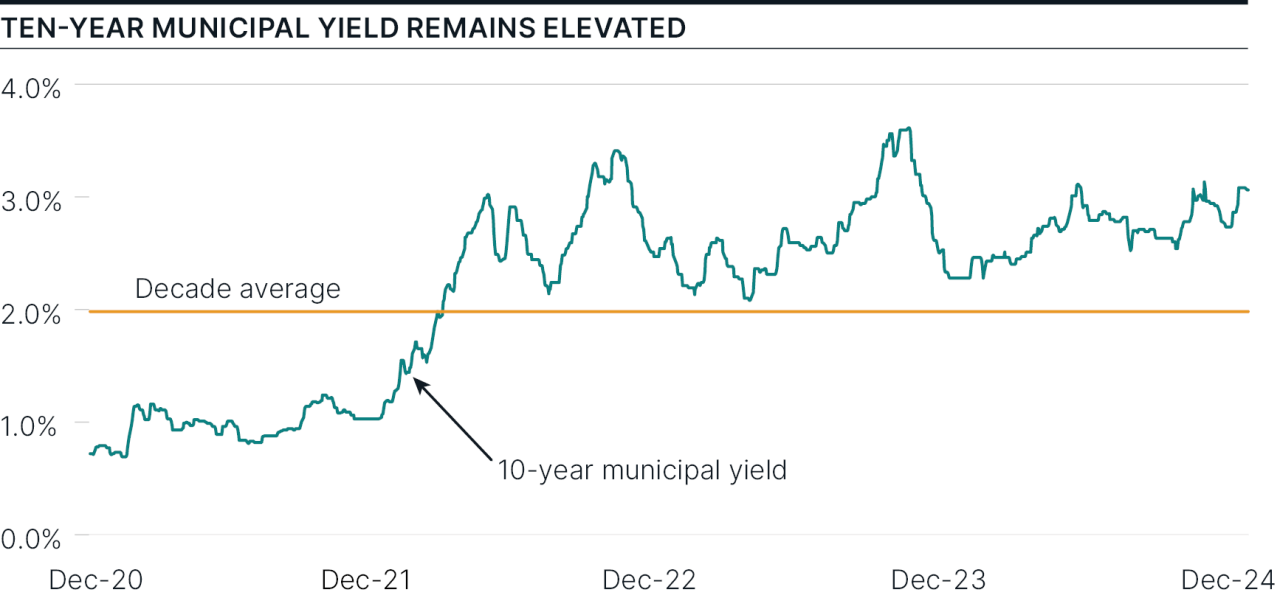

Exhibit 1: A chart depicting the 10-Year Municipal Yield.

Source: Refinitiv MMD.

4Q Highlights

|

When the story of 2024 is written, we expect a riveting page turner. The long-awaited pivot to Federal Reserve (Fed) easing, the return of an upward sloping yield curve, and record municipal new issuance all served as highlights. Credit spreads also ended the year near their historical lows, driving strong performance of lower-rated bonds.

Closer to home, we produced one of our best years of performance. We are especially proud of this result given the rally in low-rated bonds, of which we own few. Elevated market volatility and the resulting healthy flow of opportunities provided a strong helping hand. Times like this help validate active management: the more disorderly the market, the more value we can usually find.

In 2022, the Fed was forced to make a stand against inflation, tightening policy aggressively through 2023. Satisfied with inflation progress toward its long-term target, the Fed shifted its focus this summer to the other objective of its dual mandate — maximum employment. In September, the Fed turned the page and began an easing cycle. As we close the book on 2024, the Fed has cut rates 100 basis points (bps).1 Ironically, longer term rates have risen sharply with 10-year maturity municipal yields up 90 bps over the year. Yet another great reminder of the unpredictability of interest rates!

Exhibit 1: A chart depicting the 10-Year Municipal Yield.

Source: Refinitiv MMD.

Ongoing economic strength, inflationary risks associated with large fiscal deficits, and protectionist policies have reduced expectations about future policy rate cuts. The Fed itself also appears less confident about its path ahead, especially as its progress at bringing inflation back to target has stalled.

In bond markets, yesterday’s pain often leads to tomorrow’s gain. Although the recent selloff in bonds may have muted 2024 returns, municipal yields are ending the year at their highs. Remember, our portfolios carry a substantial yield advantage over generic AAA-rated bonds, with yields close to 4%, or about 6% on a pre-tax equivalent basis for those in the top-bracket. The combination of Fed rate cuts and higher long-term yields has also brought back an upward sloping yield curve for the first time in over two years. This should also help bolster future returns. Combined, these tailwinds should help you shake off the cold of these winter months!

It is a great time to review your asset allocation. Despite leading the pack for much of the last three years, cash will have a difficult time competing with traditional fixed income moving forward. We continue to recommend shifting to a more normal fixed income allocation both in terms of size and duration. From where we stand now, the downside of an intermediate strategy is limited.

