Chart comparing the annualized excess returns of global, U.S., and non-U.S. funds by the 20th, 40th, 60th, and 80th percentiles. The latest figures are as follows: 20th percentile - 3.7%, 2.7%, 2.3%; 40th - 1.8%, 1.2%, 1.0%; 60th - -.01%, 0.3%, 0.2%; and 80th - -1.8%, -0.7%, -0.8%, respectively.

Go global? Or invest at home? Despite recent years of strong outperformance by the Magnificent Seven-led1 U.S. market, we believe international and global equities,2 including developed and emerging markets, can play a valuable role in a well-constructed portfolio – especially amid the current economic and geopolitical uncertainty.

Great companies can be found around the world, and strong investment managers are able to benefit from having the ability to invest in those stocks. By high-quality, in this case we mean top-quartile, international equity managers can be a portfolio return enhancer as well as a portfolio diversifier, particularly when combined with different sector exposures and disciplined rebalancing.

Great companies can be found around the world, and strong investment managers are able to benefit from having the ability to invest in those stocks.

Enhanced portfolio returns

We believe that high-quality international and global equity managers can generate compelling returns via strong alpha generation opportunities due to a larger investment universe and less-efficient markets. By alpha we mean performance relative to a benchmark.

Larger universe + less-efficient markets = opportunity for alpha generation

Let’s break down the components of this equation.

Larger investment universe: Despite the fact that U.S. companies comprise roughly 63% of the global public equity market cap, nearly 90% of the world’s publicly-traded companies exist outside of the U.S. This large investment universe is not fully captured by passive indices, which have strict inclusion eligibility (such as sufficient liquidity, available float, or adequate reporting requirements, to name a few). This is seen when comparing the MSCI ACWI ex. U.S. ETF, which holds 1,706 companies, to the broader universe of approximately 44,000 publicly traded non-U.S. companies.

Less-efficient markets: International equity markets are generally more inefficient due to a combination of less sell-side analyst coverage, a higher number of international companies, and different financial reporting standards. In particular, a lack of sell-side analyst coverage—which can result in less information or inaccurate pricing — presents an opportunity for sophisticated fund managers to exploit and potentially create substantial value for their investors.

As an example, in Europe, the financial regulatory directive MiFID II, which was introduced in 2018, increased the expense of outsourcing European equity research to banks. A 2020 study by researchers in the U.S. and Canada found that 334 companies lost all analyst coverage completely in less than two years following the legislation.3 The picture is different in the U.S. where, according to Bloomberg, the average S&P 500 stock has 23 analysts covering it and the average DOW-listed company has a coverage of 36 analysts.

In addition to less analyst coverage abroad, the quality of data available also tends to be inferior. As an example, in the U.S. many equity managers purchase consumer debit and credit card data to determine which retailers are above or below their published revenue estimates. This type of data is generally harder to come by internationally as the markets in various countries is smaller, making it harder to get sizeable representative data sets.

