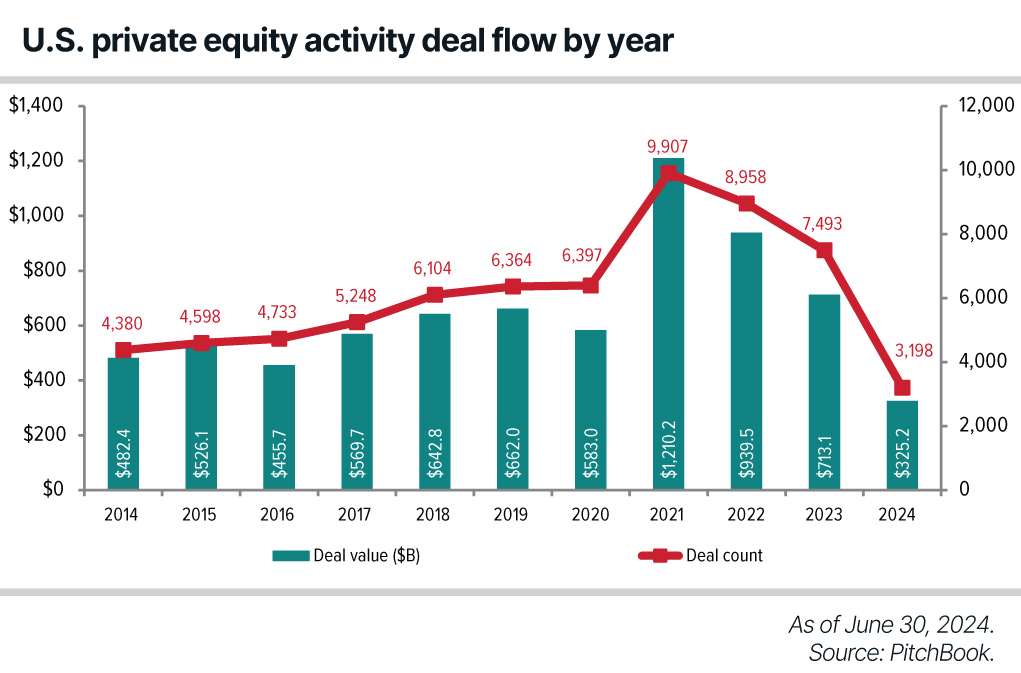

U.S. private equity (PE) dealmaking in the first half of 2024 increased approximately 12.0% year over year both in deal count and dollar amount. Second quarter 2024 PE activity saw its strongest quarter in two years with 122 deals valued at $196 billion – nearly double the $100 billion announced in the first quarter.

While dollar volumes are down 46.2% from the peak quarters of 2021, deal value and count in 2024 are significantly above the “old normal” quarterly levels of 2017 to 2019 by approximately 25% to 45%, respectively. Add-on acquisitions accounted for 75% of all buyouts in the first half of 2024, a trend that has continued in recent years.2

Generative AI is showing potential to transform and accelerate deal activity by summarizing a large amount of data so analysts can sift through opportunities more quickly. In addition, AI tools can rapidly develop outreach strategies and expand or narrow lists based on a PE manager’s investment criteria.

As deal sourcing and analysis will happen at a greater scale in the coming years, PE firms must keep up with these technological advances in order to stay competitive.3 According to Deloitte, by the end of 2023, around 10% of private investment firms had begun implementing AI in core functions such as deal sourcing and due diligence.4

The slowing pace of inflation and the potential for the end of rate hikes could clear the path for more dealmaking in the second half of the year. According to a KPMG Survey, 70% of dealmakers expect more deal activity in 2024 than the prior year.5

The slowing pace of inflation and the potential for the end of rate hikes could clear the path for more dealmaking in the second half of the year.

