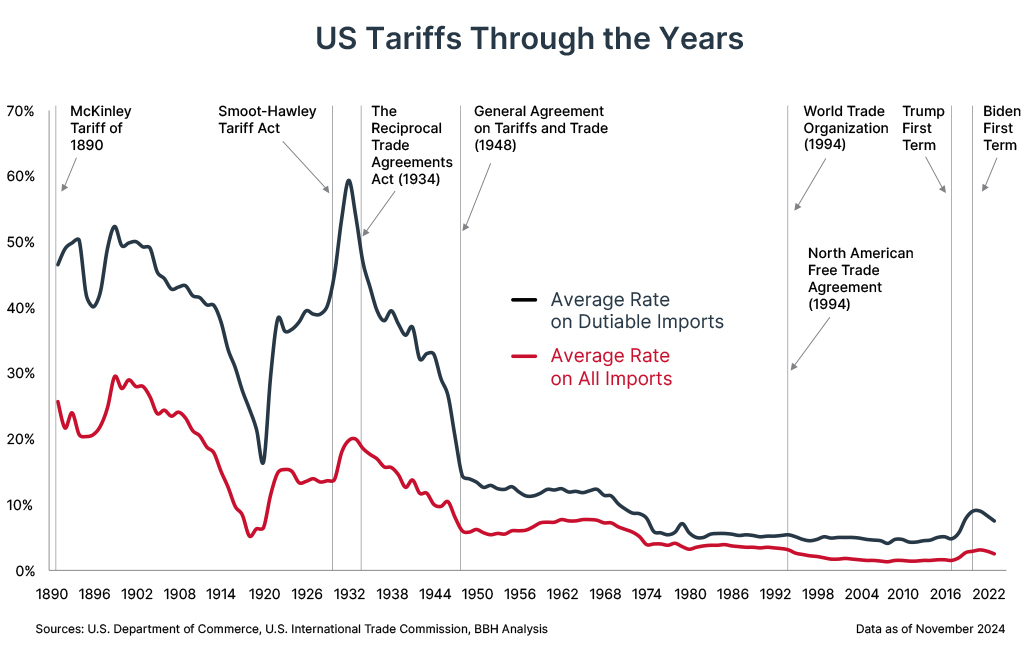

Chart tracking the average rates on all imports vs. on dutiable imports from 1900 through 2024. The latest figures are 2.4% and 7.4%, respectively.

With President Donald Trump’s return to the White House, tariffs have once again taken center stage – but this time, the conversation feels different. Tariffs are increasingly becoming a central focus of economic and political discourse, but they are by no means a new tool: Every U.S. president since this nation’s founding has used them. However, tariffs are emerging as a cornerstone of Trump’s “America First Trade Policy,” and while uncertainty remains on how these policies will be rolled out, it is clear that Trump’s approach to tariffs is more far-reaching than his contemporary predecessors.

The U.S. Constitution grants Congress the power to regulate commerce with foreign nations and to levy duties on imports. Historically, Congress has been the primary body that sets tariff rates; however, there are several modern laws that grant the president additional authority over trade policy. For instance, Trump has recently cited the International Emergency Economic Powers Act (IEEPA), which grants the president broad authority to address “unusual and extraordinary threats” with swift executive action during a national emergency.

Let’s start with the basics – what are tariffs?

Put simply, tariffs are taxes imposed on imported goods. Historically, they’ve served several functions, including raising revenue for the federal government, protecting domestic industries from foreign competition via import restrictions, and, at times, influencing the balance of trade. Tariffs are a form of protectionism, whereby in raising the cost of imported products, the government seeks to make domestic goods more attractive to U.S. businesses and consumers.

Tariff types at a glance

| Type | Ad valorem | Antidumping and countervailing duties | Retaliatory tariffs |

|---|---|---|---|

| Definition | A tariff calculated as a percentage of the value of the imported good | Tariffs imposed on imports sold below fair value to prevent unfair trade practices like dumping (selling goods below market value) or government subsidiaries | A tariff implemented in response to another country’s tariffs or trade policies |

| General purpose | Generate revenue and regulate trade by increasing the cost of the imported good | Protect domestic industries from unfair foreign competition | Punish or pressure a trading partner to change its trade policies |

| Example | The U.S. announced a 25% ad valorem tariff on all imports of steel and aluminum, which took effect on March 12, 2025. | In August 2024, the U.S. increased tariffs on Canadian softwood lumber imports from 8.05% to 14.54%, citing unfair subsidies to Canadian producers. | In March 2018, after the U.S. imposed a 25% tariff on steel and a 10% tariff on aluminum, China retaliated with a series of tariffs. The U.S. further responded with additional retaliatory tariffs on Chinese goods. |

Who pays for tariffs?

