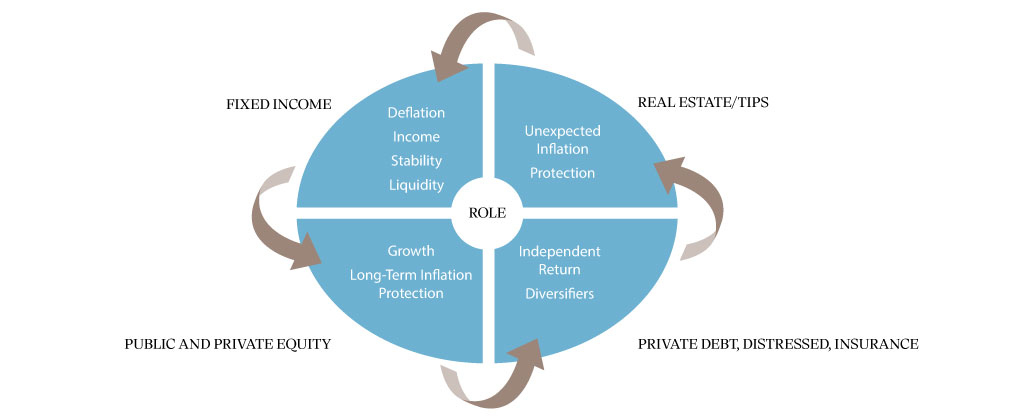

This graphic shows the different roles various asset classes (public and private equity; fixed income; real estate/TIPS; and private debt, distressed, insurance) play in a portfolio.

Endowment and foundation (E&F) trustees and management teams understand that one of their most important responsibilities is to prudently invest the institution’s assets.

Setting an appropriate asset allocation is critical to achieve that goal. Asset allocation should be carefully documented in an investment policy statement (IPS) and reviewed regularly.

Here, we explore the special considerations that are key to successful asset allocation for E&Fs, including:

- Risk/return considerations

- Spending policies

- Liquidity needs

We also discuss private investments – why and when to include them in a portfolio and how much of an allocation is appropriate.

Setting an asset allocation

David Swensen at Yale University popularized the “endowment model,” and many E&Fs have since adopted it. This asset allocation model seeks to maximize returns by focusing on partnerships with exceptional managers who can take advantage of inefficient markets and capitalize on the long-term nature of most nonprofit institutions.

This approach results in asset allocation outputs that favor alternatives, including private equity, venture capital, and real assets, as well as public equity and hedge funds, while allocating very little to fixed income and cash.

While it is tempting to replicate a model that has worked so well for Yale and other large endowments, rather than simply following this investment strategy, one should consider an institution’s unique factors, needs, and preferences when setting an asset allocation.

The primary objective of an E&F investment portfolio is to maintain its purchasing power so that support for the operating budget keeps pace with inflation over time.1 Such an objective facilitates “intergenerational equity,” ensuring that the same level of spending is available to future generations.

Trustees and management are responsible for setting an asset allocation that provides the best chance of achieving both goals of supporting the operating budget today and maintaining purchasing power into the future.

It would be easy if there was one asset allocation that worked for all E&Fs. Unfortunately, there is no “one-size-fits-all” solution, as setting an asset allocation requires an understanding of each institution’s unique attributes.

Some factors will be weighed more heavily by one institution over another. Spending policies and needs, liquidity position, and the overall financial health of an institution are all important factors in determining what level of price volatility would be tolerable and what level of investment returns are required to maintain the purchasing power of the institution in perpetuity.

Risk/return trade-off

An appropriate asset allocation involves balancing return objectives with risk tolerance. At the most basic level, when setting an asset allocation, a client’s return objective is met with growth- or equity-oriented investments, while risk is largely controlled by investing in high-quality fixed income and cash investments.

In a vacuum, it would make sense for an E&F to invest the majority of its investment portfolio in growth assets – both public and private equity – in order to maximize the value of its endowment in the long term. But such a decision would likely result in substantial short-term volatility, which could reduce spending from the endowment during a period in which equities decline, or risk a permanent impairment of capital from selling risk assets at the bottom of the market.