| U.S. Private Equity Activity Deal Flow by Year | ||

|---|---|---|

| Year | Deal Value ($B) | Deal Count |

| 2014 | $482.4 | 4,380 |

| 2015 | $526.1 | 4,598 |

| 2016 | $455.7 | 4,733 |

| 2017 | $569.7 | 5,248 |

| 2018 | $642.8 | 6,104 |

| 2019 | $662.0 | 6,364 |

| 2020 | $583.0 | 6,397 |

| 2021 | $1,210.2 | 9,907 |

| 2022 | $939.5 | 8,958 |

| 2023 | $713.1 | 7,493 |

| 2024* | $325.2 | 3,198 |

U.S. PE exit value increased by approximately 15% year over year in the first half of 2024 while exit count remained relatively flat. The lingering valuation gap between buyers and sellers is a core driver of lackluster exit activity. The exit-to-investment ratio of 0.36x in the second quarter is a new record.6 In an EY survey of general partners (GPs), just 30% cited a lack of interested buyers as the main exit impediment. Rather, GPs are focused on:

- Ensuring that their portfolio companies’ performance is optimal

- Making sure their portfolio companies present a compelling equity story

- Waiting for valuations to improve to maximize value7

The market has been clear that, in order to produce exits in this environment, GPs need to boost EBITDA efficiently and demonstrate to potential buyers that there is money “left on the table.” Fund managers need to be able to turn on value creation “levers” that can generate organic growth.8 EY’s latest “CEO Outlook Pulse Survey” reported that 74% of PE-backed companies are already using or piloting AI solutions, and this number is expected to grow.9

| U.S. Private Equity Exits by Year | ||

|---|---|---|

| Year | Exit Value ($B) | Exit Count |

| 2014 | $379.1 | 1,295 |

| 2015 | $345.0 | 1,331 |

| 2016 | $316.8 | 1,275 |

| 2017 | $359.7 | 1,338 |

| 2018 | $385.3 | 1,447 |

| 2019 | $293.3 | 1,334 |

| 2020 | $420.3 | 1,213 |

| 2021 | $828.0 | 1,893 |

| 2022 | $289.5 | 1,402 |

| 2023 | $285.8 | 1243 |

| 2024* | $141.4 | 626 |

The decline in exit activity has had a significant effect on fundraising. Slower distributions have left limited partners (LPs) cash flow negative, stifling their ability to put more capital back into PE funds. PE fundraising remained resilient in the first half of 2024 as U.S. PE funds closed 129 funds at a value of $155.0 billion, which is slightly ahead of the first half of 2023 (2023 was PE’s second-best fundraising year on record).10 However, LPs remain highly selective. While capital flowed to a subset of large and established buyout funds, fundraising for most GPs remains quite difficult.11

