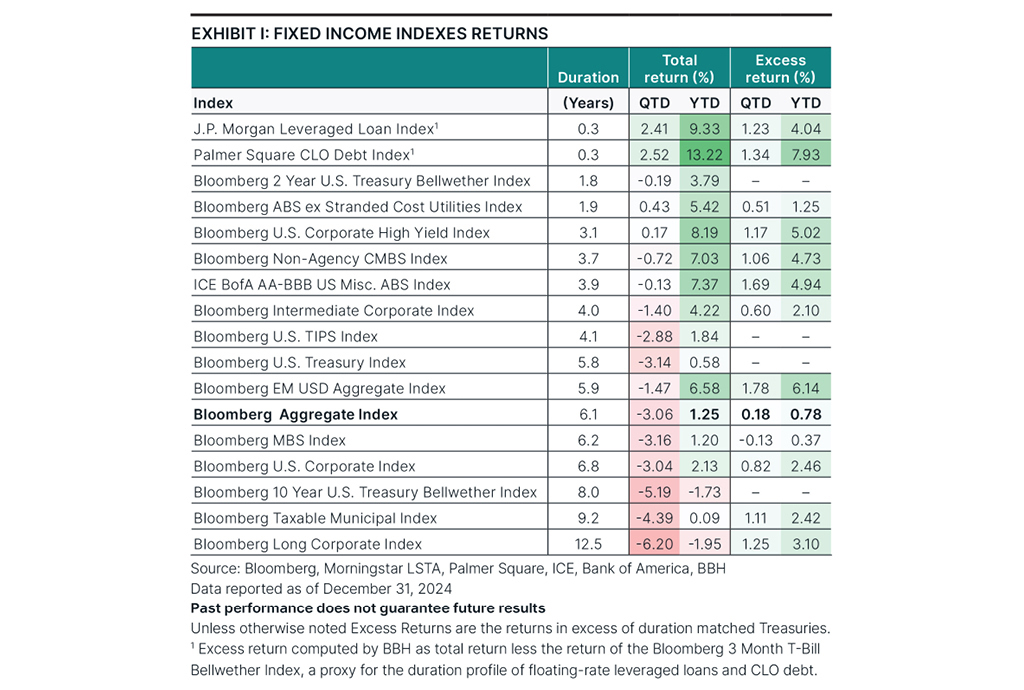

Exhibit I: Fixed income index returns for various indexes as of December 31, 2024, displaying duration, total return, and excess return.

4Q Highlights

|

| Performance As of December 31, 2024 |

|||||||

|---|---|---|---|---|---|---|---|

|

Total Return |

Average Annual Total Returns |

|||||

Composite/Benchmark |

3 Mo. |

YTD |

1 Yr. |

3 Yr. |

5 Yr. |

10 Yr. | Since Inception |

BBH Limited Duration Fixed Income Composite (Gross of Fees) |

1.17% |

7.04% |

7.04% |

4.67% |

3.75% |

2.98% |

4.57% |

BBH Limited Duration Fixed Income Composite (Net of Fees) |

1.10% |

6.77% |

6.77% |

4.41% |

3.50% |

2.74% |

4.35% |

Bloomberg 1-3 Year US Treasury Index |

-0.10% |

4.03% |

4.03% |

1.43% |

1.36% |

1.38% |

3.68% |

| Past performance does not guarantee future results Returns of less than one year are not annualized Strategy Inception: 04/01/1990 |

|||||||

| The Bloomberg 1-3 Year US Treasury Index is an unmanaged index of fixed rate obligations of the U.S. Treasury with maturitiesranging from 1-3 years. Sources: Bloomberg and BBH & Co. |

|||||||

Market Environment

Treasury note yields rose last quarter despite the Federal Reserve’s (the Fed) campaign of cutting interest rates. The Fed cut the federal funds rate by a total of 0.50% during the quarter and 1.00% during the 2024 calendar year. Nevertheless, note yields rose across all tenors, on the quarter and for the year driven by lower expectations for interest rate cuts in 2025. Fed funds rate expectations for the coming year were 4.00% vs. 3.00% when the quarter began.