The importer of record (the company purchasing goods from abroad) is responsible for paying tariffs. Tariffs incentivize importers and consumers to behave differently, such as by purchasing goods domestically or by finding other products that can be used as a substitute. In practice, importers might choose to reduce their profit margins to keep their products attractive to consumers, or exporters might lower costs to retain market share. However, it is often the consumer who bears the burden of higher prices. This is especially true when tariffs are placed on goods the U.S. does not produce domestically, such as coffee (for example, Hawaii produces limited coffee), or for which there are few substitutes, such as potash (an essential fertilizer exported from Canada).

Tariffs can also play a role in protecting emerging industries like electric vehicles by incentivizing companies to produce more domestically. According to analysis from the Peterson Institute for International Economics, low-income households are the most vulnerable to tariff-induced price increases and experience disproportionately higher costs of everyday goods as a result.

How has U.S. tariff trade policy evolved?

The Tariff Act of 1789: One of the first acts of Congress, this act established tariffs as a key source of revenue for the new federal government. Tariffs served as the most significant source of revenue for the federal government until the federal income tax was ratified in 1913.1

McKinley Tariff of 1890: This legislation raised average duties on imports to nearly 50%, continuing and strengthening protectionist policy in support of U.S. manufactures during a period of rapid industrialization. However, critics argued that this policy led to higher consumer prices.

Smoot-Hawley Tariff Act (1930): In an effort to protect domestic industries during the onset of the Great Depression, this act sharply increased tariffs on thousands of imported goods. While supporters argued it shielded domestic jobs, critics contended that it contributed to a decline in international trade as other countries imposed retaliatory tariffs. Economists and historians debate the extent of its impact, but it's often cited as a factor that exacerbated global economic challenges during the 1930s.

The Reciprocal Trade Agreements Act (1934): In response to the effects of the Smoot-Hawley Tariff Act, this act empowered the executive branch to negotiate tariff reductions on a reciprocal basis with other nations, marking a significant move toward trade liberalization.

General Agreement on Tariffs and Trade (GATT, 1948): GATT established a framework to gradually reduce tariffs and other trade barriers.

World Trade Organization (WTO, 1994): The WTO replaced GATT and expanded beyond tariffs, providing a more structured and enforceable system for trade rules in an effort to prevent unfair trade practices.

The North American Free Trade Agreement (NAFTA, 1994): NAFTA eliminated most tariffs and trade barriers between the U.S., Canada, and Mexico.

Modern tariff policy: What is the new normal?

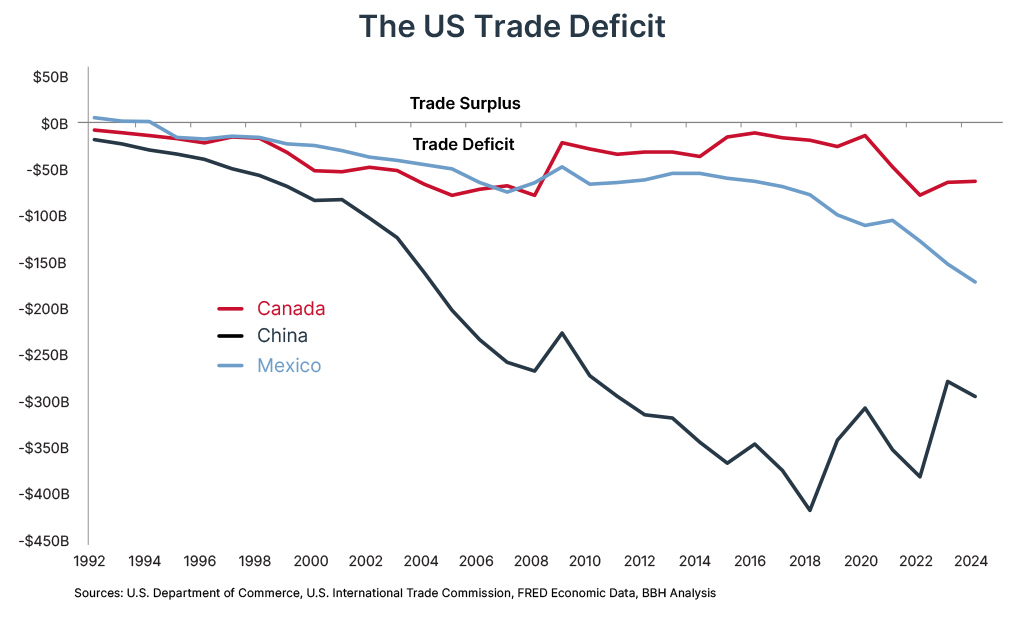

The U.S. has the largest trade deficit in the world, amounting to $918.4 billion in 2024.2 This means that the U.S. imports far more goods than it exports, relying on other countries for essential products like electrical equipment, cars, and heavy crude oil. Standard economic theory predicts that large deficits should be self-correcting over time: A large U.S. trade deficit should lead to the dollar being less valuable compared to other currencies. Americans pay foreign suppliers in dollars, and those suppliers must sell dollars and buy their own currency back, which pushes up the supply of dollars and increases demand for other currencies.

