What Role Does the Federal Reserve Play?

In the wake of the inflation of the early 1970s, Congress explicitly handed responsibility for managing inflation to the Federal Reserve, the central bank of the United States. The Federal Reserve Reform Act of 1977 requires the Fed to “promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates.”

In its pursuit of price stability, the Federal Reserve is more concerned with restraining demand-driven, or wage-driven, inflation, for the simple reason that monetary policy has little influence on supply issues. Fed policy cannot address the weather in Florida or the health of Brazilian coffee crops. The Fed’s so-called dual mandate requires it to balance the strength of the labor market with the risk that too much employment growth might lead to wage-driven inflation.

Historically, this has required the Fed to walk a fine line in keeping interest rates low enough to support economic activity and hiring, but not so low that a booming economy leads to excessive wage gains and inflation. This has been an easy exercise over the past decade, at least in retrospect, as the Fed has been more concerned with the risk of deflation than inflation. As a result, the Fed has been able to keep interest rates low for an extended period without allowing inflation to creep into the economy.

In fact, as interest rates in the United States approached zero in the 2008/2009 financial crisis, the Fed added to its policy arsenal by expanding the size of its balance sheet through so-called quantitative easing. This involves the Federal Reserve buying fixed income assets from financial institutions in the open market and paying for those purchases by crediting the seller with newly created reserves held at the Fed. Buying assets allows the Fed to exert further downward pressure on interest rates (bond yields go down as prices go up) while boosting bank reserves in an effort to incentivize lending. More lending translates into more business expansion, home purchases, renovation, consumption, et cetera – and consumption, broadly defined, drives almost 70% of gross domestic product (GDP). Through various rounds of quantitative easing, the Federal Reserve grew the size of its assets from about $900 billion in summer 2008 to the current level of roughly $4.5 trillion.

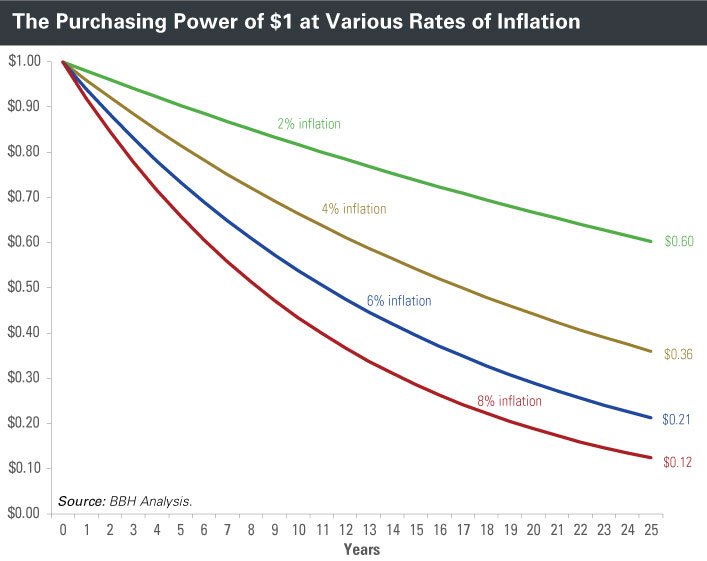

In expanding the size of its balance sheet so dramatically, the Fed runs the risk of falling short on its commitment to keeping prices stable. The laws of supply and demand apply to money as much as to goods and services, and expanding the amount of money in circulation or available for lending raises the risk of inflation. We normally think of inflation as a rise in the price of goods, but this is equivalent to a fall in the value, or the purchasing power, of the dollar. Rising prices and falling purchasing power are two sides of the same coin.

The economist Irving Fisher referred to this as the “money illusion” in a 1928 book with that title. The illusion is that the dollar is stable while prices fluctuate, which Fisher compared to the pre-Copernican notion that Earth remained still while the rest of the heavens revolved around it. The astronomical and monetary reality is that everything is moving and that the supply of and demand for dollars can affect the market price of goods as much as the supply of and demand for the goods themselves.