Most fixed income indexes experienced negative quarterly total returns due to the rise in interest rates. The Bloomberg U.S. Aggregate Index declined more than 3%. Excess returns to credit, however, were overwhelmingly positive as credit spreads in mainstream indexes narrowed further to their cyclical lows.

Short- and intermediate-duration fixed income indexes managed positive total returns for 2024 despite the rise in interest rates. Long-duration indexes posted negative total returns during the calendar year as the rise in interest rates offset any yield benefits. The Bloomberg U.S. Aggregate Index advanced just 1.3% in 2024, three points lower than its 4.5% yield at the start of the year. Excess returns to credit were positive across all major sectors in 2024.

Strong economic data does provide a tailwind to credit, although risks are emerging with looming changes to U.S. fiscal policies. Headline consumer inflation prints have been declining but remain above Fed targets. Wage growth and job openings remain higher than historic averages and could still exert upward pressure on inflation. The Chicago Fed National Activity Index remains above its recession indicator.

Corporate default rates diverged between bonds and loans, with the default rates on bonds lower and loans higher. Distressed exchanges and liability management exercises – which are undertaken by companies to avoid default but still disadvantage debtholders – are increasing. Overall, default rates for bonds and loans were steady year over year. Defaults continue to be concentrated among CCC-rated issuers, although default rates for all rating categories are below their respective long-term averages. Business loan performance appears healthy, as delinquency and charge-off rates are low and new bankruptcy filings are near pre-pandemic lows.

There are some signs of stress emerging for U.S. consumers. Loan delinquency and charge-off rates are rising to normal levels across many loan types, while the prospects of higher-for-longer interest rates and the resumption of federal student loan repayments loom as risks to straining the U.S. consumer. The increases in loss and delinquency rates remain within expected ranges and do not signal heightened risk of impairment to asset-backed securities (ABS) bondholders.

Commercial real estate headlines remain disconnected from property-level dynamics. High-quality properties have refinanced and there have been minimal losses on paydowns in commercial mortgage-backed securities (CMBS) deals. Commercial real estate woes have not had an outsized impact on banks’ commercial real estate loan portfolios to date, as delinquency rates and charge-offs have been muted.

Heavy credit issuance and narrowing risk spreads were among the biggest stories of the fourth quarter and the 2024 calendar year. Headline issuance volumes were robust across credit sectors. Net issuance, though, was more moderate in most sectors, as most 2024 issuance was to refinance existing debt. Nontraditional ABS are the exception, as the outstanding market of nontraditional ABS grew 11% year over year on the heels of a 34% surge in volumes.

