Thoughtful estate planning is essential for business owners who want to preserve the value of their estate, minimize transfer taxes, and ensure the smooth transition of their business to the next generation. As we approach 2025, understanding and utilizing the gift tax exemption is more important than ever. In our second annual Private Business Owner Survey, 74% of participants indicated an intention to do additional planning before the end of 2025 to take advantage of the historically high gift tax exemption amount.

74% of owners intend to take advantage of the gift tax exemption before the end of 2025

What is the lifetime gift tax exemption, and why are we focused on it now?

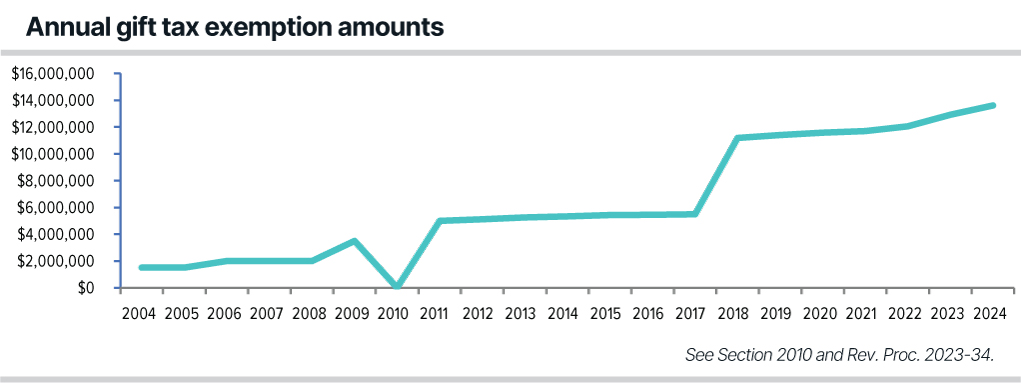

The lifetime gift tax exemption is an amount individuals can transfer to others without incurring a federal gift tax liability. In 2024, the exemption from gift tax is $13.61 million per person, or $27.22 million per married couple. Thomson Reuters is projecting the exemption to be $13.99 million per person in 2025, or $27.98 million per married couple. The applicable federal tax rate on transfers over the exemption amount is 40%.

Prior to 2018, the gift tax exemption was $5 million, adjusted annually for inflation. The 2017 Tax Cuts and Jobs Act (TCJA) doubled the exemption to $10 million, adjusted annually for inflation, from 2018 through 2025. Under the TCJA, the increased exemption amount will sunset (or expire) at the end of 2025.

Unless there is intervening legislation (requiring some level of consensus in Congress and the White House), the outcome will be a federal gift tax exemption of approximately $7 million as of January 1, 2026 (or approximately $14 million for married couples).1

As a result, many individuals are considering making gifts up to the current exemption amount before that opportunity goes away in 2026.

| Note: These numbers are the same for the estate tax exemption, but this article focuses on lifetime planning. |

| Year | Exemption |

|---|---|

| 2004 | $1,500,000 |

| 2005 | $1,500,000 |

| 2006 | $2,000,000 |

| 2007 | $2,000,000 |

| 2008 | $2,000,000 |

| 2009 | $3,500,000 |

| 2010 | $0 |

| 2011 | $5,000,000 |

| 2012 | $5,120,000 |

| 2013 | $5,250,000 |

| 2014 | $5,340,000 |

| 2015 | $5,430,000 |

| 2016 | $5,450,000 |

| 2017 | $5,490,000 |

| 2018 | $11,180,000 |

| 2019 | $11,400,000 |

| 2020 | $11,580,000 |

| 2021 | $11,700,000 |

| 2022 | $12,060,000 |

| 2023 | $12,920,000 |

| 2024 | $13,610,000 |

Planning opportunities for business owners

For business owners, estate planning is not just about identifying beneficiaries for personal property or investment accounts. It often involves strategies aimed at:

- Transferring ownership of the business to the next generation

- Minimizing the tax consequences of such a transfer

- Planning for sufficient liquidity to cover estate taxes or buy-sell agreements

- Preparing for a smooth transition of operational responsibilities

- Communicating the plan to the family

The following opportunities relate specifically to business owners leveraging their remaining gift tax exemption to minimize the tax consequences of transferring ownership of the business to the next generation.

Gifting an interest in a privately held business is an effective way to use up one’s exemption for a number of reasons, including:

- Reducing the size of your taxable estate

- Allowing future appreciation in the business to accrue outside of your estate

- Minimizing the family’s overall tax liability

In addition, when you gift an interest in a privately held business, you must obtain a valuation for purposes of reporting the gift. When valuing the interest, appraisers take into account factors like the marketability of the asset and the control or voting rights associated with it.

Typically, appraisers will take a discount for lack of marketability when assessing the value of a privately held business interest. This is because there is not a readily accessible market for it in the way there is for liquid investments or publicly traded stocks.