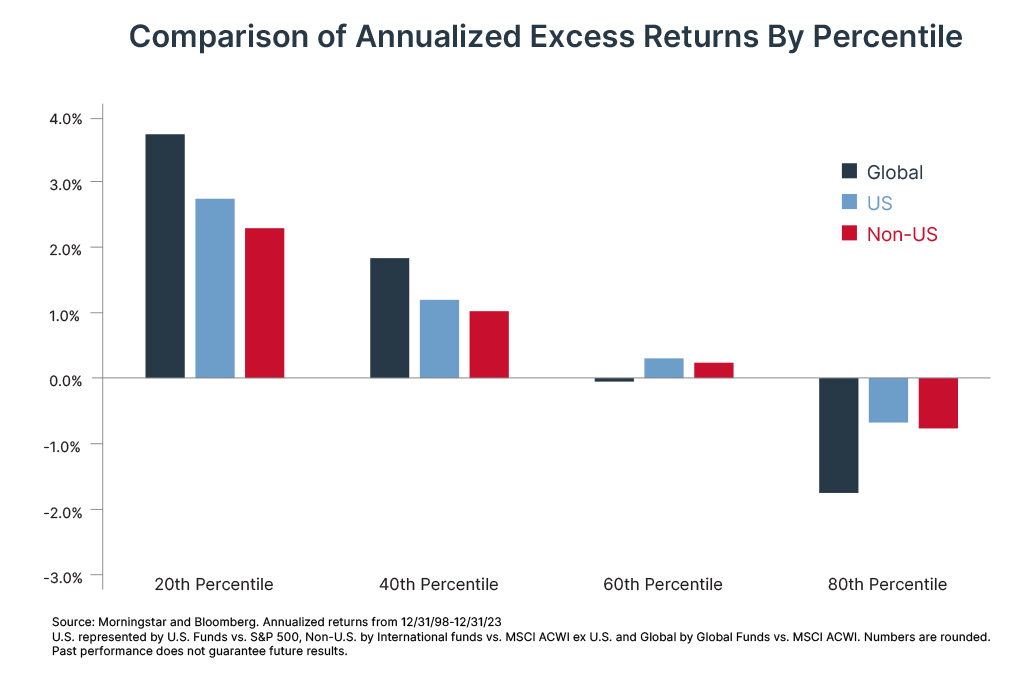

Opportunity for alpha generation: A large opportunity set, with approximately 44,000 publicly-traded international companies, as well as less efficient markets, creates the opportunity for greater alpha generation in international equity markets. Our research finds that the top-performing global and international funds have generated more excess return than U.S.-focused equity managers.

According to Morningstar, the top quintile of global funds exceeded the annualized return of the MSCI ACWI Index by roughly 250 basis points4 from December 1998 to December 2023, while the top quintile of U.S. funds exceeded the annualized return of the S&P 500 by roughly 70 basis points.

Skilled international and global equity managers have been able to generate significant outperformance over their representative index. This is even in spite of potential macroeconomic headwinds, particularly from currency movements.

| Across the BBH platform, our public equity managers (including international and global equities) are highly selective, scouring a vast investment universe to select only a handful of the best companies. To build their concentrated portfolios, our managers perform rigorous bottom-up research in order to find exceptional companies around the world. Common criteria for our managers include predictable earnings and free cash flow growth, strong returns on invested capital, well-established barriers to entry, and strong management teams with good capital allocation skills. |

Portfolio diversification

Along with greater opportunities for alpha generation, owning international equities as part of a larger equity portfolio provides helpful portfolio diversification through:

Stock market leadership has alternated between U.S. and developed international numerous times over the past 50 years and between the U.S. and emerging markets over the past 30 years. There have been lengthy periods of both outperformance and underperformance of U.S. stocks relative to international stocks. The cyclicality of returns implies that exposure to more than one asset class can benefit a portfolio over time, as long as the cycles of different investments are not perfectly correlated. Each region can exhibit sustained periods of outperformance, sometimes lasting from a few years to over a decade.

Chart depicting the MSCI USA vs. MSCI EAFE rolling 36-months returns, where blue means MSCI USA outperformance and red means MSCI EAFE outperformance. The latest figure is 5% as of February 28, 2025.

International stocks can provide an important source of diversification through a larger and differentiated opportunity set. The U.S. market (as represented by the S&P 500) is more concentrated in the technology and healthcare sectors, while non-U.S. equities (as represented by the MSCI ACWI ex. U.S. Index) provides more exposure to financials, industrials, and consumer staples. In comparison, Europe offers exposure to opportunities not available in the U.S. Specifically, Europe dominates the luxury goods space (the luxury goods sub-industry holds 3.1% weight in the MSCI EAFE vs. 0.3% in the S&P 500) and is at the forefront of the energy transition, as 75% of offshore wind capacity is installed in Europe.