Valuations

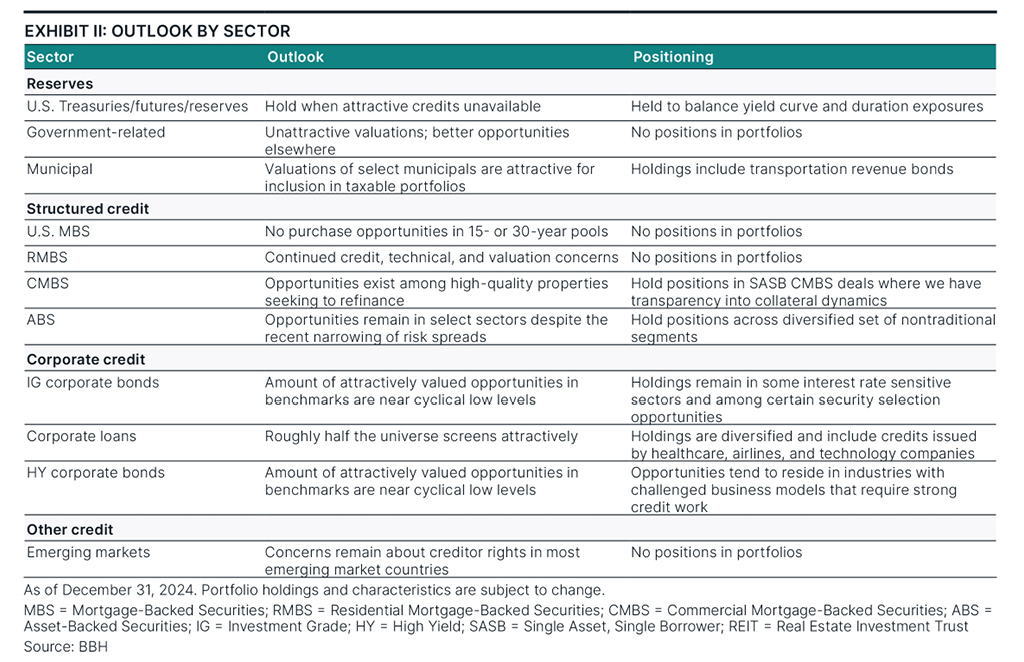

The compression of credit spreads amid low net issuance growth and strong inflows into fixed income is suggestive of an environment where many credits’ valuations are overbought and disconnected from their fundamentals. BBH’s valuation framework1 lends credence to that theory. The framework identifies few opportunities today in traditional index segments of the credit markets. The percentage of potential “buy” opportunities is screening near cyclical low levels across most sectors. It’s declined to 4% from 7% for investment-grade corporate bonds, to 58% from 68% for corporate loans, and to 16% from 19% for high-yield corporate bonds. No cohort of the 15- or 30-year mortgage-backed securities (MBS) market screens as a “buy” candidate. Away from credits in mainstream indexes, bonds of collateralized loan obligations (CLOs) and a minority of nontraditional ABS sectors have narrowed to recent lows and screen unattractively for new purchases, although most non-traditional ABS and CMBS continue to screen attractively.

There remain opportunities in select subsectors of the market. Investment-grade corporate bonds in life insurance and banking, two interest rate-sensitive subsectors, continue to offer attractive opportunities. The corporate loan market continues to offer numerous opportunities that screen as “buy” candidates. In the structured credit markets, we continue to find opportunities in a variety of ABS subsectors through our bottom-up process. Opportunities are arising in the CMBS market as supportive property and deal-level dynamics are disconnected from the negative headlines impacting the sector.

We continue to avoid emerging markets credits due to concerns over creditor rights in most countries and the impact on their durability. We continue to avoid non-agency residential mortgage-backed securities (RMBS) generally due to poor technical factors, unattractive valuations, and weak fundamentals, underpinned by poor housing affordability, low inventory of homes for sale, and stable-to-declining home prices.