If an E&F prioritized generating income to meet its spending needs, it might invest mostly in fixed income. That decision, while significantly reducing volatility, would likely result in the portfolio’s spending power declining over time by not keeping pace with the spending rate plus inflation.

Finding the right balance between equity and fixed income is a first priority, but setting an asset allocation for an E&F is more nuanced than this simple example. As shown in the nearby graphic, asset classes play different roles in a portfolio, and the long-term target allocation for each asset type is established based on the role it can play.

Combining asset classes that have different return drivers and therefore perform differently in various market environments (that is, diversifying the portfolio) is a prudent risk management strategy that is key to meeting long-term investment objectives while dampening volatility. For example:

- Independent return strategies such as private debt or distressed investments can provide excellent returns that are not dependent on equity or fixed income market performance.

- Adding real estate or Treasury inflation-protected securities (TIPS) can protect the portfolio in periods of unexpected inflation.

- To benefit from an illiquidity premium and further enhance returns, a private equity allocation can be additive. (A deeper discussion of private equity is set forth later in this piece.)

Diversifying a portfolio’s equity and fixed income allocations across positions, regions, and sectors is also important. For example, if several managers have significant overlapping positions, the portfolio may not be as diversified as one might otherwise assume. Doing a proper look-through analysis and understanding these concentrations is critical to manage risk.

One of our highest-conviction managers illustrates diversification well. He asks two questions that must be answered together: 1) Do you believe in diversification? and 2) Are you disappointed if one part of your portfolio has losses when others are positive? If the answer to the first question is yes and the second is no, you do not believe in diversification. It is important to discuss with an investment committee what diversification truly means so that expectations are properly managed. |

Risk tolerance

Many institutions think they can stomach short-term volatility. In reality, when a market downturn occurs, management and trustees often decide they can no longer hold onto declining investments, and they sell at exactly the wrong time.

Running stress tests and scenario analyses to understand what those return patterns could look like – and what those declines translate to in dollar terms – helps educate stakeholders and ensures that no one is surprised in a downturn.

Setting appropriate return and risk expectations can help the institution to not only hold on to investments during a market correction, but also add when valuations are particularly compelling. Opportunistic rebalancing – and in particular, rebalancing without tax implications – is one of the greatest levers that nonprofit institutions can utilize to enhance returns.

It is never easy to stay invested when markets are declining. We have seen even very sophisticated investors sell out of equities during periods of market panic, such as the global financial crisis and COVID-19. However, as shown in the nearby chart, it is nearly impossible to time the market successfully. You might make the right call to exit the market, but you will inevitably miss the market recovery.

The following chart presents the return of the S&P 500 over the past 34 years compared with the return if you simply missed the 10 best trading days. The return difference is staggering. Unfortunately, no one can consistently predict when downturns will occur, or when the market will rebound, so the best approach is to remain invested according to your long-term asset allocation and rebalance.

| Nominal Value of $1 | |

| Stayed invested | $30 |

| Missed the single best day in the market | $27 |

| Missed the three best days in the market | $22 |

| Missed the five best days in the market | $19 |

| Missed the 10 best days in the market | $14 |

Finally, while we highlighted volatility as an important risk, one must be mindful of other risks in the portfolio. Factors such as appropriate leverage levels, derivatives use, duration in fixed income, position and sector concentration, and fees should be agreed upon and documented.

Spending policies

Another important consideration in setting an asset allocation is determining an institution’s spending needs and its reliance on its endowment to meet those needs. These spending requirements translate into the institution’s spending rate (dollars spent out of the endowment divided by the endowment’s net asset value).

A higher spending rate generally necessitates a higher required rate of return to maintain purchasing power over time. However, a higher spending rate can also result in an institution that is unable to tolerate endowment volatility.

All institutions should set an appropriate spending policy (that is, a plan that governs how much of the organization’s long-term assets can be used each year). Choosing the right policy for your institution is critical to maintaining the balance between current and future spending needs.

For a deeper discussion on the various spending policies and the considerations around choosing from three general approaches – steady growth, target percentage, or a hybrid of the two – please reach out to your Brown Brothers Harriman (BBH) relationship manager.