Appraisers will also reduce the valuation when the gifted interest is a minority stake in the company or does not have voting rights. The application of these discounts decreases the value of the gift for gift tax purposes, thereby maximizing the amount of the business you are able to transfer using your remaining gift tax exemption.

The most common way to transfer interests in a business is through outright gifts or gifts to irrevocable trusts.

- Outright gifts: The simplest option is to make an outright gift of shares of stock in a corporation or interests in a partnership or LLC. The recipient will be a new owner of the business. You will need to commission an appraisal to determine the value of the transferred interest and file a gift tax return to report the gift.

- Gifts to a trust: The combination of valuation discounts and gifting to a trust (rather than outright) maximizes the amount that you can transfer without the imposition of gift tax. It also minimizes not only your estate taxes, but those of future generations.

In addition, the trust structure allows more than one person to benefit from this gift. For example, you could gift a 40% interest in your business to a trust for the benefit of your spouse and your descendants. The cash flow from that interest could be distributed to any or all of the beneficiaries of the trust, or it could be accumulated for the future.

The appreciation in value of that business interest would occur outside of your estate (and therefore would not be subject to estate taxes at your death) and outside of the beneficiaries’ estates (and therefore would not be subject to estate taxes at their death).

If this transfer is made to a trust that benefits your spouse, commonly referred to as a spousal lifetime access trust (SLAT), then your spouse (and you, indirectly through your spouse, as long as your spouse is living and you are married) can benefit from distributions from the trust. This flexibility often provides comfort when making a large gift because it allows you to get assets (and future appreciation on those assets) out of your estate for estate tax purposes while still having a way to access those funds if necessary.

You can maximize the tax efficiency of your gift by making it to a grantor trust, or one that requires you to pay income taxes, thereby allowing you to further reduce your estate and the trust principal to grow free of income tax liability.

Layered onto discount planning, some business owners have unique opportunities based on the structure of their business. For example:

- Qualified small business stock (QSBS): If your shares in the business meet the requirements for QSBS, then not only can you use those shares to plan for your family, but you may also be able to reduce your eventual capital gains tax liability when the business is sold. The interest must be:

- Shares in a C corporation

- Acquired at original issuance directly from the company

- Operating a qualified active trade or business

- With less than $50 million of assets at the time you invested

- Held for at least five years

- Carried interests/profits interest: If you are a private equity (or other) fund principal with a carried interest, you can take advantage of the typically low initial valuation of your carried interest by transferring it, along with a proportionate share or “vertical slice” of all other interests you own in the fund, to an irrevocable grantor trust.

A practical example of gift tax exemption utilization Imagine you own a family business with a fair market value of $100 million. You gift a 20% interest in the business to a trust for the benefit of your spouse and descendants. That interest would be worth $20 million if the business were sold tomorrow, but in valuing the gift, the appraisers apply a 32% combined discount for lack of marketability and lack of control. The result is a value for gift tax purposes of $13.6 million. Since the gift tax exemption is $13.61 million in 2024, you owe no gift tax. In this example, you successfully transferred 20% of the family business out of your estate without the imposition of gift tax. If the value of the business doubles over the next five years and you decide to sell it, the trust’s share will then be worth $40 million. That is $40 million that would be outside of your estate for estate tax purposes, and outside of your descendants’ estates as well, if the trust was a properly created dynasty trust. To further highlight the effectiveness of gifting interest in a family business, consider an alternative scenario: If you had instead gifted $20 million of cash to a trust for the benefit of your spouse and descendants, you would owe approximately $2.5 million in gift tax. |

Conclusion

As we look ahead to 2025, we encourage business owners to consider leveraging their gift tax exemption. It is a powerful tool for those seeking to optimize tax efficiency prior to the exemption being cut in half on January 1, 2026 (absent intervening legislation). Effective estate planning minimizes taxes while helping to secure a stable future for both your family and your business.

If you have already used up your gift tax exemption, don’t fret. There are some alternative strategies available – most commonly, sales to grantor trusts and grantor retained annuity trusts (GRATs). |

These issues are complex and should be discussed with advisors who have deep expertise in these areas. If you have questions or wish to speak about anything covered in further detail, reach out to your BBH relationship team.

Neither Brown Brothers Harriman, its affiliates, nor its financial professionals render tax or legal advice. Please consult with an attorney, accountant, and/or tax advisor for advice concerning your particular circumstances.

1 There is also a gift tax annual exclusion, which is $18,000 per recipient in 2024. Thomson Reuters projects the annual exclusion to increase to $19,000 per recipient in 2025. This article is not focused on the annual exclusion from gift tax because there is no expectation of a reduction to or loss of this exclusion.

Brown Brothers Harriman (“BBH”) is not affiliated with and does not endorse the views of any third-party publications linked to this issue. BBH was not involved in the preparation and is not responsible for the content, accuracy, completeness, or fairness of such information. BBH makes no representations, guarantees or warranties of any kind regarding such information. Any such information is intended for informational purposes only, and any views or opinions expressed therein are the views or opinions of that third party.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07802-2024-10-08