Performance

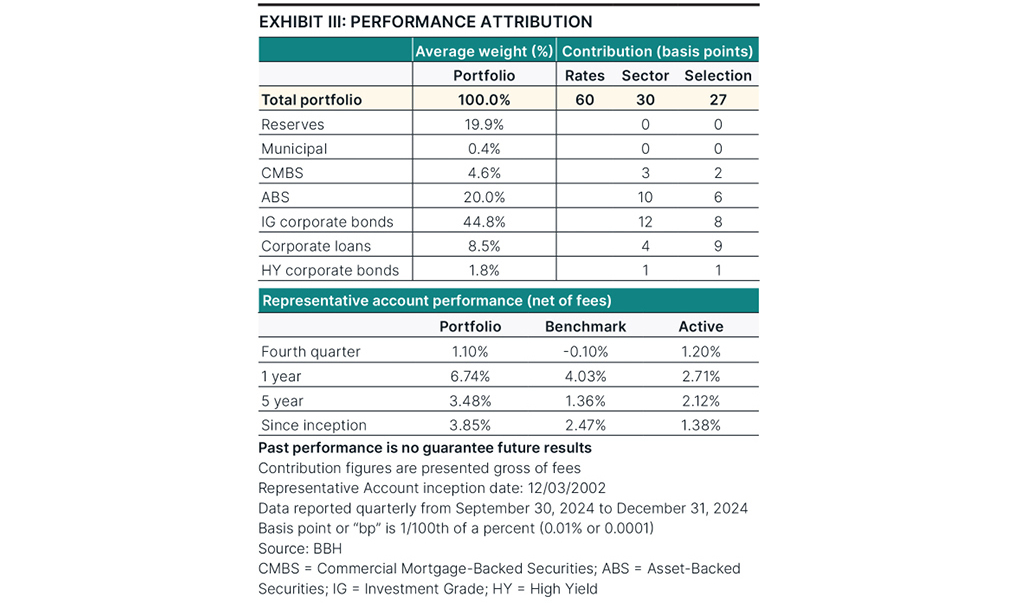

The portfolio outperformed its benchmark during the quarter on the heels of favorable credit selection results, sector and rating emphases, and defensive duration positioning in an episode of sharply rising interest rates.

The portfolio’s duration profile contributed to total returns during the quarter as interest rates rose, and it had a stronger impact on relative returns as the portfolio’s one- to three-year Treasury benchmark had a slightly negative return during the quarter.

The portfolio’s sector and rating emphases contributed to relative results during the quarter. The portfolio was allocated to strong-performing segments of the credit markets within its holdings of investment-grade corporate bonds, ABS, CMBS, and corporate loans.

Security selection was additive to relative performance during the quarter, and there were contributions across the sectors in which the portfolio was invested. Holdings of loans to healthcare, media entertainment, and wireline telecommunication companies impacted performance favorably. Investment-grade corporate bonds issued by life insurers, banks, and specialty finance companies also enhanced performance. Positions in loans to specialty finance companies and asset managers, as well as high-yield bonds issued by technology companies, detracted from selection results.

Exhibit III: Attribution as of December 31, 2024, showing average portfolio weight and gross contribution displayed in basis points.

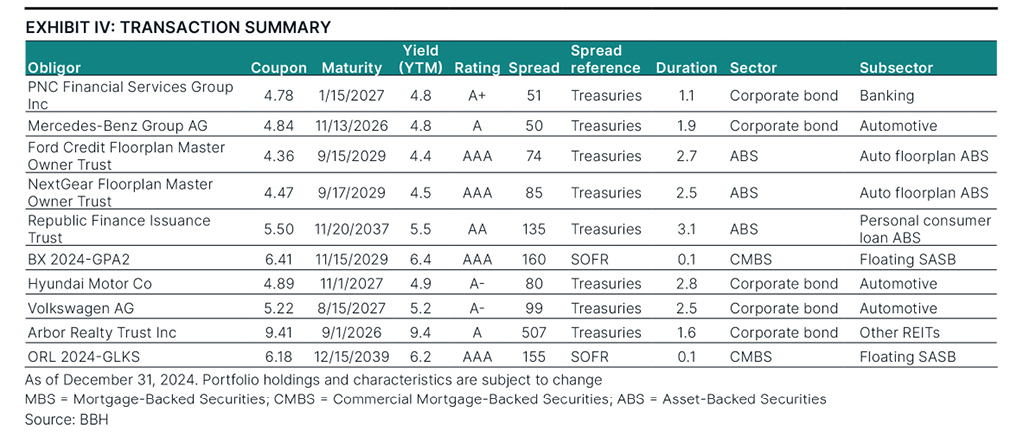

Transaction Summary

We continued to find durable credits2 offering attractive value despite weak attractiveness of valuations of credits in indexes. The table below summarizes a few notable portfolio additions.

