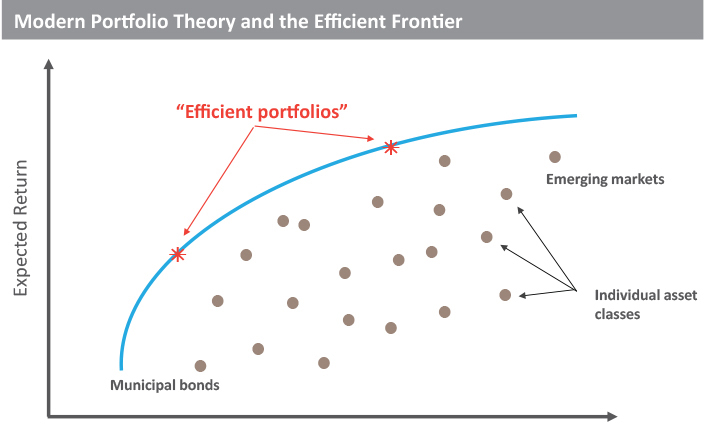

The mathematics of modern portfolio theory are elegant but rarely reflect the reality of markets. First, the theory requires a forecast of future return, volatility and correlation. Practitioners typically rely on the past as an indication of the future, but the past is a fickle guide, and is furthermore not normally distributed across a typical bell curve. In addition, MPT defines risk as price volatility, whereas most investors hold that risk is more accurately defined as the permanent impairment of capital. Short-term price volatility poses no risk to a longer-term investor. Finally, MPT relies on various asset classes having less-than-perfect correlation, whereas in periods of market stress, global asset classes tend to move together. Correlations rise along with fear, and the benefits of diversification evaporate.4

Perhaps the most significant shortcoming of modern portfolio theory is the claim that investors are rational. The entire field of behavioral economics disputes this assumption, as does a glance at market action during periods of stress. Fear, panic, greed and hope play important roles in creating the deviation between price and value that disciplined investors can exploit.

Asset Allocation at Brown Brothers Harriman

Rather than attempt to predict future price movements and correlations, asset allocation should instead reflect an investor’s specific needs. Portfolio construction is essentially an exercise in balance sheet management. Individuals and families have assets and liabilities, just like companies. Family liabilities might comprise future tuition payments, the desire to retire at a certain age, to live a certain lifestyle, to engage in philanthropy, to leave wealth to future generations and so forth. Admittedly, many of these goals are not liabilities in the strictest sense of the word, but the important insight is that current asset allocation should reflect both current and future spending objectives. Furthermore, the risks associated with future spending, of which inflation looms large, should be reflected on the asset side of the balance sheet as well.

For example, a young investor with a steady income who is still building wealth is better positioned to weather shorter-term price volatility. Furthermore, even modest inflation poses a threat to future spending needs many years from now when she plans to retire. Growing her wealth and protecting it against inflation would lead to a robust exposure to equity-like assets – not because of an optimization of risk and return, but because the nature and longevity of her liabilities warrant it. Conversely, a retired investor who lives off of his portfolio might have a greater need for liquidity to pay bills, thereby calling for a higher exposure to traditional fixed income.

The asset allocation exercise is both an art and a science, which is why relationship managers at BBH spend so much time understanding a client’s whole financial picture before arriving at the right asset allocation.

Capital Allocation at Brown Brothers Harriman

So much for the “where” of asset allocation. We now turn to the “how” – that is, the implementation of a client-specific asset allocation through allocating capital to various managers.

The core of our capital allocation approach is the search for talented managers to partner with for the long term. Contrary to popular belief, outperformance generally comes from the value added by active managers, not from tactical changes to asset class weights. Because of this, we have designed our investment process in a way that does not oblige us to hit predetermined asset class target weights set by a committee. While various investment team members have particular areas of investment expertise, we are all generalists, and as such have no duty to recommend a certain number of managers within an assigned asset. In our experience, that would lead to suboptimal decision-making where capital might be allocated to second-tier managers merely to comply with asset class targets.

Each investment opportunity is evaluated individually and against all competing opportunities from a risk and return perspective, and our process instead aims to steer capital toward our highest conviction managers. Overlaid on top of this is a disciplined risk management framework that prevents us from taking on large, unintended exposures that might result from our bottom-up process. Importantly, we manage overall portfolio risk by looking through to the underlying exposure in each of our managers’ portfolios. Accordingly, our policy portfolio weights with which clients are familiar are generally the result of bottom-up investment decisions.

This investment process differs from approaches common in the investment industry. First, we have an integrated capital allocation and manager research team. Team members are responsible for everything from initial screens to in-depth due diligence and eventually position sizing or capital allocation decisions. Instead of quarterly investment committee meetings, our team has formal meetings multiple times per week and maintains a constant dialogue as it relates to our managers, their holdings and the market environments in which they operate. Second, our approach can lead us to pass on entire asset classes where we cannot find a manager who meets our stringent criteria.5 Our approach to investing is squarely focused on owning assets or businesses, rather than markets or geographies. We insist on knowing what we own and why we own it, and if we cannot find quality investments in a given area of the market and a manager who executes well with regard to a particular opportunity set, we simply pass even though these investments are part of the global opportunity set that many feel compelled to allocate to. Examples of this include master limited partnerships (MLPs) and direct commodity investments. If we are not comfortable with the manager, its approach and alignment and the specific investments it owns, we prefer to allocate capital to another opportunity.