The theory holds that a weaker dollar makes imports more expensive and incentivizes Americans to buy more goods domestically, which reduces the deficit. However, as supporters of tariffs point out, this hasn’t happened over the past 20 years, in part because of the dollar’s status as the global reserve currency.3

Let’s take a look at how U.S. trade has evolved. In 2024, the U.S. imports of goods and services were 14.0%4 of the country's nominal gross domestic product.

Chart tracking the U.S. trade deficit with its top three trading partners (Canada, Mexico, and China) from 1922 to 2024. The latest figures are $63 billion, $172 billion, and $295 billion, respectively.

For example, in March during the period where trade liberalization was favored in U.S. policy, the country’s trade deficit with its top three trading partners – Canada, China, and Mexico – grew significantly. President Trump’s first term set out to respond to growing concerns of trade imbalances, laying the groundwork for a new era of trade policy. For example, in March 2018, President Trump applied a 25% tariff on steel and a 10% tariff on aluminum imports, asserting that the reliance of the U.S. on foreign metals constituted a national emergency, which he argued weakened U.S. manufacturing capabilities critical to defense. By mid-2019, these tariffs were lifted on Canada and Mexico and led to the United States-Mexico-Canada Agreement (USMCA, 2020), which replaced NAFTA but retained many of the core trade liberalization principles.

Trump’s new administration has taken a different approach, not only withholding exemptions for key trade partners, but actively targeting them along with other countries where the U.S. faces a trade deficit. During his first term, Trump created a system allowing companies to request exceptions from tariffs, particularly for critical manufacturing materials inputs that cannot be sourced domestically. In his new term, however, he has opted to eliminate these carve-outs almost entirely (although the tariff policies are ever-evolving).

President Trump continues to use tariffs in new ways, including as a direct form of diplomatic pressure, breaking previously established economic and political norms. For instance, in January 2025, he threatened to impose a 25% tariff on all Colombian imports in response to Colombia’s refusal to accept deportation flights carrying Colombian nationals. Once the Colombian president revised his position, the tariff was put on hold indefinitely.

Uncertainty remains…

While there was a modest increase in domestic employment with steel and aluminum manufacturing jobs following President Trump’s initial tariff policy in his first term, many other manufacturing jobs that rely on these key inputs faced higher production costs and suffered related job loss. It is worth noting that the last two quarters of 2019 and first quarter of 20205 were marked by consecutive declines in real gross domestic product investment (GDPI), a leading indicator for companies’ willingness to invest in the U.S. When companies face uncertainty around trade policy, they often delay or scale back capital investment to avoid potential risks, which puts pressure on the manufacturing industry. Real GDPI declined for the second consecutive quarter at the end of 2024, highlighting how uncertainty around trade policy continues to shape investment decisions and leaving the manufacturing sector facing some of the same challenges it did five years ago but on a new scale.6

The evolution of U.S. trade policy highlights the complex and often unpredictable impact of tariffs on the economy. While tariffs are designed to protect domestic industries, their broader effects – rising costs, shifting trade relationships, and investment slowdowns – can create unintended consequences. The growing trade deficit with Canada, China, and Mexico, despite their status as key trading partners, underscores the challenges of using tariffs as a long-term economic strategy. With manufacturing investment declining and uncertainty shaping business decisions, all eyes are on the coming quarters to watch which industries are most affected and to see if real GDPI continues to fall, signaling deeper economic concerns.

We will continue to monitor the state of U.S. trade policy. In the meantime, if you have further questions or wish to discuss tariffs and their implications in more detail, reach out to your BBH relationship team or a member of the Corporate Advisory & Banking group.

Contact Us

1 https://www.archives.gov/milestone-documents/16th-amendment

2 https://www.bea.gov/news/2025/us-international-trade-goods-and-services-december-and-annual-2024

3 As a reserve currency, foreign companies can transact with other foreign companies using dollars, or to buy U.S. treasury debt with dollars.vThis keeps the supply/demand for dollars steady and interrupts the feedback loop predicted by standard economic theory.

4 https://fred.stlouisfed.org/series/B021RE1A156NBEA

5 https://fred.stlouisfed.org/series/GPDIC1

6 https://www.bea.gov/news/2025/gross-domestic-product-4th-quarter-and-year-2024-advance-estimate

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-08411-2025-03-28