| Sector | S&P 500 | MSCI ACWI ex. U.S. |

| Tech | 30.7% | 13.0% |

| Financials | 14.5% | 24.2% |

| Health Care | 10.6% | 8.9% |

| Cons Disc | 10.5% | 11.4% |

| Comm Services | 9.5% | 6.2% |

| Industrials | 8.3% | 13.8% |

| Cons Staples | 5.9% | 6.5% |

| Energy | 3.3% | 4.7% |

| Utilities | 2.4% | 2.9% |

| Real Estate | 2.2% | 1.7% |

| Materials | 2.0% | 6.2% |

Investors can increase diversification by holding securities denominated in various currencies, each of which may enhance or detract from U.S. dollar returns at a given point in time based on changes to the exchange rate. Currency exchange rates are influenced by a great number of factors including inflation, interest rates, speculation, government debt, and balance of payments.

Dollar strength is equivalent to foreign currency weakness, which poses stiff headwinds to the returns of asset classes denominated in other currencies when those returns are translated into dollars. For example, if a South Korean stock rises 10%, but the dollar strengthens 12% against the won, the net return to a dollar-based investor is -2%, all else equal.

However, the opposite holds true when the dollar depreciates relative to a basket of global currencies, thereby boosting the returns of international stocks in dollar terms. The nearby chart shows the returns of domestic, international, and emerging equities in two different time periods: when the U.S. dollar is appreciating and when the U.S. dollar is depreciating.

| S&P 500 | MSCI EAFE ($ returns) | MSCI EM ($ returns) | |

| 2002-2008 (weaker U.S. dollar) | 3.5% | 11.1% | 22.1% |

| 2011-2014 (stronger U.S. dollar) | 13.6% | 4.9% | 1.9% |

As the dollar strengthened between 2011 and 2024, developed markets (as measured by the MSCI EAFE Index) lagged the U.S. by an annualized 8.7%, while emerging markets (as measured by the MSCI EM Index) lagged by 11.7% annually. However, from 2002 to 2008, the opposite was true: a weakening dollar magnified international returns. MSCI EAFE outpaced the S&P 500 by 7.6% annually, while emerging markets posted annualized returns that were 18.6% better than domestic equities. Across our portfolios, currency exposure is an output of our bottom-up, fundamental process. We do not actively seek to invest in a specific region to gain exposure to its currency. Given our criteria of investing in superior business models with a high probability of compounding value over the long-term, our public equity portfolio tends to have more exposure to the U.S. dollar and the euro (about 80% of the portfolio on a look-through basis with the balance across 18 other currencies). Having exposure to securities denominated in foreign currencies helps reduce the correlation of the portfolio to U.S. equities, thereby reducing the volatility of the overall portfolio.

Key takeaways

We believe that over the long term, international equities can play valuable roles in a well-constructed portfolio:

- Opportunities for strong alpha generation due to a larger investment universe and less-efficient markets

- Portfolio diversification through sector exposure, opportunity set, and currency exposure

At BBH, we take a methodical approach to investing in international markets by working with active managers that meet our strict criteria. To learn more about our strategic allocation to international equities, reach out to your BBH relationship team or the Investment Research Group.

Contact Us

1 Magnificent Seven stocks include Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla.

2 When using the term “international equities,” we are referring to non-U.S. equities across developed and emerging markets, while the opportunity set in global equities is inclusive of both U.S. and non-U.S. equities.

3 Fang, Bingxu and Hope, Ole-Kristian and Huang, Zhongwei and Moldovan, Rucsandra, The Effects of MiFID II on Sell-Side Analysts, Buy-Side Analysts, and Firms (May 8, 2020). Rotman School of Management Working Paper No. 3422155, Available at SSRN: https://ssrn.com/abstract=3422155 or http://dx.doi.org/10.2139/ssrn.3422155

4 One basis point or bp is 1/100th of a percent (0.01% or 0.0001).

References to specific securities, asset classes, and financial markets are for informative purposes only and are not intended to be and should not be interpreted as recommendations.

International investing involves special risks including currency risk, increased volatility, political risks, and differences in auditing and other financial standards.

Prices of emerging market securities can be significantly more volatile than the prices of securities in developed countries, and currency risk and political risks are accentuated in emerging markets.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-08411-2025-03-28