| U.S. Private Equity Fundraising by Year | ||

|---|---|---|

| Year | Capital Raised ($B) | Fund Count |

| 2015 | $144.7 | 405 |

| 2016 | $190.7 | 436 |

| 2017 | $255.6 | 531 |

| 2018 | $208.7 | 466 |

| 2019 | $369.1 | 559 |

| 2020 | $265.1 | 569 |

| 2021 | $362.0 | 850 |

| 2022 | $400.1 | 891 |

| 2023 | $377.1 | 497 |

| 2024* | $155.0 | 129 |

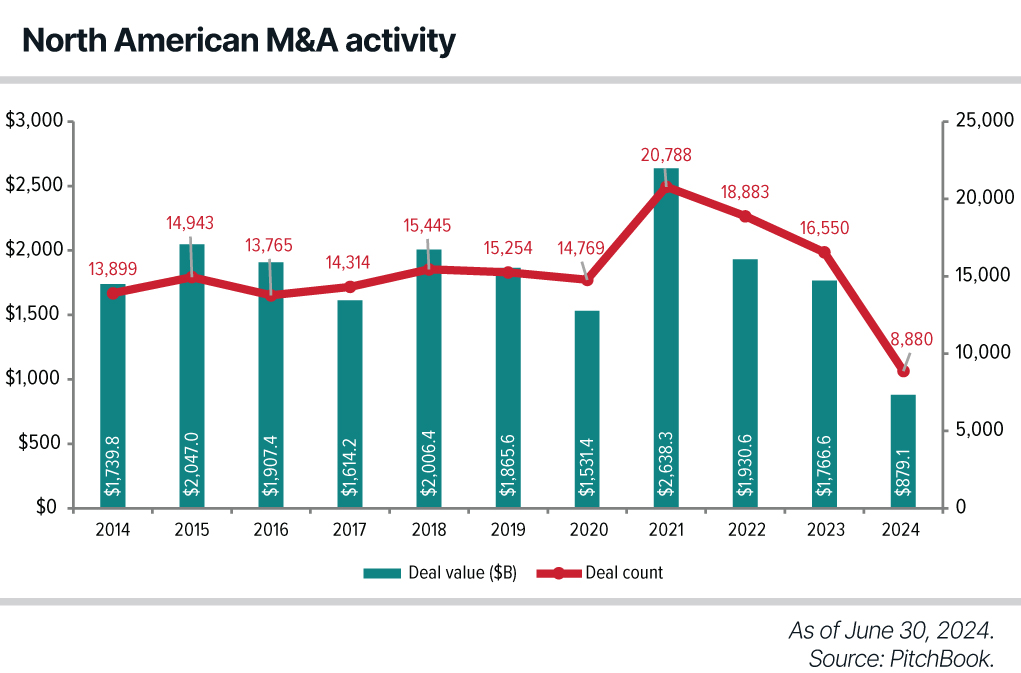

Cautious optimism is returning to the M&A market in 2024. After a tepid 2023, an M&A recovery has arrived, driven by:

- Strong corporate profits

- Rising executive confidence

- Stabilizing inflation12

In the first half of the year, North American M&A increased by approximately 13.0% year over year in terms of deal count (9,000) and deal value ($975 billion) and led all regions during this time period.13 According to a June KPMG M&A survey, the majority of executives anticipate a surge in M&A activity this year, and three-quarters plan to complete at least one deal.14

| North American M&A Activity | ||

|---|---|---|

| Year | Deal Value ($B) | Deal Count |

| 2014 | $1,739.8 | 13,899 |

| 2015 | $2,047.0 | 14,943 |

| 2016 | $1,907.4 | 13,765 |

| 2017 | $1,614.2 | 14,314 |

| 2018 | $2,006.4 | 15,445 |

| 2019 | $1,865.6 | 15,254 |

| 2020 | $1,531.4 | 14,769 |

| 2021 | $2,638.3 | 20,788 |

| 2022 | $1,930.6 | 18,883 |

| 2023 | $1,766.6 | 16,550 |

| 2024* | $879.1 | 8,880 |

Conclusion

As we near the end of 2024, we are keeping an eye on a variety of converging factors, including the Fed’s recent rate cut of 50 bps, the rise in the unemployment rate over the last several months, continued geopolitical tensions, and the upcoming U.S. presidential election – to name a few.

Meanwhile, in the credit markets, banks’ caution prevails, driven by economic outlook and risk tolerance. However, results indicate a steady and gradually improving business environment. Generative AI is also at the front of everyone’s minds – including in the PE and M&A markets, where it has the potential to transform and accelerate deal activity.

We continue to monitor this quickly developing technology and the risks and opportunities it presents. Finally, third quarter 2024 saw an increase in U.S. PE exit value, while cautious optimism returned to the M&A market after a tepid 2023.

If you have any questions about navigating today’s business environment, reach out to a BBH relationship manager.

1 One basis point or bp is 1/100th of a percent (0.01% or 0.0001) and is used to denote the change in price or yield of a financial instrument.

2 Pitchbook.

3 AlphaSense: Private Equity Trends and Outlook for 2024.

4 Deloitte Center for Financial Services.

5 KPMG August 2024 M&A deal market study.

6 Pitchbook.

7 EY Private Equity Pulse: key takeaways from 2Q4.

8 Private Equity Outlook 2024: The Liquidity Imperative.

9 EY.

10 Pitchbook.

11 Bain: Private Equity Outlook 2024: The Liquidity Imperative

12 PWC US Deals 2024 midyear outlook.

13 Pitchbook.

14 KPMG 2024 M&A outlook for corporate deal makers.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07802-2024-10-08