* Formerly called U.S. Large Capital Equity Strategy.

1 Basis point (bp) is a unit that is equal to 1/100th of 1% and is used to denote the change in price or yield of a financial instrument.

RISKS

There can be no assurance the Strategy will achieve its investment objectives.

Investors should be able to withstand short-term fluctuations in the equity markets and fixed income marketsin return for potentially higher returns over the long term. The value of portfolios changes every day and can beaffected by changes in interest rates, general market conditions and other political, social and economic developments.

The Strategy and may assume large positions in a small number of issuers which can increase the potential forgreater price fluctuation.

International investing involves special risks including currency risk, increased volatility, political risks, and differencesin auditing and other financial standards.

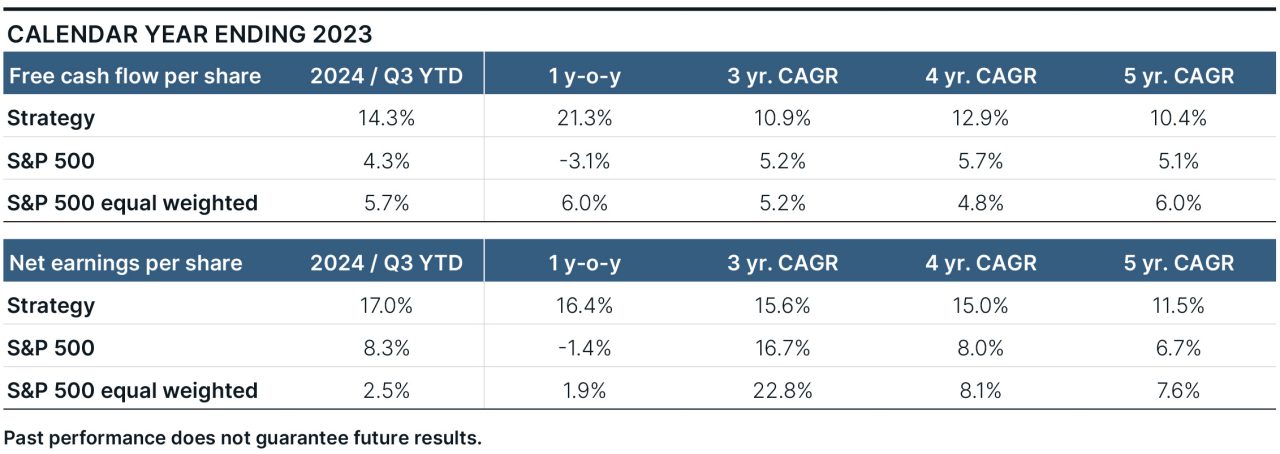

Gross of fee performance does not reflect the deduction of investment advisory fees. Net of fees performanceresults reflect the deduction of the maximum investment advisory fees. Returns include all dividends and interest,other income, realized and unrealized gain, are net of all brokerage commissions and execution costs. Performancecalculated in U.S. dollars.

Brown Brothers Harriman Investment Management (“IM”) claims compliance with the Global Investment PerformanceStandards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse orpromote this organization, nor does it warrant the accuracy or quality of the content contained herein. To receiveadditional information regarding IM, including a GIPS Composite Report for the strategy, contact John Ackler at212-493-8247 or via email at john.ackler@bbh.com.

Brown Brothers Harriman & Co. (“BBH”) may be used as a generic term to reference the company as a whole and/or its various subsidiaries generally.This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries.This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended asan offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and maynot be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketingor recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, andreliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the contentdisclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respectiveowners. © Brown Brothers Harriman & Co. 2025. All rights reserved.

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE

IM-16141-2025-02-26 Exp. Date 4/30/2025