Characteristics

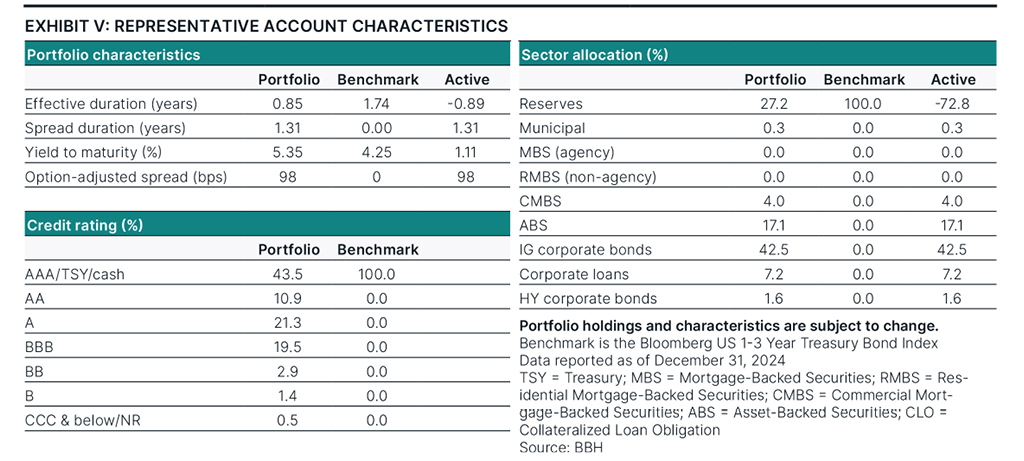

At the end of the quarter, the portfolio’s duration was 0.9 years. The portfolio’s weight to reserves increased to 27% from 15% while its weights to credit sectors decreased. The weight to high-yield and non-rated investments declined to 5% from 6%, were comprised primarily of credits rated “BB,” and consisted of a blend of corporate bonds and loans. The portfolio’s yield to maturity was 5.4% and remained elevated vs. short-term bond market alternatives. The portfolio’s option-adjusted spread was 98 basis points (bps)3 over Treasuries; for reference, the longer-duration Bloomberg U.S. Corporate Index’s was 80 bps over Treasuries at quarter end.

Exhibit V: Characteristics as of December 31, 2024, including credit rating and sector allocation.

Concluding Remarks

Credit investors face a choice today: keep buying expensive credit and hope that historical credit risks and pricing don’t return in the near term, or stick with valuation discipline, a longer-term view, and realism on the inevitability of a rise in credit spreads. We believe the valuation and credit disciplines embedded in our bottom-up process will help us balance caution and opportunity in this environment.

1Our valuation framework is a purely quantitative screen for bonds that may offer excess return potential, primarily from mean reversion in spreads. When the potential excess return is above a specific hurdle rate, we label them “Buys” (others are “Holds” or “Sells”). These ratings are category names, not recommendations, as the valuation framework includes no credit research, a vital second step.

2Obligations such as bonds, notes, loans, leases, and other forms of indebtedness, except for cash and cash equivalents, issued by obligors other than the U.S. Government and its agencies, totaled at the level of the ultimate obligor or guarantor of the Obligation. Durable means the ability to withstand a wide variety of economic conditions.

3Basis point (bp) is a unit that is equal to 1/100th of 1% and is used to denote the change in price or yield of a financial instrument.

The securities do not represent all of the securities purchased, sold, or recommended for advisory clients and you should not assume that investments in the securities were or will be profitable.

Issuers with credit ratings of AA or better are considered to be of high credit quality, with little risk of issuer failure. Issuers with credit ratings of BBB or better are considered to be of good credit quality, with adequate capacity to meet financial commitments. Issuers with credit ratings below BBB are considered speculative in nature and are vulnerable to the possibility of issuer failure or business interruption.