A Bottom-Up Approach to Risk Management

Modern portfolio theory leads to risk management through diversification. At an extreme, the investor winds up owning the entire market, regardless of whether the market itself poses unacceptable risk.

At BBH, our most fundamental investment belief is that the long-term equity ownership of high-quality businesses – with an emphasis on purchasing these businesses at a discount to their conservatively estimated intrinsic value6 and selling them when fully valued – is the surest way to preserve capital and to generate a real return on capital over time. Furthermore, the ownership of a concentrated number of strategies that own a concentrated portfolio of businesses or assets that we know well is our most consistent and dependable tool to manage risk and avoid capital impairment.

In our opinion, most investors derive a false sense of comfort from diversification alone as a risk management tool. While we monitor our risk concentrations across the asset classes listed in our policy portfolios as well as a range of other factors such as currency, country and market cap, we do not count on forecasted correlations among asset classes to get us out of trouble in a weak economic environment. History has shown that most major global equity asset classes move together in close step during bear markets, which is precisely the environment in which investors count on this diversification benefit to work in their favor. U.S. small-cap stocks, to pick one example, vary widely in their risk characteristics and should not be thought of as a homogeneous group. They range from stable, cash-generative businesses with proven business models and strong competitive advantages to highly leveraged companies that burn cash and are reliant on leveraged capital markets for continued funding.

Our approach has the disadvantage that it does not reduce risk to a single number, although we believe it is more intellectually honest. While portfolio volatility may be quantifiable, it does not truly represent investment risk for a longer-term investor, and we prefer the more productive, but challenging, endeavor of assembling a portfolio of investments where we know what we own and why we own them. Beyond this, we think about potential macro risks that could impair our capital. An investor we met with once described this as investing bottom-up, but worrying top-down, which we think is the framework to building out global multi-asset class portfolios.

Understanding Market Cycles and Dislocations

Whereas we do not make investment decisions based on macroeconomic forecasts, we believe strongly in being macro-aware. Though understanding the current macroeconomic environment can never hurt, it has particular applicability to some of the highly cyclical asset classes we invest in, such as high-yield bonds, distressed debt and real estate. In addition to earning returns by owning high-quality businesses for the long term, we believe it is possible to earn attractive risk-adjusted returns by allocating capital into market dislocations of more cyclical asset classes. Such opportunities are rare and typically happen at most once per market cycle, but constantly monitoring markets for these opportunities is a key component of our investment process. As opposed to opining on minute differences in P/E ratios of different equity markets, we look for true dislocations where market prices vastly understate the intrinsic value of investments.

We look to take advantage of market dislocations in less cyclical asset classes too, which usually are created by unexpected macroeconomic or political events. Periods of high uncertainty typically lead to indiscriminate selling and opportunities for prices to overshoot on the downside. While we will never make a contrarian investment for the sake of being contrarian, we prioritize due diligence efforts to out-of-favor areas.

We believe this more prudent approach to our investment offering starts with partnering with managers that meet our stringent criteria and then blends a combination of their own bottom-up insights and recommendations about their opportunity sets and our top-down observations about risks and opportunities in certain asset classes. Neither BBH, nor our managers, should think about the macro environment in isolation. We seek to partner with managers where we maintain an ongoing dialogue about the attractiveness of their opportunity set. We hope to be the first call for additional capital when market volatility presents an opportunity to put capital to work, and conversely, we are completely comfortable with allowing managers to build cash in their portfolios if they cannot find enough investments that meet their standards.

When it comes to the cyclical asset classes that we invest in, we do not aim to tactically shift our positioning multiple times per cycle. Many allocators seem to feel that constantly making portfolio changes is an exercise necessary to justify their existence, but as short-term market moves are mostly based on sentiment, constantly shifting policy allocations is not a repeatable path to outperformance. An example of this type of thinking in action was our position in high-yield bonds from October 2011 to June 2014.

Conclusion

Successful portfolio construction requires asset allocation driven by an investor’s needs, along with capital allocation driven by partnering with managers who invest fundamentally with an insistence on value. At BBH, we follow a bottom-up process to building portfolios, which we believe is the surest way to generate solid long-term investment results and mitigate risk. We shy away from the common industry practice of constantly shifting portfolio weights based on short-term market moves, and instead aim to own high-quality businesses and assets through managers we partner with for the long run and to carefully deploy capital into occasional market dislocations. While we are constantly learning about the current state of the macroeconomic environment, we are mindful of the limitations of economic forecasting. Through full market cycles, we believe our bottom-up focus and macro-aware approach to risk management will produce attractive risk-adjusted returns for clients.