The first phase – the documented annual review of compliance policies and procedures – went into effect on November 13. Here’s our key takeaways:

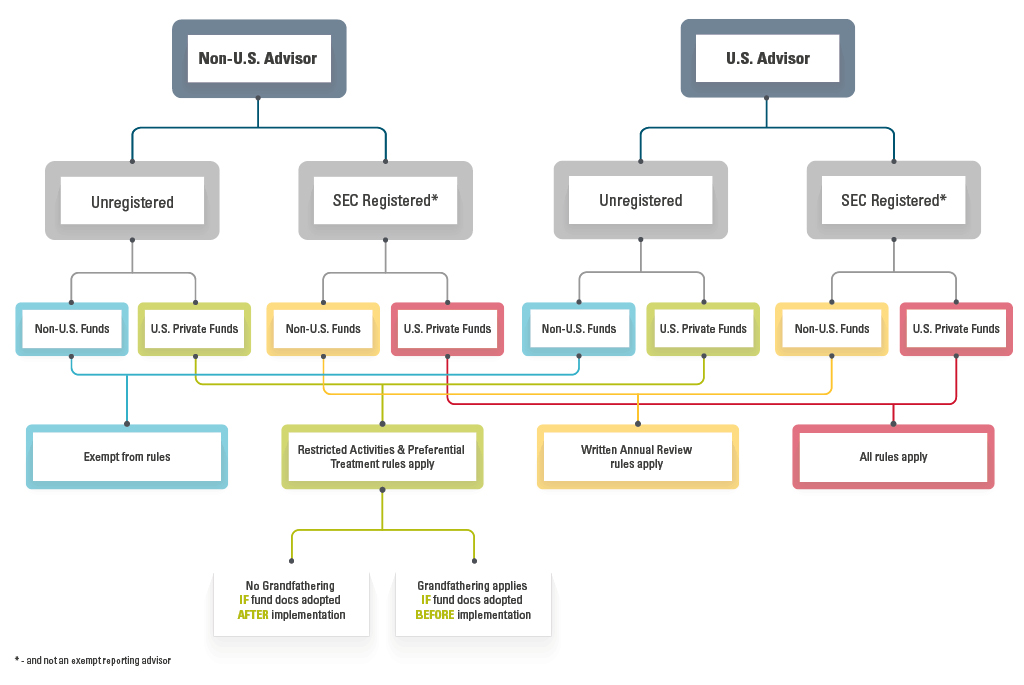

Who’s in scope of the rules?

There are five key components to the SEC’s final rule and their impacts largely depend on a mixture of your location and your registration status.

- Non-US Advisor → Unregistered → Non-US Funds → Exempt from rules

- Non-US Advisor → Unregistered → US Private Funds → Restricted activities & Preferential treatment rules apply → No Grandfathering IF fund docs adopted AFTER implementation

- Non-US Advisor → Unregistered → US Private Funds → Restricted activities & Preferential treatment rules apply → Grandfathering applies IF fund docs adopted BEFORE implementation

- Non-US Advisor → SEC Registered → Non-US Funds → Written Annual Review Rules Apply

- Non-US Advisor → SEC Registered → US Private Funds → All Rules Apply

- US Advisor → Unregistered → Non-US Funds → Exempt from rules

- US Advisor → Unregistered → US Private Funds → Restricted Activities & Preferential Treatment Rules Apply → No Grandfathering IF fund docs adopted AFTER implementation

- US Advisor → Unregistered → US Private Funds → Restricted Activities & Preferential Treatment Rules Apply → Grandfathering applies IF fund docs adopted BEFORE implementation

- US Advisor → SEC Registered → Non-US Funds → Written Annual Review Rules Apply

- US Advisor → SEC Registered → US Private Funds → All Rules Apply

Why are they needed?

The new rules restrict activity that the SEC believes may be a conflict of interest or involve controversial compensation plans. However, the Rules generally allow advisors to engage in such restricted activities so long as there is investor consent and transparency.

