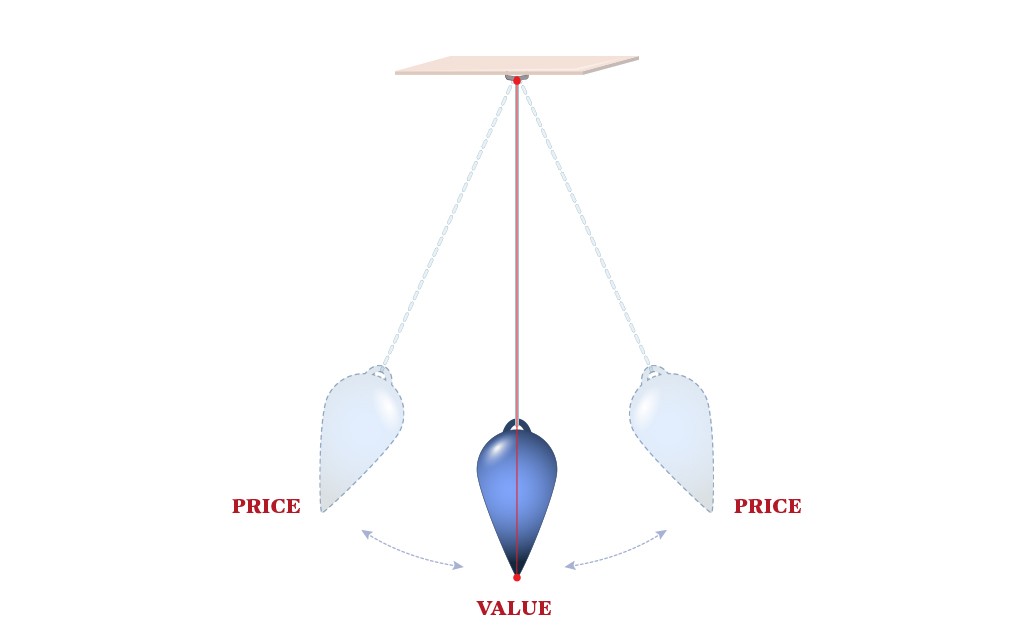

Pendulum depicting the relationship between price and value, where price is the point of the pendulum and value is the equilibrium position.

We at Brown Brothers Harriman (BBH) are fortunate to work with private business owners throughout our practice, whether we’re lending money, investing private equity, counseling clients on business strategy, advising on estate planning or trust issues, or managing the liquid wealth that business ownership creates.

Private business is not only the history of our firm, it is the history of the American economy: Even today, less than 1% of all companies in the United States are publicly traded. We’re proud to be part of the 99% of American businesses that are privately owned.

Many of our clients rely on us to invest their financial wealth while they focus on running their businesses. We are reminded repeatedly that managing an operating business and managing a financial portfolio are, at their core, the same exercise. Both involve the careful allocation of capital, which, in turn, requires prudent risk analysis, a careful assessment of value, and a prioritization of competing opportunities.

As investors of financial capital, we have much to learn from our friends and clients who are investing operating capital. Here, we consider the insights that successful private businesses have to offer to the art and science of investing and portfolio management.

Invest for intrinsic return

The difference between extrinsic (market-driven) and intrinsic (value-driven) returns can seem nuanced, but savvy investors know and appreciate the distinction. The best investments are those that have an internal engine of value creation. Rather than relying on another buyer to pay a higher price for an asset, the patient and disciplined investor or business manager instead focuses on nurturing the fundamental value of the business to generate long-term growth and cash flow along the way.

Rather than give into the temptation of daily pricing, the patient and disciplined portfolio manager spends time, energy and resources understanding the fundamental value of the business, and the growth intrinsic to the business itself."

A financial investor who depends on the market for her return has no choice but to pay attention to price on a regular basis. Make no mistake – markets are good things. Public markets allow investors to price their portfolios daily, but it is dangerous to place too much meaning on daily market moves, or to make decisions based only on prices.

Private business owners, meanwhile, don’t have the distraction of outside shareholders placing a daily price on their business, which allows them to focus solely on enhancing the quality and value of their business. This is the same case with portfolio managers. Rather than give into the temptation of daily pricing, the patient and disciplined portfolio manager spends time, energy and resources understanding the fundamental value of the business, and the growth intrinsic to the business itself.

Furthermore, the private business owner has control, or at least influence, over the value of the business through the management decisions she makes. This doesn’t translate directly into the world of public markets: A passive shareholder of a traded stock rarely has a seat at the management table unless she is an activist shareholder. In the portfolio world, the equivalent of control or influence is the assessment of value, and the discipline to buy or sell an asset based on the deviation of price from value.

This is easier said than done. In pursuit of intrinsic business growth, we prefer to invest in securities that afford us a greater than average degree of control over value, usually by providing an essential product or service, earning the loyalty of repeat customers, and enjoying the protection of a strong balance sheet and healthy free cash flow. Businesses with these characteristics are better able to withstand the perils of market and economic volatility. Why make it more difficult?

To quote Warren Buffet, the dean of intrinsic value investing, “I don’t look to jump over seven-foot bars: I look around for one-foot bars I can step over.”

Price ≠ value

This isn’t to say that price plays no role in decision making in public markets, just that it should play the right role. The concept of price has a handful of appealing attributes. Prices are transparent, frequently updated, broadly disseminated, and generally agreed upon. Unfortunately, all these benefits come with one big downside: prices are volatile. Over the last decade, the annual price volatility of the S&P 500 large capitalization index has been 26%, and the prices of individual securities can vary much more widely.