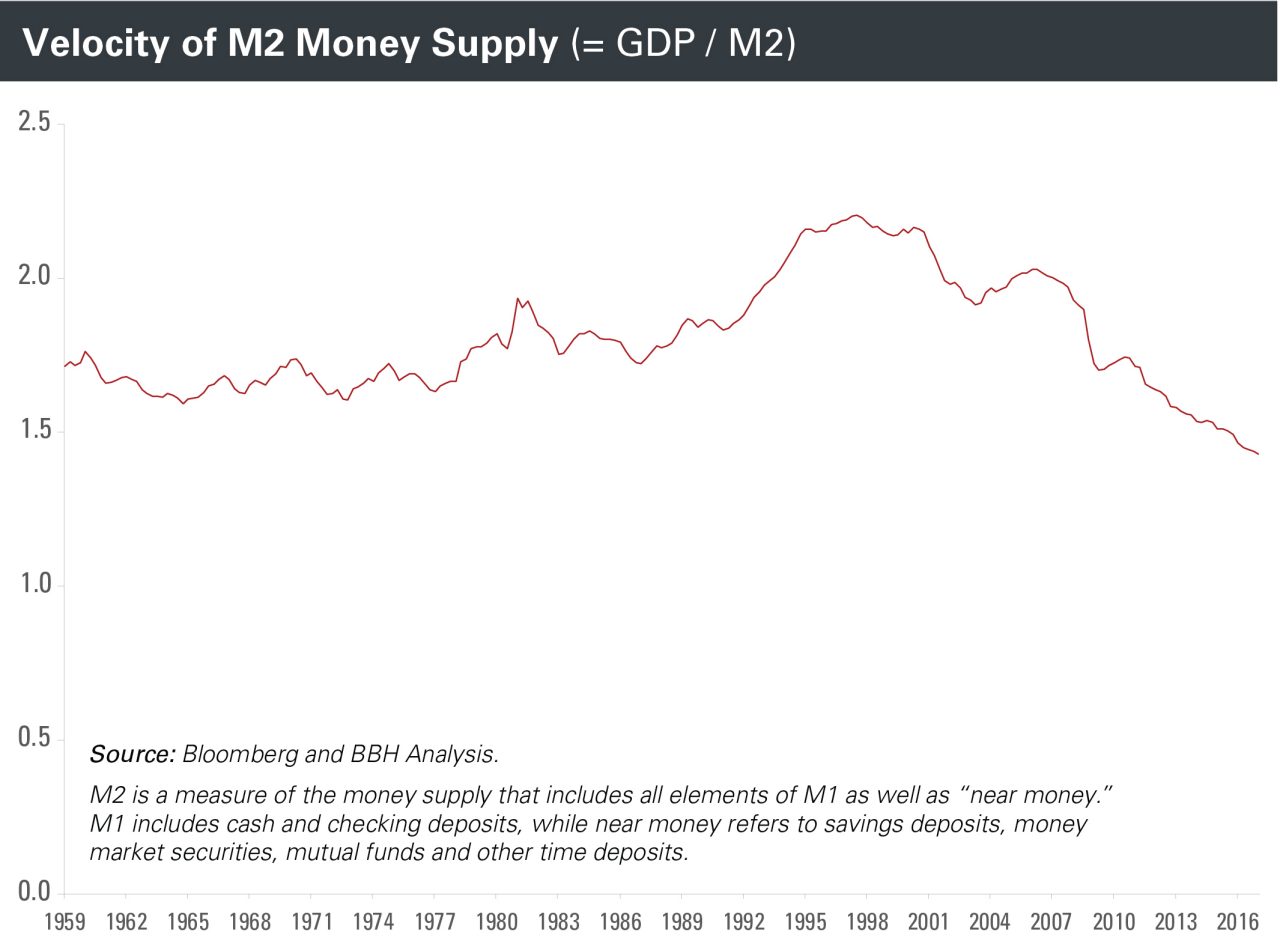

Money Supply and Velocity

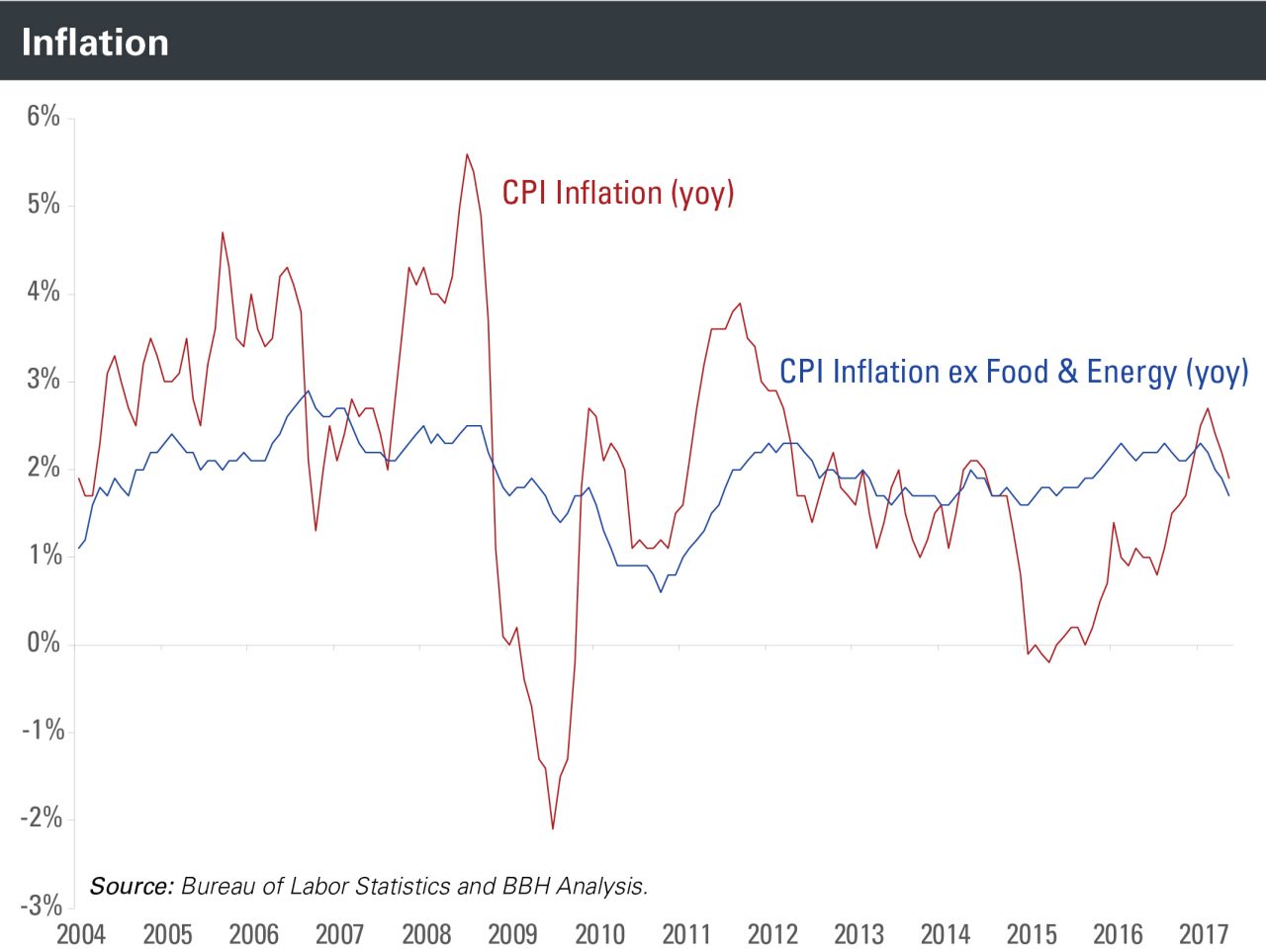

And yet, as the earlier graph demonstrates, even with zero interest rates and a fivefold increase in the size of the Fed’s balance sheet, prices and wages remained stagnant. Why? Because money is inflationary only if it moves. If I pay someone $100 and she does nothing with the income, there is no impact on demand or prices. This is the monetary concept of velocity, which measures how many times money transfers from one economic actor to another, influencing prices with every move. In this example, my $100 payment represents a velocity of 1, as the money only changes hands once. If, on the other hand, the recipient of my $100 subsequently spends $50 on dinner and a movie and $50 on a taxi to get home, the velocity rises to 2 ($200 in aggregate money flows divided by a total of just $100 in circulation). My spending is someone else’s income, and the more times that happens, the greater the velocity and the more pressure on prices. Expand this simple example to about $13 trillion, and you get the U.S. money supply. At the aggregate economic level, money velocity is GDP divided by the total supply of money (including cash and bank deposits).

As the nearby graph shows, in spite of modestly rising wages and the growth in the Fed’s balance sheet, money in the U.S. economy is moving increasingly slowly. The absolute level of money in circulation is at an all-time high, but the movement of that money is at an all-time low. From a peak of 2.2 in the third quarter of 1997, the velocity of money has slowed to a low of 1.4 as of the first quarter of this year.