The percentage of the institution’s budget that is supported through endowment spend should also be considered. In general, if the amount of endowment support is relatively low (that is, 15% to 20%), and there are many other sources of income that can be relied upon for spending (for example, operating revenues, gifts, etc.), then the portfolio might be able to tolerate more risk and short-term volatility to achieve a higher return.

In contrast, if the endowment is the sole source of support for the budget, it may be more appropriate to achieve a balance of growth assets and diversifiers/fixed income, as a significant decline in the endowment could make it difficult for the institution to fund its current expenses.

Planning for the steps an E&F can take in the inevitable situation when the market – and therefore, spending from the endowment – declines is a prudent exercise. Key questions include:

- Can the institution cut expenses if necessary?

- Are there other sources of income that can be tapped in a downturn (for example, gifts or lines of credit)?

- Is there debt that must be serviced?

- Is there a rating on the debt that must be maintained?

In all cases, it is important to consider the financial health of the institution as a whole to establish an asset allocation that allows for staying power during a downturn so that the long-term return objectives can be met.

Liquid vs. illiquid

Different asset classes provide varying amounts of liquidity, from cash that is completely liquid to private equity investments, which typically have fund lives of more than 10 years.

Even public equities, which can usually be sold quickly, should not be counted on for liquidity needs, as one of the worst outcomes is the permanent impairment of capital that comes from selling equities in a market downturn to fund current cash needs.

When establishing an asset allocation, it is imperative to forecast cash flow needs so that the portfolio will have enough liquidity to meet its obligations for operating expenses, nonoperating expenses (such as interest payments on debt, capital expenditures, and so forth), and capital calls for private investments.

We believe that carefully selected private investments can boost portfolio returns, as investors are provided with an illiquidity premium to lock up their money. However, all private investments are not created equally and should only be made if the following criteria are met:

- The investor is getting an adequate illiquidity premium.

- There is an internal team or external advisor that can identify top-tier private investment managers.

- The organization can properly handle the capital call and distribution activities from an operational perspective.

Private investments: Why, how, and how much?

As discussed, if an institution can take on illiquidity within its investment program, private funds have historically added value over public markets, earning a consistent illiquidity premium over time.

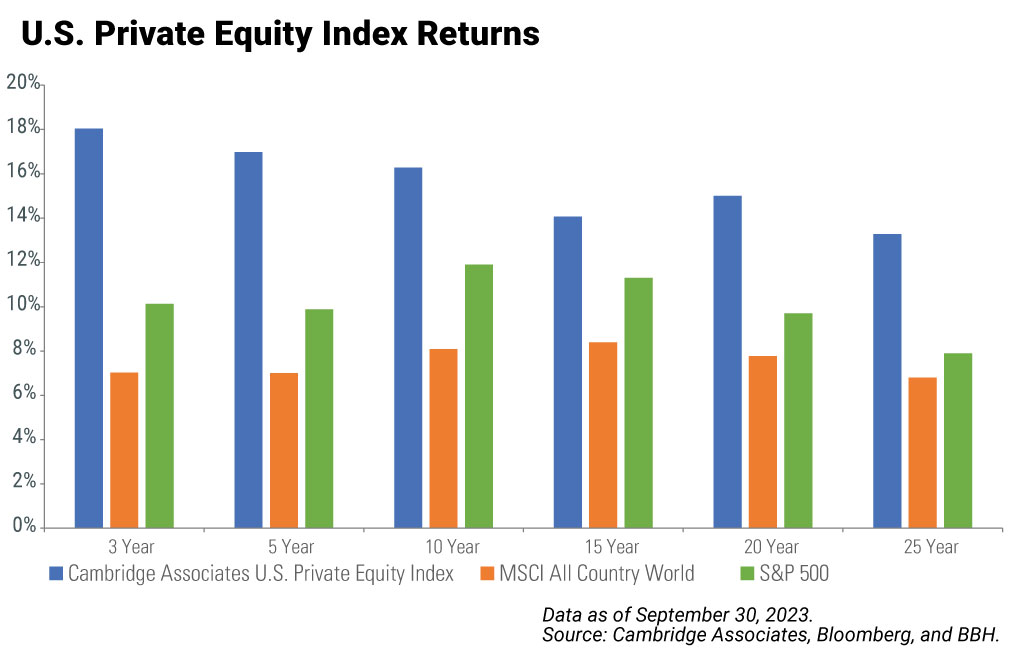

A 2015 Cambridge Associates study, “The 15 Percent Frontier,” analyzed data amassed since the 1970s to conclude that E&Fs with higher allocations to private investments achieved stronger long-term returns with remarkable consistency year after year.