The concept of value has the opposite characteristics. Value is not transparent, analysts often disagree dramatically on the true value of an asset. It takes work and time to develop a robust estimate of the value of an asset.

Yet unlike price, value is a pretty durable concept. Compared to public equity volatility of 26% over the past decade, the volatility of nominal Gross Domestic Product (GDP) over this same period was only 3%, even accounting for the COVID-19 pandemic. The growth in the value of American businesses over time reflects broad economic growth rather than the price of the S&P 500 index.

This distinction between price and value leads to the observation that there are only two investment strategies in all the world – either a price anticipation or value recognition approach:

1. The price anticipation approach is far more common. Turn on any financial news show, and someone is recommending that you buy a certain stock before an earnings announcement or a product launch, or sell bonds before the Fed shifts monetary policy, etc. Algorithmic or high-frequency trading approaches fall into this category as well, with quantitative analysis driving the trading decisions rather than fundamental analysis.

There are three challenges with this approach:

1. You have to know what the future holds

2. You have to know the timing of future developments

3. You have to know what these developments mean for asset prices

If we have learned nothing else over the past four years, we’ve learned that the future is forever an unknowable place. Any investment strategy that relies on consistently getting all three of these things right is doomed to fail.

2. The value recognition approach, meanwhile, requires a keen analysis of the intrinsic value of an asset, but does not rely on a particular economic outcome, market condition, timing, or specific buyer to generate a return. We prefer this approach, as it transforms the volatility of price from the investor’s worst enemy into her good friend.

It is precisely the difference between price and value that an investor seeks to exploit. So, too, in the world of business. A patient and disciplined business can benefit from anxiety or panic in the private marketplace by exploiting the difference between the price and value of private assets.

In a perfectly efficient world, price and value would be the same. We believe that markets are relatively efficient and that prices trend towards underlying value over time, but the volatile range of human emotions often pushes prices far away from any reasonable estimate of value. Think of a pendulum, where the point of the pendulum is price, and the equilibrium position is value.

At rest, value and price are the same thing, but markets are never at rest. Patient capital allocation requires a focus on the equilibrium position (value) rather than the volatility of the pendulum (price).

The critical importance of writing things down

Nothing went right on June 6, 1944. The weather, wind and tides confounded the Allies landing at Normandy, and very few troops wound up where they were supposed to be. Improvisation became a soldier’s most valuable weapon.

After the war, Supreme Allied Commander Dwight Eisenhower was asked about the failure of pre-invasion preparation. “Yes,” he agreed, “all of our plans turned out to be worthless. Planning, on the other hand, won the war.”

A robust and repeated planning exercise and culture allows a business to adapt as unexpected opportunities arise and unforeseen challenges develop."

In other words, the planning exercise itself created the adaptability that allowed the troops to respond in the moment to unexpected developments. The output of the exercise – the plans themselves – was far less useful.

Every good operator has a business plan. It may be PowerPoint slides, a Word document, a board presentation, or even just the back of a napkin (not recommended beyond the venture capital stage, although it makes for a good founding story). Yet as with D-Day, plans often begin to unravel as soon as they are put into action.

So why plan at all? A robust and repeated planning exercise and culture allows a business to adapt as unexpected opportunities arise and unforeseen challenges develop.

The investing world requires similar adaptability. At the individual asset level, a thorough investment memo outlines the rationale for a capital allocation decision, an assessment of valuation, and expectations about the development of the business. This forms a disciplined methodology to capture the reasoning behind a decision at the time it is made. It helps to prevent the all too human inclination to project future developments into a past investment decision, usually to the detriment of the investor.

| For example, an investor might rationalize a missed product launch, a key executive departure, the rise of a competitor or an adverse regulatory ruling by remembering (incorrectly) that these risks were part of the original investment thesis. A written and dated plan for the investment prevents this slippery thinking. |

There is a similar benefit to writing things down at the portfolio level. Asset allocation should differ from investor to investor depending on needs for return, desired liquidity, and tolerance for risk or volatility. These needs can change over time, and so, too, should strategic asset allocation.

It is easy, however, to allow market moves to influence asset allocation. Buying more of whatever is going up is tempting, as it feels good to get a positive signal from price moves in the short run. Conversely, it feels good to sell things that are going down, as you no longer need to be reminded of them when you look at your portfolio. Good planning prevents this and even imposes the discipline of rebalancing when one or another asset class rallies sharply.

A robust Investment Policy Statement (IPS), or Statement of Investment Objectives, is particularly valuable in periods of market volatility. Price volatility looms large in bear markets, amplified by breathless media coverage of how far the S&P fell, or how many stocks are making 52-week lows, and so forth. Behavioral psychologists call this an “availability cascade,” as heightened media coverage amplifies bad news, which can induce more selling, which feeds tomorrow’s bad news.

The risk in this environment is that investors naturally feel like they should do something in response to price swings. Yet if an investor is fully invested, the only available action is to sell, which is often the wrong response. A well-crafted IPS acts like a letter from a current composed you to a future anxious you, distracted and depressed by market volatility. Planning helps to win the war against your own emotions.

Conclusion

Investing is complicated, but it’s not complex. Capital is capital, and the prudent allocation of it in business, as well as markets, requires an assessment of quality and value, coupled with the temperament and planning to withstand the temptation posed by price volatility in public markets. There are no guarantees of success in markets or business, but remaining disciplined and patient can help stack the odds in your favor.

If you are interested in learning more about the intersection of business ownership and investing, reach out to your BBH relationship team.

Contact Us

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2026. All rights reserved. PB-09318-2026-02-17