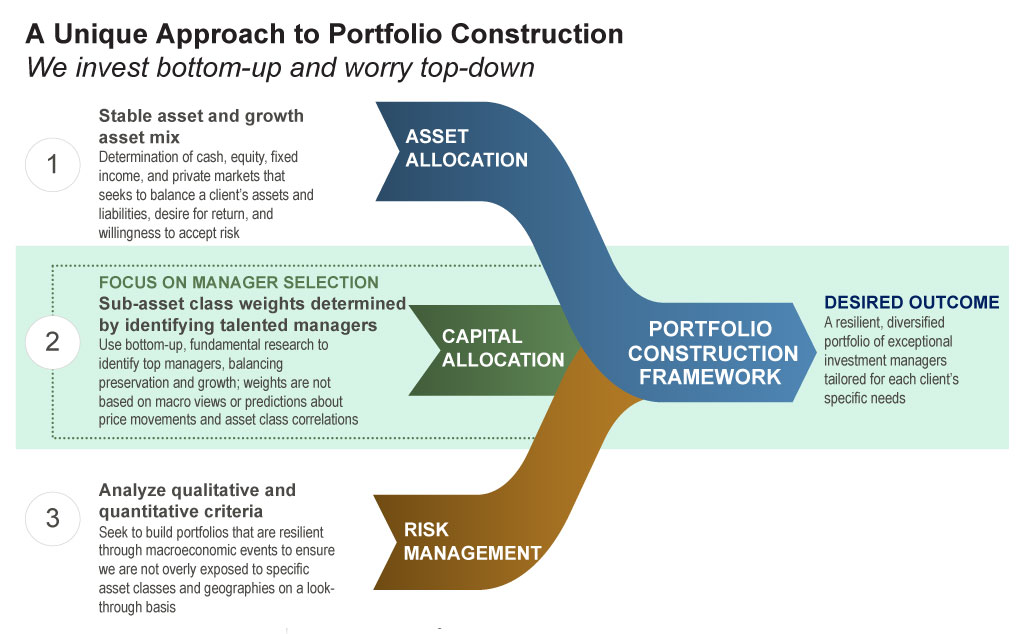

This graphic depicts how our asset allocation, capital allocation, and risk management frameworks inform BBH’s portfolio construction process.

At Brown Brothers Harriman (BBH), we are partners in our clients’ success. We go the extra mile to ensure our clients achieve their goals and objectives, preserving and growing wealth along the way.

To do so, we must question and test common investment industry assumptions, with the idea that a rigorous application of “truth seeking” will allow us to generate better results for our clients. We have crafted sophisticated frameworks in our unique approach to portfolio construction to enhance the traditional asset allocation process.

BBH’s Holistic Approach to Portfolio Construction

We believe in a multipronged implementation of several different allocation frameworks to achieve a balanced and resilient portfolio. The Investment Research Group (IRG) has frequently discussed our unique three-step approach to portfolio construction, which involves asset allocation, capital allocation, and risk management. Importantly, each of these elements incorporates additional second-order allocation frameworks, such as:

- Risk-return goals

- Objectives

- Liquidity needs

- Role in the portfolio

- Style

In this article, we describe how we use each of these allocation frameworks to construct custom portfolios that meet each client’s risk/return objectives, as well as goals and liquidity needs. The following chart depicts how these frameworks all inform BBH’s portfolio construction process.

Asset Allocation

Most in the investment industry think of asset allocation as using techniques such as mean-variance optimization (MVO) to bucket portfolios among different sub-asset classes based on top-down macroeconomic and financial market variables.

However, we define asset allocation as the process of selecting the optimal mix of cash, public equities, fixed income, and private investments that best balances a client’s goals, objectives, liquidity needs, and risk tolerance.

Determining a client’s investment goals and objectives is a critical step in the portfolio construction process. Considerations we assess for each client include:

This graphic shows various considerations when construction a client's investment portfolio, including financial situation, risk tolerance, investment goals, and preferences and constraints.