To maintain compliance with both the new rules and the Advisors Act compliance rule, the SEC is also adopting corresponding amendments to the Advisors Act books and records rule.

What are the five rules?

In some respects, the new rules are similar to European private fund rules (e.g.: AIFMD). While the data disclosures will largely be in pro forma templates, they will require significant work to set up, oversee, and distribute the required information, as well as a relatively tight timeline to prepare for implementation.

This is unquestionably a new dawn for U.S. private fund reporting.

1. Quarterly Statement Rule

Private fund investors require quarterly statements to list fund details such as portfolio companies, performance metrics, as well as fees and expenses specifying:

- Advisor compensation details - including those related to the amount allocated or paid by the private fund to the Registered Investment Advisor (RIA) and any of its related persons. Compensation details should also include total compensation and fund expenses before and after applicable offsets, rebates, or waivers.

- Fees and expenses allocated to or paid by the private fund (e.g., organizational, accounting, legal, administration, audit, tax, due diligence, and travel fees and expenses).

- Portfolio investment compensation allocated or paid to the advisor by a portfolio company. Private Fund Advisors will be required to retain a copy of the quarterly statements distributed to fund investors, including the supporting data for information included in the quarterly statements.

Statements must be prepared and distributed in tabular form to existing investors within 45 days after the first three fiscal quarter ends and 90 days after the end of each fiscal year.

2. Fund Performance Rule

Prominent disclosure of the criteria and assumptions used to calculate fund performance is required. Performance inclusions within the quarterly statement should be clear, concise, and in plain English using a format that allows for comparison from one quarterly statement to the next. The reporting requires that the dates of the performance period are clearly outlined and remain current.

The rules vary slightly depending on whether the fund is considered a liquid or illiquid fund. Liquid funds may be required to display data for up to 10 fiscal years prior, while illiquid funds must provide detailed quantitative metrics, in an itemized manner, such as Internal Rates of Return (IRR) and Multiple of Invested Capital (MOIC), and a statement of contributions and distributions. This will add a new administrative burden and complexity to all in scope funds.

3. Audit Rule

Advisors must ensure the fund undergoes a financial statement audit that meets the requirements of the audit provision in the SEC’s Custody Rule (also subject to proposed changes) at least annually and on liquidation. This requirement applies whether the advisor directly or indirectly provides investment advice to the fund. The audit must be conducted under U.S. GAAP by an independent public accountant per SEC requirements and must be registered with and subject to regular inspection by the Public Company Accounting Oversight Board (PCAOB). Unlike the Custody Rule, there is no alternative means of satisfying the private fund audit requirements within these rules. The recently proposed SEC Safeguarding Advisor Client Assets proposal also interplays with these audit requirements.

4. Advisor Led Secondaries Rule

Secondary transactions, which are initiated by the advisor, offer fund investors the choice to sell all or a portion of their interests in one private fund and invest all or a portion of that interest in another private fund. Due to the increased volume of activity in advisor-led secondary transactions, especially closed-ended private funds, the SEC now requires the advisor to obtain a fairness or valuation opinion from an independent provider. This acts as a check against any inherent conflict of interest the advisor may have in possibly profiting from such transactions at the expense of the fund investors. There are also disclosure requirements relating to the independence of “material business relationships” which seek to ensure the advisor, or other related parties, and the opinion provider are truly independent of one another. All RIAs, not just private fund advisors, must obtain a fairness or valuation opinion and disclose any material business relationships with a fairness opinion provider.

Questions around when an advisor is considered to “initiate” a transaction, e.g., if the advisor merely assists an investor with a secondary sale of the investor’s interest in the fund following an unsolicited request by that investor, are also common.

5. Restricted Activities Rule

The final rules stopped short of explicitly banning certain practices and instead opted for a disclose or gain consent for practices. It brings a level of transparency around certain existing practices, most notably relating to instances of preferential treatment of certain investors. The rules restrict all private fund advisors from certain sales practices, conflicts, and compensation schemes, which are not in the public interest or that do not protect fund investors, unless certain required disclosures are made, or in some instances consent obtained.

