In periods of economic growth and prosperity, funding for small, medium, and large businesses is plentiful. Capital providers are eager to expand their activities. As supply of capital and liquidity increases relative to demand for capital, the terms under which businesses access capital and liquidity loosen.

This creates the best of all possible worlds for consumers of capital: Leverage ratios increase, interest rates decrease, reporting requirements decrease, and covenants and lender protections gradually melt away. These conditions provide business owners the luxury of many options, such as paying down debts, making a long-desired acquisition, paying a dividend, or buying out an aging or inactive shareholder.

However, in periods of economic stress, this virtuous cycle can abruptly shift into reverse. Leverage ratios naturally increase as cash flow generation declines and debt levels remain fixed. Capital providers begin tightening terms as they focus on protecting existing loans and investments as opposed to providing new capital.

The questions facing owners start to change and may include:

- What happens if I violate a covenant in my credit facility?

- What happens to my liquidity if my customers take an extra 30 days to pay their bills?

- Should I defer that capital expenditure or acquisition target to preserve liquidity?

The answers to these questions are unique for each business, but many of our time-tested principles can help guide business owners through periods of volatility. When working with clients to help them think through liquidity risk management, we advise that they implement and maintain a three-pronged strategy:

| 1. First, measure your liquidity early and often. |

|---|

| 2. Second, stress test your liquidity through modeling and forecasting a range of potential scenarios. |

| 3. Finally, craft a strategy to maintain and enhance your access to liquidity. |

Measuring Your Liquidity

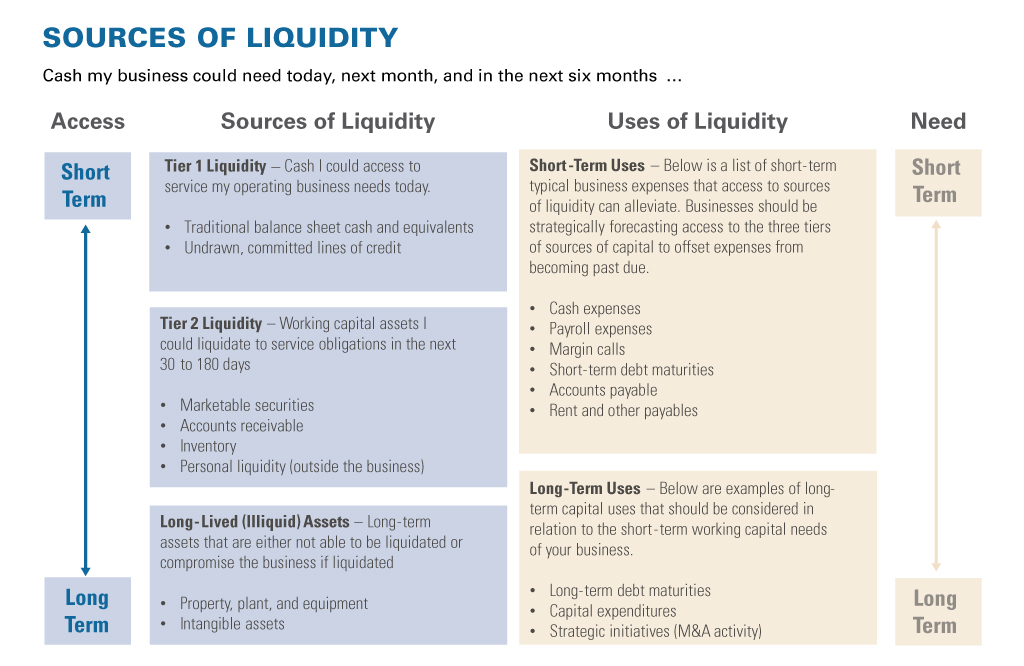

The most common way to measure liquidity is by looking at the ratio of your current assets to current liabilities, or your current ratio. In general, the higher the ratio, the more liquid your balance sheet. The current ratio measures your ability to convert current assets, including cash and cash equivalents, marketable securities, inventory on hand, and accounts receivable to cash. This is measured against obligations you have coming due in the next 12 months.

Other metrics, such as the quick ratio, conduct a similar test but exclude inventory, which – depending on your business – can take longer to convert to cash and may be a necessary working capital investment for your business.

One flaw in these ratios is that in a period of economic stress, cash conversion cycles slow down; quick assets become less quick assets. Receivables take longer to collect, and inventory often takes longer to sell. For clients with highly coveted inventory (the “toilet paper effect” that we saw in March 2020, for example), supply chains can back up. Meanwhile, liabilities tend to have fixed payment dates and maturities and cannot be easily extended.