These considerations can further be refined to several second-order allocation frameworks:

- Risk-return goals

- Objectives

- Liquidity needs

Risk-Return Goals Allocation

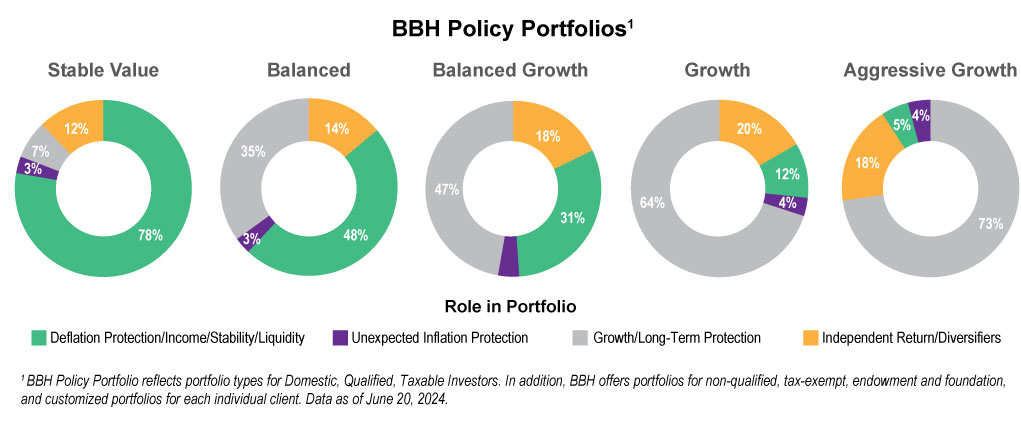

Risk-return goals-based allocation is often used in conversations involving one’s investment policy statement (IPS). BBH manages investment portfolios that span the spectrum of risk tolerance and return objectives.

For example, our Stable Value portfolios – which seek to support both current and future spending needs by focusing on income, liquidity, and total return – are composed largely of fixed income and cash, with small allocations to equities and private investments.

On the other side of the spectrum, our Aggressive Growth (or All-Equity) portfolios, which seek to preserve and grow purchasing power by employing an approach focused predominately on capital appreciation, are made up largely of public and private equity exposure.

| Role in Portfolio | Stable Value | Balanced | Balanced Growth | Growth | Aggressive Growth |

| Deflation Protection/Income/Stability/Liquidity | 78% | 48% | 31% | 12% | 5% |

| Unexpected Inflation Protection | 3% | 3% | 4% | 4% | 4% |

| Growth/Long-Term Inflation Protection | 7% | 35% | 47% | 64% | 73% |

| Independent Return/Diversifiers | 12% | 14% | 18% | 20% | 18% |

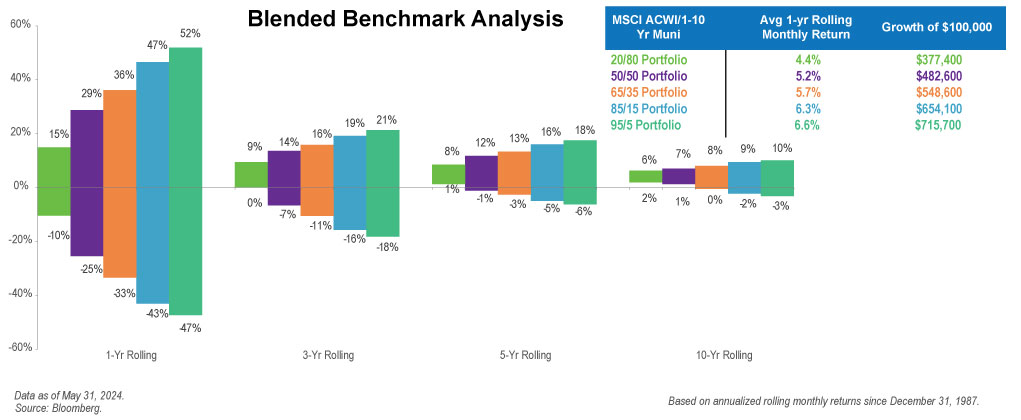

A risk-return goals-based allocation facilitates conversations around potential trade-offs between expected returns and several different definitions of risk. We often share charts like the one below to engage our clients in “what-if” scenarios, which helps us better align their portfolios with their true return objectives and risk tolerance.