Purchase and sale information provided should not be considered as a recommendation to purchase or sell a particular security and that there is no assurance, as of the date of publication, that the securities purchased remain in a portfolio or that securities sold have not been repurchased.

Opinions, forecasts, and discussions about investment strategies are as of the date of this commentary and are subject to change without notice. References to specific securities, asset classes, and financial markets are not intended to be and should not be interpreted as recommendations.

Definitions

ICE BofA 1-3 U.S. Year Treasury Index is an unmanaged index that tracks the performance of the direct sovereign debt of the U.S. Government having a maturity of at least one year and less than three years.

Duration is a measure of the portfolio’s return sensitivity to changes in interest rates.

An index is not available for direct investment

“Bloomberg®” and the Bloomberg indexes are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the indexes (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Brown Brothers Harriman & Co (BBH). Bloomberg is not affiliated with BBH, and Bloomberg does not approve, endorse, review, or recommend the Strategy. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Strategy.

Risks

Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, maturity, call and inflation risk; investments may be worth more or less than the original cost when redeemed. Bond prices are sensitive to changes in interest rates and a rise in interest rates can cause a decline in their prices. Mortgage-backed securities have prepayment, extension, and interest rate risks.

Asset-Backed Securities (“ABS”) are subject to risks due to defaults by the borrowers; failure of the issuer or servicer to perform; the variability in cash flows due to amortization or acceleration features; changes in interest rates which may influence the prepayments of the underlying securities; misrepresentation of asset quality, value or inadequate controls over disbursements and receipts; and the ABS being structured in ways that give certain investors less credit risk protection than others. Below investment grade bonds, commonly known as junk bonds, are subject to a high level of credit and market risks.

SASB lacks the diversification of a transaction backed by multiple loans since performance is concentrated in one commercial property. SASBs may be less liquid in the secondary market than loans backed by multiple commercial properties.

The Strategy invests in derivative instruments, investments whose values depend on the performance of the underlying security, assets, interest rate, index or currency and entail potentially higher volatility and risk of loss compared to traditional bond investments.

Foreign investing involves special risks including currency risk, increased volatility, political risks, and differences in auditing and other financial standards. Prices of emerging market securities can be significantly more volatile than the prices of securities in developed countries, and currency risk and political risks are accentuated in emerging markets.

The Strategy may engage in certain investment activities that involve the use of leverage, which may magnify losses.

A significant investment of assets in one or more sectors, industries, securities and/or durations may increase its vulnerability to any single economic, political, or regulatory developments, which will have a greater impact on returns.

Illiquid investments subject the investor to the risk that she may not be able to sell the investments when desired or at favorable prices.

Portfolio Characteristics are of the Representative Account. The Representative Account is managed with the same investment objectives and employs substantially the same investment philosophy and processes as the Strategy.

Brown Brothers Harriman Investment Management (“IM”), a division of Brown Brothers Harriman & Co (“BBH”), claims compliance with the Global Investment Performance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

To receive additional information regarding IM, including a GIPS Composite Report for the strategy, contact John W. Ackler at 212 493-8247 or via email at john.ackler@bbh.com.

Gross of fee performance results for this composite do not reflect the deduction of investment advisory fees. Actual returns will be reduced by such fees. Net of fees performance results reflects the deduction of the maximum investment advisory fees. Returns include all dividends and interest, other income, realized and unrealized gain, are net of all brokerage commissions, execution costs, and without provision for federal or state income taxes. Results will vary among client accounts. Performance calculated in U.S. dollars.

The objective of our Limited Duration Fixed Income Strategy is to deliver excellent returns in excess of industry benchmarks through market cycles. The Composite includes all fully discretionary fee-paying accounts with an initial investment equal to or greater than $10 million with a duration of approximately 1.5 years. Accounts that subsequently fall below $9.25 million are excluded from the Composite.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved.

Not FDIC Insured No Bank Guarantee May Lose Money

IM-16009-2025-02-03 Exp. Date 04/30/2025