Considerations for GPs

For alternative asset managers looking to optimize their fundraising, our research provides numerous areas to consider:

1. Products offering flexible investor liquidity appeal to both institutional and wealth investors.

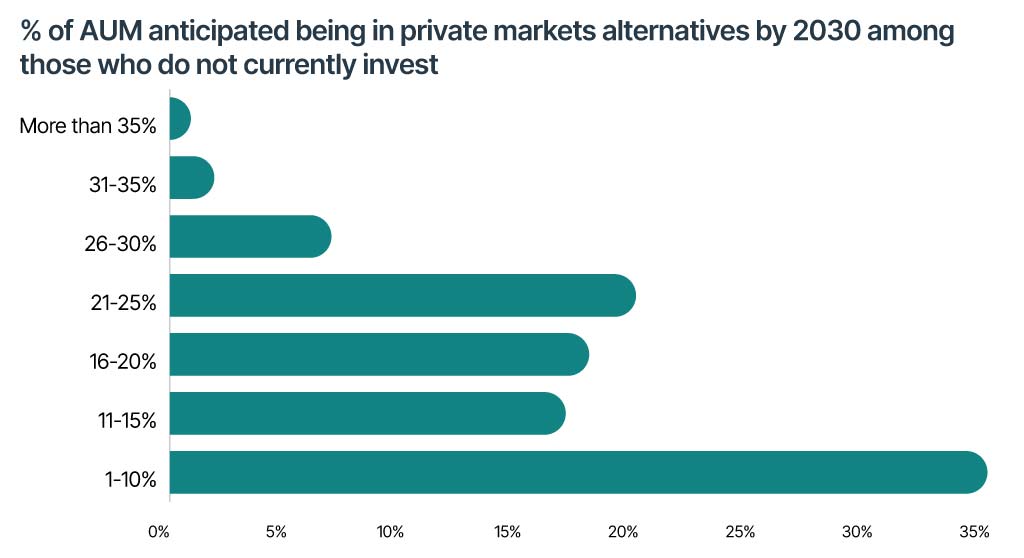

This represents a huge opportunity for GPs, but product development and investor access need to be prioritized. According to 2024 research by Preqin1, the total amount of evergreen funds – products typically designed to invest in private market assets and are oriented toward wealth investors — nearly doubled to 520 in the last five years. Despite that considerable growth, wealth advisors continue to perceive a dearth of available products and/or challenges accessing the products that do exist. Despite that considerable growth, wealth advisors continue to perceive a dearth of available products and/or challenges accessing available products. This represents a huge opportunity for GPs, but product development and investor access need to be prioritized.

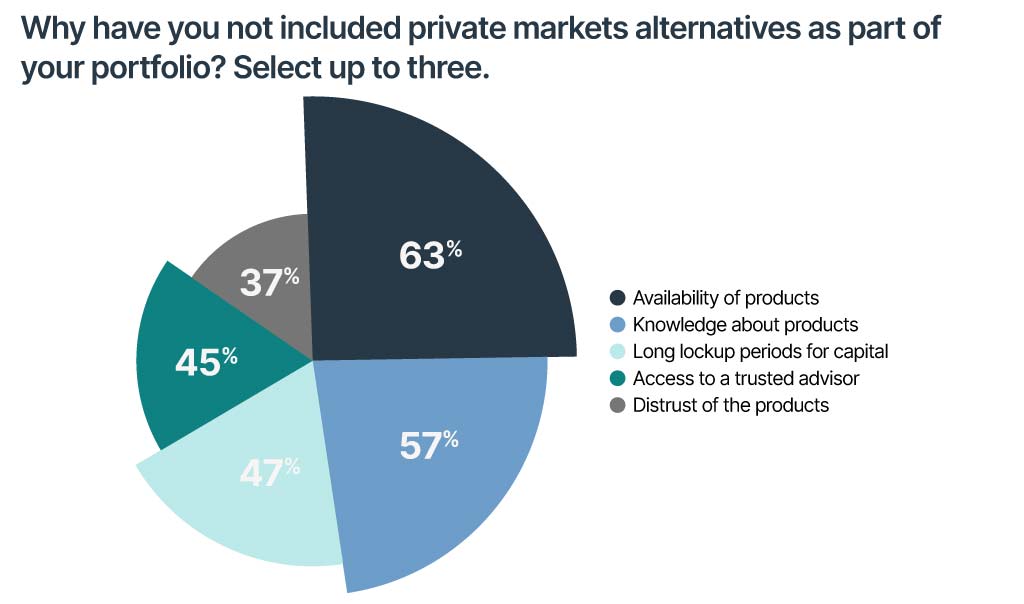

2. Investor education, particularly through the wealth advisory channels, remains a broad industry challenge.

Investor appetite is clearly there, but products with complicated liquidity provisions that may also combine both liquid and illiquid investments need to be thoughtfully explained to new investors. Ultimately, both GPs and wealth advisors bear some responsibility to educate this new base of investors.

3. LPs rank brand recognition, firm reputation, and the track record of a manager as the most important determinants in manager selection.

This is very similar to what others have reported in the traditional space, a sign of ongoing convergence across the broader asset management industry.