| 1-Yr Rolling | 3-Yr Rolling | 5-Yr Rolling | 10-Yr Rolling | ||||||||||||||||||||

| Stable Value | Balanced | Balanced Growth | Growth | Aggressive Growth | Stable Value | Balanced | Balanced Growth | Growth | Aggressive Growth | Stable Value | Balanced | Balanced Growth | Growth | Aggressive Growth | Stable Value | Balanced | Balanced Growth | Growth | Aggressive Growth | ||||

| Max | 15% | 29% | 36% | 47% | 52% | 9% | 14% | 16% | 19% | 21% | 1% | 12% | 13% | 16% | 18% | 2% | 1% | 8% | 9% | 10% | |||

| Min | -10% | -25% | -33% | -43% | -47% | 0% | -7% | -11% | -16% | -18% | 7% | -1% | -3% | -5% | -6% | 4% | 6% | 0% | -2% | -3% | |||

An asset allocation comprising 95% equity and 5% fixed income (solely using index performance) has experienced annual returns that range from 52% to -47%. Clients who are unwilling to potentially incur such volatility should consider portfolios with lower equity exposure.

It is worth noting that in order to complement equity and fixed income, we source private market investments to enhance overall performance, increase diversification, and reduce portfolio risk.

We do look to analyses such as MVO to help inform risk-return allocation, but we emphasize that it is just one of many different considerations that should inform one’s overall portfolio construction.

Objectives Allocation

Objectives-based allocation can also help refine a client’s portfolio, with separate return and risk goals for each objective. Objectives can include:

- Spending

- Philanthropy

- Retirement

- Opportunistic capital (e.g., cash intended for once-a-decade opportunities)

- Inheritance

Such allocations help increase the probability that a portfolio will meet a client’s goals and objectives, as success is often multidimensional and reflects more than one objective.

Liquidity Needs Allocation

Liquidity refers to the ability to convert an investment to cash without affecting its market price. The determination around a liquidity needs allocation framework is often closely related to a client’s assets and liabilities, age, and time horizon.

For example, a young client with few liquidity needs and a long time horizon could choose to invest a large percentage in relatively illiquid investments, whereas a client with large upcoming liquidity needs would be advised to have a higher allocation to cash and fixed income by comparison.

Our liquidity needs allocation breaks down all of the underlying investments by liquidity classification (for example, highly liquid, liquid, and limited liquidity), which allows us to ensure that our clients’ liquidity needs are met. Liquidity stress testing the portfolio can provide enhanced comfort that the desired liquidity will be available in potential times of stress.

It is worth noting that these three components of asset allocation – returns, objectives, and liquidity – should not be viewed in isolation. Rather, it is the combination of them all, and the conversations they foster, that facilitate great portfolio construction.

Capital Allocation

Capital allocation, or manager selection, involves identifying exceptional investment managers capitalizing on market inefficiencies.

We do not set targets for sub-asset classes based on macroeconomic views or predictions about price movements and asset correlations. Instead, sub-asset class weights are largely determined by our long-term conviction in specific investment managers.

This bottom-up approach to sub-asset class weights prevents us from forcing capital into a sub-asset class where we cannot find a manager that meets our rigorous standards. All investment opportunities must compete for capital against all other opportunities regardless of sub-asset class.

Our approach to capital allocation allows us to generate additional alpha1 for our clients. The scale to which the traditional asset class approach is practiced often causes market inefficiencies that allow us to find overlooked, yet exceptional, investment managers.

For example, many U.S.-based advisors use a U.S./international equity construct that implicitly removes global strategies (that is, strategies that can invest in both the U.S. and internationally) from consideration. A flexible mandate that invests in both the U.S. and internationally allows us to partner with managers who do not fit squarely into commonly used classifications. Accordingly, we have found an attractive universe of such managers who have typically been overlooked as an accident of traditional asset allocation structuring.

We believe that our approach to portfolio construction, which is similar to many of the top-performing endowments and foundations, provides a richer universe of opportunities, resulting in a high-quality portfolio that best optimizes return for a given level of risk.

To underscore this, we turn to Howard Marks, co-chairman of Oaktree Capital and the former investment committee chair at the Metropolitan Museum of Art’s endowment:

- A common perception of risk illustrates the risk-return trade-off where lower risk equates to lower potential return, and higher risk equates to higher potential return. Marks suggests that this is often erroneously taken to imply that “riskier investments produce higher returns.”

- Instead, we look at the relationship between risk and return where, in Marks’ words, “the return of each investment is shown as a range of possibilities, not the single outcome suggested by the upward-sloping line.”

Our capital allocation process demands that we partner with top-quartile managers who can drive outcomes such that they land in the top half of a distribution for a given level of risk. Effectively, our approach to capital allocation is focused on achieving higher returns while holding risk constant by partnering with the world’s best investors.

