What a difference a year makes. A little over a year ago, the U.S. economy was reeling from the extraordinary measures taken to slow the spread of COVID-19: Businesses were shut, those that remained open were operating remotely or under severe constraints, air travel ground to a near halt, and we got to know our families a lot better. The U.S. government responded to this challenge with financial support on an unprecedented scale and breadth. Starting with the CARES Act in early March 2020, and continuing into the Biden administration, Washington has spent well over $5 trillion to preserve economic vitality and retain as many jobs as possible. At the same time, the Federal Reserve slashed interest rates to zero while buying close to $4 trillion of Treasuries and asset-backed securities to ensure that fixed income markets remained healthy and borrowing costs low.

It worked. After a record contraction of 31% in the second quarter of last year, GDP bounced back 33% in the third quarter, and by summer 2021 has regained all the ground lost during the pandemic recession, and then some. The National Bureau of Economic Research – the official arbiter of when economic cycles begin and end – announced that the recession that began in February 2020 ended in April 2020, setting a record for the shortest and sharpest contraction in American economic history.

As vaccination rates rise and life lurches back to a semblance of normality, the question now is what will be the economic price of this extraordinary government intervention. The federal budget has run a deficit of more than 10% for over a year, and the Federal Reserve has bought bonds and increased the size of its balance sheet by over $4 trillion since the beginning of the pandemic. Traditional economic theory holds that the inevitable price tag of deficit spending and excessive growth in money supply is inflation, and the bill has arguably already arrived.

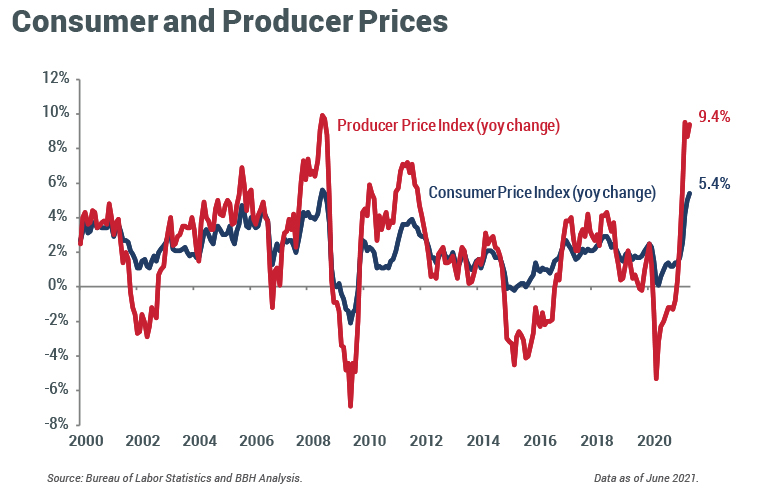

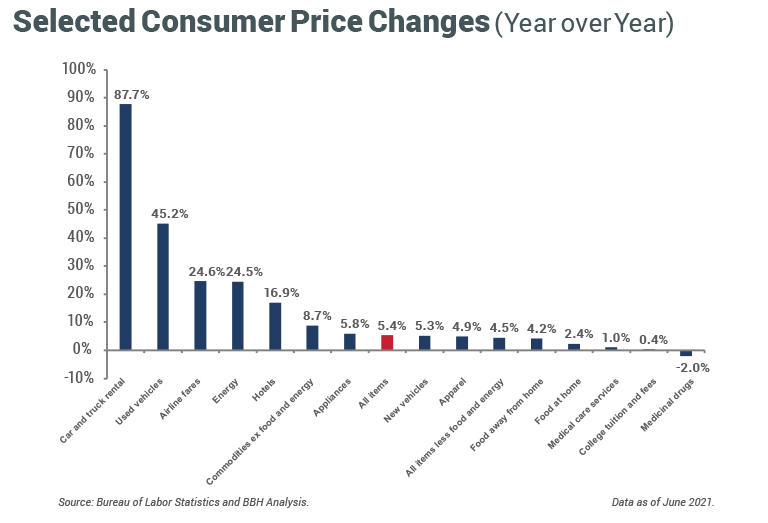

The consumer price index (CPI) was up 5.4% in June 2021, and core prices (excluding food and energy) were up 4.5%. This is only the third month this century that a monthly CPI report has been north of 5%. Perhaps even more worrisome, producer price index (PPI) increases have hovered around 9% for the past three months. To the degree that producers are able to pass on these costs to consumers, it will add further pressure to consumer prices. Prices of basic commodities such as soybeans, lumber, oil and steel have risen sharply from pandemic lows, implying that there may be even more inflationary pressure to come as these prices feed through into end products.