We consider yields increasing 100 bps as a practical bear market scenario. Were that to happen, portfolio yields would be able to offset most of the downward price pressure over a 12-month period. We view this scenario as unlikely given that the 10-year municipal yield peaked 50 bps higher than today’s levels in the fall of 2023, when the Fed was still tightening.

There is no shortage of indicators that define the rampant volatility experienced in recent years. In 2024, an outrageous statistic is that the average weekly change in Municipal VRDN rates was north of 50 bps! Volatility of longer maturity instruments picked up markedly during the fourth quarter. Yields climbed 40 to 60 bps across maturities as investors anxiously awaited the election outcome. As the market absorbed the details of the new administration and election angst subsided, yields declined 20 to 40 bps by the end of November. That rally proved short lived. Yields increased 30 to 40 bps to close out the year as investors reacted poorly to the Fed’s waning enthusiasm for future rate cuts.

The selloff pushed intermediate returns into negative territory for the quarter and under 1% for the year. Our portfolios fared better with a -0.9% return for the quarter and a 2.5% return for the year. This brings our year-to-date outperformance to over 150 bps. Our yield advantage, driven by housing, prepaid energy, airports, and bonds with non-standard coupon structures, was the main driver of performance. Abstaining from lower-rated credit was like driving on a long and lonesome highway this year and we are proud of our results given our preference for high-quality securities.

Strong fundamentals in combination with attractive yields drove consistent demand for municipal mutual funds and ETFs. Credit also remained strong, which helped solidify retail demand. Even margins in the healthcare sector, one of the areas hardest hit by the pandemic, are improving. Since the July 4th holiday, Funds have attracted net inflows for 23 consecutive weeks. We much prefer investing during periods of pessimism with high levels of redemption activity like we had in 2022 and 2023. This year’s consistent inflows reduced secondary market opportunities and we are grateful 2024’s heavy new issuance helped fill that gap.

Municipal supply exceeded $500 billion, an increase of more than 40% relative to 2023 and a new record. Excluding taxable municipals, 2024’s $460 billion of issuance easily beat the prior record of $400 billion set in 2016. The new issue calendar provided plenty of opportunities throughout the year, particularly in sectors important to our strategy: Housing PAC and airport issuance increased 23% and 35%, respectively. In recent years, these have served as a major source of our yield advantage over the index. We are pleased that early projections for 2025 indicate another strong year of strong issuance.

We entered the fourth quarter with our portfolios on solid footing, and selectively added several attractive opportunities. During periods of heavy issuance, smaller deals can slip through the cracks. Such was the case with a $35 million delayed-delivery deal issued by AAA-rated Norfolk Water Enterprise. We purchased two-thirds of the deal at a significant discount to its fair value. We take pride in finding value in niche sectors and overlooked securities. Taking meaningful positions in high-quality securities that provide attractive yield or return potential defines our strategy.

During the quarter, we also expanded our footprint in the multifamily housing sector. Multifamily programs help finance affordable rental units for low- to moderate-income families. Unlike our single-family housing bonds, which are backed by a pool of federally backed collateral, our multifamily bonds enjoy a direct guaranty from either Fannie Mae or Freddie Mac. The bonds have a relatively narrow buyer base and consequently offer much higher yields than their AAA ratings would suggest.

Finally, we had another active quarter in the prepaid energy sector. Money center banks usually serve as guarantors on these transactions, but insurance companies have also stepped in. Specifically, we purchased prepaid energy bonds backed by Pacific Life and New York Life, both at wider spreads than their prevailing taxable corporate debt.

As we look ahead, investors are analyzing the new administration’s potential impact on the Municipal market. While numerous policy ideas have been floated, with all the same old cliches, tax reform will be top of mind. The top four items we are watching are outlined in the nearby table:

Exhibit 2: A table outlining four potential tax policy reforms that we are monitoring.

Today’s higher yields provide clients with attractive opportunities to extend duration and defend their portfolio income. Cash reserves will likely struggle to keep pace. We believe our portfolios are well-positioned in high-quality, durable credits that provide attractive yields. The market volatility of the last three years has proven unprecedented, and we are proud to have capitalized on it. We will approach the future with the same methods that have proven successful through market cycles. Our team is excited about turning the calendars to 2025 and look forward to next year’s treasure hunt!