While the majority of our efforts in capital allocation relate to the aforementioned processes, there are a couple of second-order capital allocation frameworks that are worth highlighting:

- Role in the portfolio

- Style

Role in the Portfolio

We categorize investments into four different categories by the role they play in the portfolio. This allocation framework ensures that we focus on more than just the underlying assets and look at the role we expect the strategy to play in the portfolio.

- Public and private equity provide growth and long-term inflation protection. Many investors understand intuitively that public equities should provide growth in one’s portfolio, but the long-term inflation protection benefits are often underappreciated. Since 1926, the S&P 500 has annualized at 9.8% on average, while inflation has grown at a 3% average rate over the same time.

We focus on investing in high-quality companies that have pricing power, which implies that they can raise prices faster than the underlying rate of inflation by passing on price increases to customers. We believe that this provides our clients with more attractive growth and long-term inflation protection. As we have long said, the best hedge against inflation over the long term is high-quality equities.

- Real estate, or opportunistically, Treasury inflation-protected securities (TIPS), provide short-term inflation protection. Within our real estate portfolio, the majority of our assets are multi-family housing, where rents generally adjust every 12 months to increase in line with, or in excess of, inflation spikes. The American Housing Survey shows that during the inflationary period between 1973 and 1983, median multi-family rent expanded at an average rate of 8.5% and easily outpaced relative inflation.

- Cash and fixed income provide deflation protection, stability, liquidity, and/or yield. These roles are particularly useful but must be balanced with the fact that cash and most fixed income investments do not provide long-term inflation protection. In other words, a portfolio of only cash and fixed income, while providing stability, is unlikely to preserve real purchasing power over time.

In the 15 years following the great financial crisis, fixed income and cash investors also did not provide the yield that investors sought. However, the post-pandemic interest rate regime has resulted in a higher interest rate environment that is finally providing investors with more attractive yields.

- Private debt, distressed, alternative credit, insurance, and other nontraditional opportunities provide independent return or diversifying exposures. Importantly, these assets should be capable of generating public equity-like returns with low public equity beta.2 We look to returns in this category to be driven largely by alpha, which by definition is idiosyncratic, and therefore diversifying.

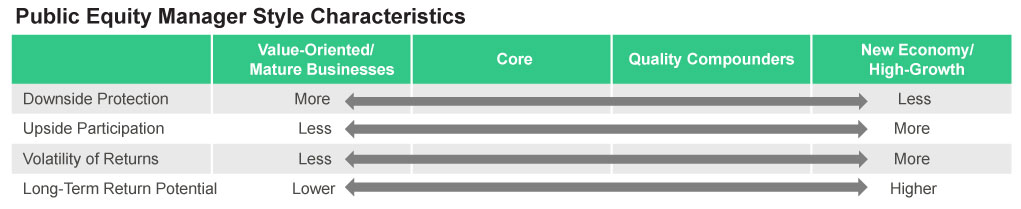

Style Allocation

While we spend a lot of time selecting a concentrated group of exceptional investment managers on a bottom-up basis, that alone is insufficient capital allocation.

We also classify our managers by style characteristics – such as value-oriented, core, quality compounders, and high growth in our public equity portfolio. This allows us to better understand how the portfolio’s underlying investments will work together to maximize return and minimize risk.

- Value-oriented/mature: These managers tend to have a relatively stricter valuation discipline, owning more lower-growth businesses that generate a higher current free cash flow yield. Many of these companies are in more mature industries.

- Core: These managers tend to be valuation sensitive and own more stable or modest growth businesses.

- Quality compounders: These managers typically target mid-teen returns or above and have long time horizons, although such managers tend to be slightly less valuation sensitive than core and value-oriented managers. The underlying businesses tend to be predictable with above-average growth profiles.

- New economy/high-growth: These managers tend to exhibit higher tracking error relative to benchmarks, more upside potential, greater volatility, and higher long-term return expectations.

This graphic shows our public equity manager style characteristics – value-oriented/mature businesses, core, quality compounders, and new economy/high-growth.

Risk Management

The final step in our portfolio construction process is risk management. Given our focus on bottom-up selection and unwillingness to fill asset class buckets with inferior managers, we insist upon a rigorous application of risk management. This approach ensures there are no unintended consequences of our previous portfolio construction-related decisions and that we capitalize on short- and medium-term market inefficiencies through opportunistic portfolio adjustments.