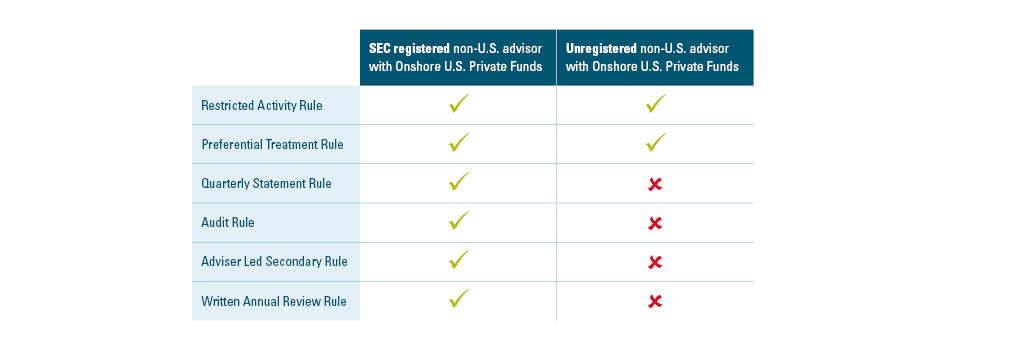

- Statement 1: SEC registered non- US advisor with Onshore U.S. Private Funds

- Statement 2: Unregistered non- U.S. advisor with Onshore U.S. Private Funds

- Restricted Activity Rule: Statement 1, yes. Statement 2, yes.

- Preferential Treatment Rule: Statement 1, yes. Statement 2, yes.

- Quarterly Statement Rule: Statement 2, yes. Statement 2, no.

- Audit Rule: Statement 1, yes. Statement 2, no.

- Advisor Led Secondary Rule: Statement 1, yes. Statement 2, no.

- Written Annual Review Rule: Statement 1, yes. Statement 2, no.

In terms of preferential treatment, the rules apply to instances of providing only certain investors with information regarding redemptions, portfolio holdings, or exposures. There are certain exemptions and any preferential treatment not disclosed in writing is strictly prohibited. The timing and detail involved in delivery of these disclosures depends on whether it is an existing or prospective fund investor.

Do these rules have extra territorial effect beyond the U.S.?

Yes. Whether by way of your registration status or even use of U.S. feeder funds (e.g.: Delaware funds) in your own offshore structures, non-U.S. managers can be drawn into the scope of the rules. It’s also largely expected that the rules may become “market standard”, so even if not directly in scope, it could potentially become table stakes for anyone selling private funds to U.S. investors to provide the information required under the SEC rules.

When will the rules come into effect?

The final rules were published in the Federal Register on September 14, 2023. This means the implementation schedule is as follows:

| Larger Private Fund Advisors (>$1.5 billion) | Smaller Private Fund Advisors (<$1.5 billion) | |

| Audit & Quarterly Statement Rules | March 14, 2025 | March 14, 2025 |

| Advisor Led Secondaries, Preferential Treatment and Restricted Activities Rules | September 14, 2025 | March 14, 2025 |

| Amended Advisors Act Compliance Rule | November 13, 2023 | November 13, 2023 |

This is a broad overview of the various aspects of the new rules, however we are just scratching the surface and will continue to provide insights. Please contact any of our team or your Relationship Excellence Manager should you wish to discuss.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. Pursuant to information regarding the provision of applicable services or products by BBH, please note the following: Brown Brothers Harriman Fund Administration Services (Ireland) Limited and Brown Brothers Harriman Trustee Services (Ireland) Limited are regulated by the Central Bank of Ireland, Brown Brothers Harriman Investor Services Limited is authorised and regulated by the Financial Conduct Authority, Brown Brothers Harriman (Luxembourg) S.C.A is regulated by the Commission de Surveillance du Secteur Financier. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2023. All rights reserved. IS-09475-2023-11-21