We advise clients to dissect balance sheet categories and understand how quickly each asset can be converted to cash and at what value. Traditional cash should be easy, and the value should be fairly certain. However, make sure “cash” really means cash.

Is the money in an overnight demand deposit at an FDIC-insured bank? A money market fund with daily liquidity? Or could it be a liquid investment with potential to decline in value?

The value of marketable securities may have declined; as such, you may prefer not to tap these resources immediately. Setting up a line of credit with your investment advisor can help you avoid liquidating long-term investments at the worst time.

Be conservative in valuing current assets; assume late payments on accounts receivable and soften demand/price reductions for inventory. And assume you may be faced with the difficult decision of selling inventory at a discount to raise liquidity and meet obligations, without incurring unacceptable losses.

Private business owners may also factor in their personal balance sheet during liquidity measurement. Maintaining dry powder outside of the business can be a valuable tool to quickly improve funding liquidity. For businesses with a single owner, the process of adding capital to your business is fairly straightforward, but for partnerships or family businesses with multiple shareholders, the process can be more complicated and require lengthy structuring and negotiation. In such situations, shareholder loans to the business may be the optimal structure.

This table shows sources of Liquidity: short term to long term sources (cash, working capital, long-term assets), uses and need

Liquidity Forecasting

The best-managed businesses build liquidity forecasting into their enterprise risk processes. This financial modeling exercise involves projecting a slowdown in cash receipts while demands on cash resources increase.

- For example, what happens if your sales slow by 20% over the next three months, receivables take 30 days longer than usual to collect, and you have to change vendor payment terms to cash against documents or prepayment to secure scarce raw materials?

- In an extreme scenario, what happens if revenue slows to a halt? How much cash do you have to survive four weeks of virtually no revenue? Eight weeks?

- Are there unforeseen cash needs that could arise due to economic stress – requirements to cure a breached lender covenant or a margin call to a derivative counterparty?

Suffice it to say that in periods of stress, businesses will often put liquidity over profits in the short term. The ability to perform with your suppliers and customers is a function of liquidity in the short term and will likely provide commercial opportunities that position you for growth when the stress ultimately subsides.

Managing Debt and Liquidity

What happens to credit facilities when revenue declines, accounts receivable collections slow, and inventory accumulates? Liquidity structures governed by borrowing bases or asset-based structures naturally constrict available liquidity. Companies borrowing on cash multiples (for example, debt/EBITDA) may edge closer to breaching covenants due to declining EBITDA. If you expect to violate covenants or have issues with eligible collateral, you should proactively communicate with your lender. Lenders are more likely to respond positively if they are aware of problems in advance.

Periods of volatility may also affect lenders’ own liquidity profiles, creating a knock-on effect on their borrowers. Direct lending funds may have rising defaults in their portfolio, restricting access to the bank liquidity they use to fund loans. Traditional banks may be more focused on managing credit issues with existing clients than lending new money.

Funding costs could be rising, especially for lenders with no natural deposit base. Understanding how your lender funds itself is critical. Does it have a natural deposit in the U.S.? Or must it access funding in the wholesale market? Does the bank have any sector concentrations in its loan portfolio that could expose it more to credit losses in this environment?

A Strategic Approach – Liquidity over Profits

Liquidity is the lifeblood of business. This truism becomes even more apparent in periods of economic duress. Understanding, measuring, and forecasting your liquidity position is crucial to enduring periods of economic contraction and ensuring your business continues to thrive as economic conditions improve.

Business owners have many helpful tools. Consider liquidating inventory to raise liquidity, even at the expense of short-term profitability. Develop a communication plan with all of your stakeholders; overcommunicate with your customers, and be ready for payment delays. Negotiate extended payment terms with your vendors if necessary. In order to enhance your liquidity position, it’s important to have these challenging conversations with all of your stakeholders: employees, customers, vendors, landlords, and even lenders. How you manage each stakeholder will directly affect your liquidity position. For the businesses most affected, buying “insurance” to increase liquidity may be worth the temporary hit to profits.

Businesses with strong liquidity positions will weather the storm. History suggests some of the best, highest-returning capital allocation decisions are made in periods of duress. Those who proactively develop the tools to manage liquidity in volatile periods will have the best opportunities to grow again when the sun shines once more.

If you would like to discuss how to effectively manage your business’s liquidity, particularly during times of uncertainty and volatility, please reach out to our Corporate Advisory & Banking team.

Contact Us

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07534-2024-06-27