To address unintended consequences, we employ a top-down risk management overlay designed to avoid unintended risk exposures by analyzing a range of different qualitative and quantitative criteria.

Risks are usually viewed as threats to wealth preservation and growth, but they can also highlight opportunities that we can capitalize on through opportunistic portfolio adjustments. For example:

- During the COVID-19 pandemic, we had a short-duration bias within our fixed income portfolio, which was rewarded when the Federal Reserve started raising rates in March 2022 and longer-duration fixed income sold off. “Cash was not trash” in this environment, and we took advantage by purchasing securities with high yields and very low risk.

- More recently, with rate cuts more likely than rate increases, we have been extending duration at the most attractive parts of the yield curve, locking in attractive yields for longer time horizons.

- We also look to make such portfolio adjustments outside of the fixed income portfolio. For example, prior to the pandemic, our team recognized potential company distress in several markets and opportunistically partnered with an exceptional distressed debt manager that successfully capitalized on the distressed opportunities in 2020 and 2021.

- Today, we are acutely aware of the threats and opportunities surrounding artificial intelligence (AI). We have positioned our public equity portfolio to overweight companies that should benefit from the rise of AI rather than those that may be disrupted. We have also allocated more capital to an exceptional venture capital manager that has been a leader in AI for over a decade.

Capital Impairment

Chief among the myriad risks investors must consider is permanent capital impairment. What is difficult about this is that “permanent” is often indistinguishable from “temporary.” From time to time, the fundamentals of our underlying investments will become disconnected from how they are priced in the market. Price is not value.

The key is to have the confidence to stick with your investment manager during periods where prices are lagging the fundamental performance of the underlying assets. Temporary price underperformance during a period of fundamental asset performance is actually an opportunity to buy (or hold) assets on sale, which, research has shown, will reflect fundamental performance in the long run.

Downside Returns

Because our approach to portfolio construction incorporates several dimensions, we also monitor risks such as “the risk of falling short.” It is human nature to focus on downside risk. Indeed, behavioral economics makes it clear that losses of the same amount as gains are felt 2.25 times as much.3

Yet we also understand that for many of our clients, not having the necessary assets or liquidity at the right time is also a risk that warrants much consideration. As such, it is imperative to understand the downside return potential for any relevant portfolio over a certain period of time. Without this “worst-case scenario” visualization, a client could end up without sufficient cash for spending needs or wealth for future generations, for example.

Rebalancing

Rebalancing is the final leg of our risk management approach. We generally encourage thoughtful rebalancing, which incorporates tax considerations where appropriate, to ensure optimized long-term results. Rebalancing is, at its core, an exercise in risk control, in that it keeps a client’s portfolio in line with desired allocation ranges.

Importantly, our approach to rebalancing requires that we know the fundamental performance of our portfolio, not just the price performance. We spend a lot of time monitoring the valuation and fundamental performance of our portfolio (and the underlying managers and assets) relative to various benchmarks. This allows us to rebalance in a targeted way that can add value to long-term results.

For example, when a manager has generated higher earnings, better margins, and higher cash flow than a relevant benchmark but has underperformed, we may suggest adding capital to that manager and moving some away from one that has exhibited price increases in excess of its fundamentals. Tax impact must be considered where necessary, but we have found that such data-informed rebalancing can enhance after-tax portfolio results.

Conclusion

Our approach to portfolio construction is multifaceted and client-specific. We believe that leveraging our unique three-step approach to portfolio construction – which involves asset allocation, capital allocation, and risk management, with additional second-order asset allocation frameworks built into each layer – is the surest way to generate long-term success for our clients while mitigating risk.

We look forward to continuing to be partners in your success, tailoring our unique allocation frameworks to help you best meet your goals and objectives.

Contact Us

1 Alpha is the amount by which a strategy has outperformed its benchmark, taking into account the strategy’s exposure to market risk (Source: Morningstar).

2 Beta is a measure of a portfolio’s sensitivity to market movements. The beta of the broader equity market, as measured by the S&P 500, is 1.00 (Source: Morningstar).

3 Kahneman, D., & Tversky, A. (1979). Prospect Theory: An Analysis of Decision Under Risk,” Econometrica, XLVII (1979), 263-91.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07530-2024-06-27