Best wishes for a healthy, happy, and prosperous 2025 and thank you for your ongoing trust and confidence.

| Performance As of December 31, 2024 |

|||||||

|---|---|---|---|---|---|---|---|

Total Returns |

Average Annual Total Returns |

||||||

Composite/Benchmark |

3 Mo. |

YTD |

1 Yr. |

3 Yr. |

5 Yr. |

10 Yr. |

Since Inception |

BBH Municipal Fixed Income Composite (gross of fees) |

-0.81% |

2.71% |

2.71% |

1.04% |

1.82% |

2.59% |

3.63% |

BBH Municipal Fixed Income Composite (net of fees) |

-0.87% |

2.45% |

2.45% |

0.79% |

1.56% |

2.33% |

3.37% |

Bloomberg 1-10 Yr. Municipal Bond Index |

-0.94% |

0.91% |

0.91% |

0.15% |

1.03% |

1.81% |

3.15% |

| Sources: BBH & Co. and Bloomberg Returns of less than one year are not annualized. BBH Municipal Fixed Income inception date is 05/01/2002. |

|||||||

| Past performance does not guarantee future results. | |||||||

| Representative Account Top 10 Obligors As of December 31, 2024 |

|

|---|---|

South Carolina Mortgage Revenue Bonds |

2.9% |

Salem-Keizer School District #24J, OR |

2.4% |

Texas Department of Housing and Community Affairs Single Family Mortgage Revenue Bonds |

2.4% |

Illinois Housing Development Authority |

2.4% |

Houston Airport Enterprise, TX |

2.2% |

New Mexico Mortgage Finance Authority |

2.2% |

Central Plains Energy Project Gas Project Revenue Bonds Project No. 5 Series 2022 |

2.2% |

Texas Municipal Gas Corporation II |

2.1% |

Grossmont Healthcare District |

2.1% |

Salt Verde Financial Corporation |

2.0% |

Total |

22.9% |

| Sources: BBH and Bloomberg | |

1 Basis point (bp) is a unit that is equal to 1/100th of 1% and is used to denote the change in price or yield of a financial instrument.

Risks

There is no assurance that a portfolio will achieve its investment objective or that the strategy will work under all market conditions. The value of the portfolio can be affected by changes in interest rates, general market conditions and other political, social and economic developments. Each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market.

Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, maturity, call and inflation risk; investments may be worth more or less than the original cost when redeemed.

Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

The Strategy also invests in derivative instruments, investments whose values depend on the performance of the underlying security, assets, interest rate, index or currency and entail potentially higher volatility and risk of loss compared to traditional stock or bond investments.

As the Strategy’s exposure in any one municipal revenue sector backed by revenues from similar types of projects increases, the Strategy will become more sensitive to adverse economic, business or political developments relevant to these projects.

The Representative Account is managed with the same investment objectives and employs substantially the same investment philosophy and processes as the strategy.

The objective of our Municipal Fixed Income Strategy is to deliver excellent after-tax returns in excess of industry benchmarks through market cycles. The Composite includes all fully discretionary fee-paying municipal fixed income accounts with an initial investment equal to or greater than $5 million that are managed to an average duration of approximately 4.5 years. Portfolios that subsequently fall below $4.5 million are excluded from the Composite.

Bloomberg 1-10 Year Municipal Bond Index is a component of the Bloomberg Municipal Bond index, including bonds with maturity dates between one and 17 years. The Bloomberg Municipal Bond Index is considered representative of the broad market for investment grade, tax-exempt bonds with a maturity of at least one year. One cannot invest directly in an index.

Bloomberg US Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $300 million par amount outstanding and with at least one year to final maturity.

Bloomberg US Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers. The Index is a component of the US Credit and US Aggregate Indices. “Bloomberg®” and the Bloomberg 1-10 Year Municipal Bond Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Brown Brothers Harriman & Co (BBH). Bloomberg is not affiliated with BBH, and Bloomberg does not approve, endorse, review, or recommend the BBH Strategy. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the fund.

Brown Brothers Harriman Investment Management (“IM”), a division of Brown Brothers Harriman & Co (“BBH”), claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

To receive additional information regarding IM, including a GIPS Composite Report for the strategy, contact John Ackler at 212 493-8247 or via email at john.ackler@bbh.com.

Gross of fee performance results for this composite do not reflect the deduction of investment advisory fees. Actual returns will be reduced by such fees. “Net” of fees performance results reflect the deduction of the maximum investment advisory fees. Returns include all dividends and interest, other income, realized and unrealized gain, are net of all brokerage commissions, execution costs, and without provision for federal or state income taxes. Results will vary among client accounts. Performance calculated in U.S. dollars.

Holdings are subject to change.

Credits: Obligations such as bonds, notes, loans, leases and other forms of indebtedness, except for Cash and Cash Equivalents, issued by obligors other than the U.S. Government and its agencies, totaled at the level of the ultimate obligor or guarantor of the Obligation.

Issuers with credit ratings of AA or better are considered to be of high credit quality, with little risk of issuer failure. Issuers with credit ratings of BBB or better are considered to be of good credit quality, with adequate capacity to meet financial commitments. Issuers with credit ratings below BBB are considered speculative in nature and are vulnerable to the possibility of issuer failure or business interruption.

Opinions, forecasts, and discussions about investment strategies represent the author’s views as of the date of this commentary and are subject to change without notice. References to specific securities, are for illustrative purposes only and are not intended to be, and should not be interpreted as recommendations.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. IM-15795-2025-01-09

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE MONEY