The following chart compares Cambridge Associates U.S. private equity pooled returns with public market benchmarks (S&P 500 and MSCI ACWI) over multiple time periods. Private market returns have consistently outperformed by a significant margin.

| 3 Year | 5 Year | 10 Year | 15 Year | 20 Year | 25 Year | |

| Cambridge Associates U.S. Private Equity Index | 18.0% | 17.0% | 16.3% | 14.1% | 15.0% | 13.3% |

| MSCI All Country World | 7.0% | 7.0% | 8.1% | 8.4% | 7.8% | 6.8% |

| S&P 500 | 10% | 10% | 12% | 11% | 10% | 8% |

We have seen the outperformance of private investments in our own portfolios at BBH, where real estate, distressed debt, private debt, and private equity funds have all outperformed their relevant public market benchmarks.

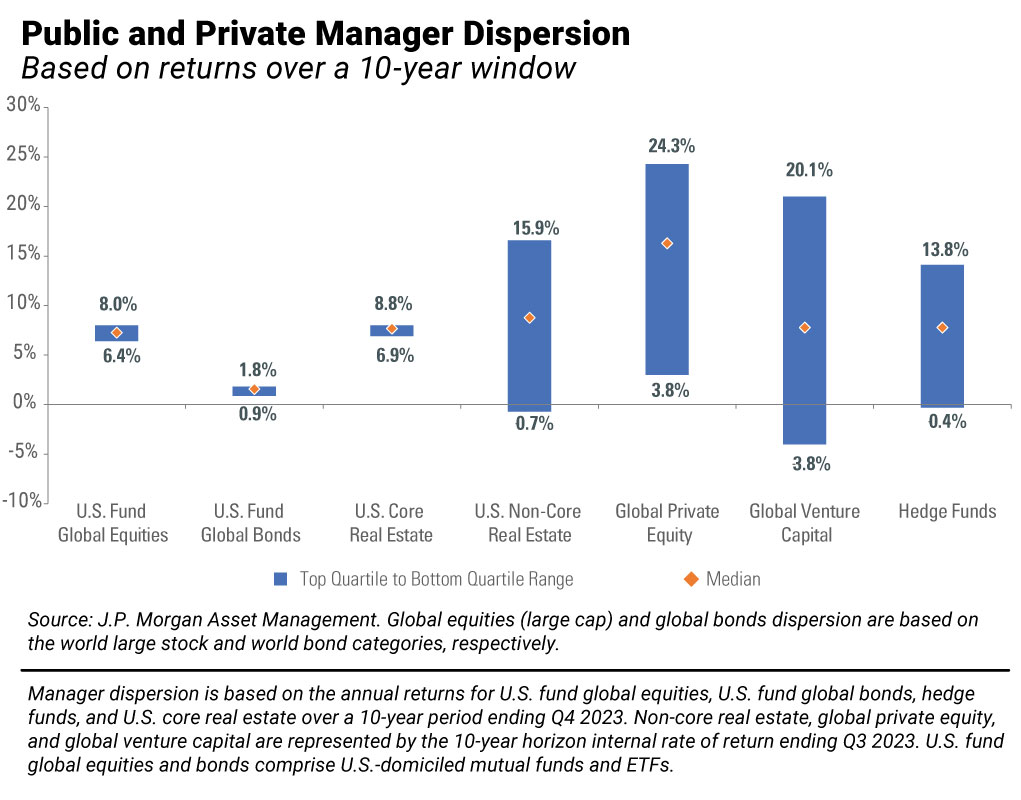

Manager selection can be particularly additive in private markets, as there tends to be greater dispersion of returns vs. traditional markets and more persistency bias, with the strongest managers consistently outperforming.

For example, as seen in the nearby chart, for the 10-year period ended September 30, 2023, there was over a 20% spread between top- and bottom-quartile private equity funds (24.3% vs. 3.8% net IRR) vs. a spread of less than 1% between top- and bottom-quartile U.S. global equity funds.

| 3 Years | 5 Years | 7 Years | ||

| Private Debt | 11% | 7% | 6% | |

| Morningstar LSTA Leveraged Loan Index | 6% | 5% | 5% | |

| 3 Years | 5 Years | 7 Years | 10 Years | |

| Private Equity | 10.8% | 11.4% | 12.8% | 12.2% |

| MSCI ACWI Index | 6.9% | 6.5% | 8.6% | 7.6% |

| 3 Years | 5 Years | 7 Years | ||

| Distressed | 17% | 10% | 9% | |

| HFRI ED Distressed/Restructuring Index | 8% | 4% | 6% | |

| 3 Years | 5 Years | 7 Years | ||

| Private Real Estate | 5% | 6% | 8% | |

| FTSE NAREIT Equity REITs Index | 3% | 3% | 3% |

How much of the portfolio should be allocated to private investments? To answer this question, several others must be answered in turn.

- First, how much incremental return does the institution need to meet its return objective? Since private equity is added to provide a return premium to public equity, a greater allocation may be justified to support a higher spending rate.

- Second, how much cash flow is needed for spending, and is there enough liquidity in other parts of the portfolio? If the portfolio is invested in many hedge funds with lockups, small-cap equities that do not trade as easily, or other assets that have lower liquidity, private equity might be appropriate at a lower level (for example, 5% to 15%), or not at all. If there is an adequate level of cash and fixed income and few other calls on the endowment, the institution might be able to have a higher allocation (for example, 25% to 30%).

- Finally, what is the mix of private investments, and what are the expected distribution and income characteristics? There are different private investment asset classes, including real estate, private credit, and private equity. A private investment portfolio composed of predominantly private credit has a different liquidity profile than one entirely composed of venture capital, for example.

Larger institutions generally have a greater allocation to private investments compared with smaller institutions. A Mercer study from 2023 found that allocations to nontraditional asset classes (asset classes excluding developed market equities and bonds) were strongly correlated with the size of investment portfolios. For example, 63% of the institutions surveyed with portfolios over $1 billion had an allocation to private equity funds relative to 33% of portfolios under $100 million and just 12% of those under $50 million.

A recent NACUBO survey found that endowments with more than $1 billion in assets allocated nearly 30% of capital to private capital (private equity and venture capital collectively), whereas those institutions surveyed with $500 million to $1 billion in assets had an average allocation of 18%. Institutions below $100 million generally had less than a 5% allocation.

This same study found that, consistent with recent years’ surveys, the largest endowments outperformed, which was largely driven by their substantial exposure to private equity and venture capital.

The pattern of larger institutions maintaining greater private capital exposure likely exists because larger organizations have the resources and skill sets to identify, monitor, and record the activities that are required for these types of investments.

Lastly, in building an allocation to private investments, it is important to note that it takes time, as vintage year diversification is an important first principle of prudently investing in privates. BBH recommends using an annual private investments “budget” to consistently allocate across vintage years, with the goal of reaching and maintaining the long-term target asset allocation.

Creating an IPS

The final stage of the asset allocation process is to codify all of these carefully made decisions in an IPS. An IPS should include:

- The portfolio’s long-term return objectives

- The policy asset allocation targets and ranges around these targets

- Policy benchmarks

- Risk levels

- Time horizon

- Liquidity provisions

- Spending needs

- The parties responsible for ensuring adherence to these policies

Inevitably, the institution’s needs and market environment will change. Therefore, the asset allocation should be reviewed at least annually, along with the other components of the IPS, and any changes should be documented and approved. If you have any questions about setting up your institution’s IPS, please reach out to your BBH relationship manager.

Contact Us

1 The exception to this rule is when an E&F will not last in perpetuity but has a finite life.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2026. All rights reserved. PB-09606-2026-05-20